Excerpt

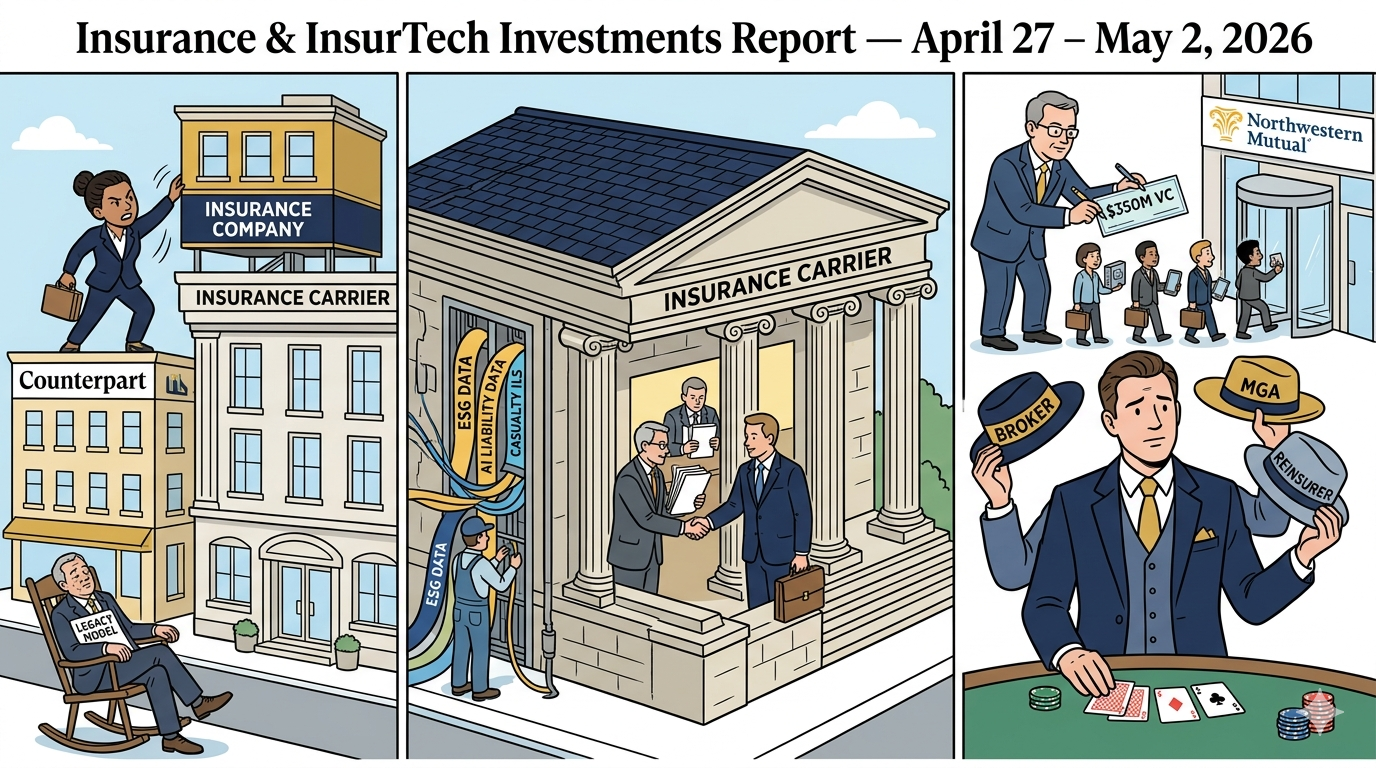

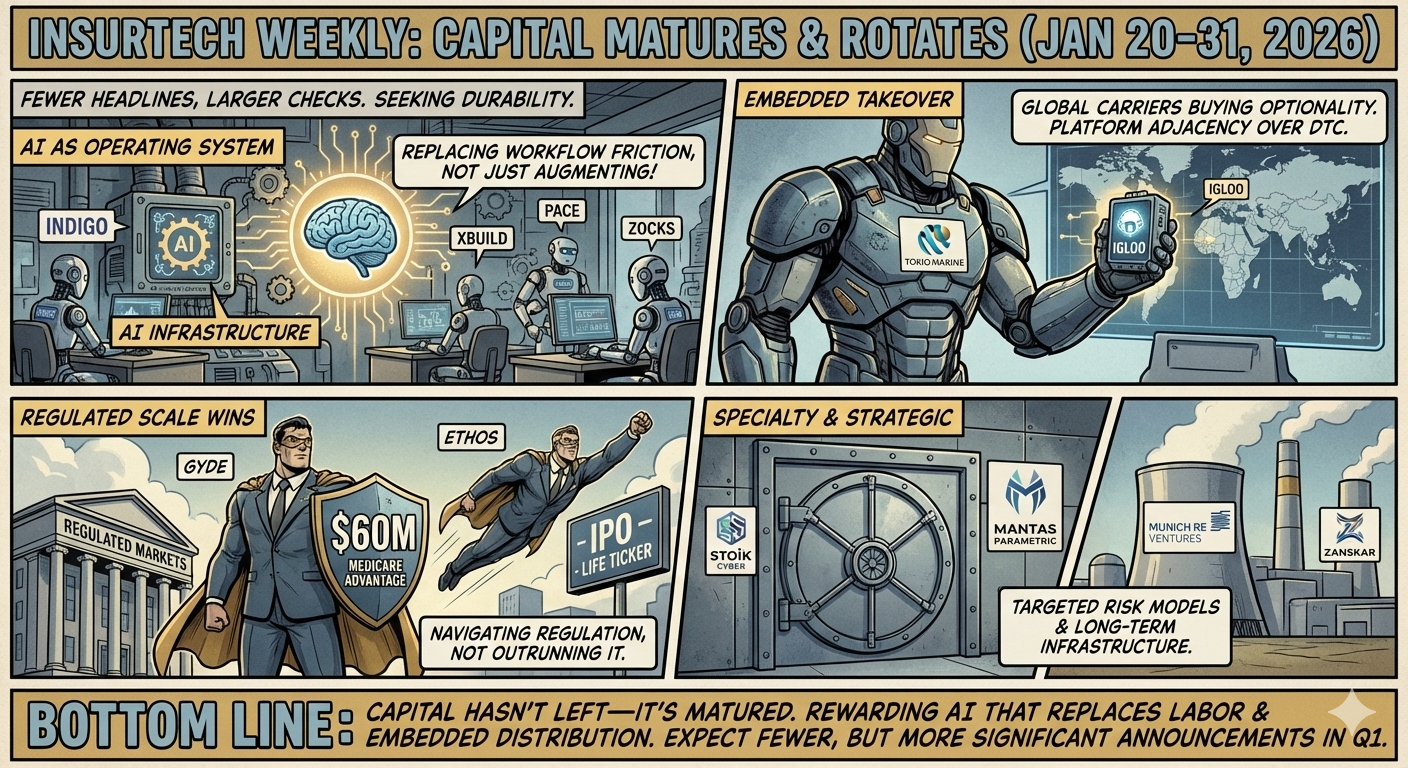

The last two weeks of January made one thing clear: insurance isn’t being “disrupted” anymore—it’s being rewired. Capital flowed decisively toward AI-native platforms, vertical specialists, and embedded distribution models, while full-stack replacement narratives continued to lose oxygen. From Gyde and Indigo redefining brokerage and underwriting economics, to Zurich backing embedded auto insurance via TrueCar, the signal is consistent: advantage now comes from infrastructure, not ambition.