January 19–31, 2026 (Week 4–5)

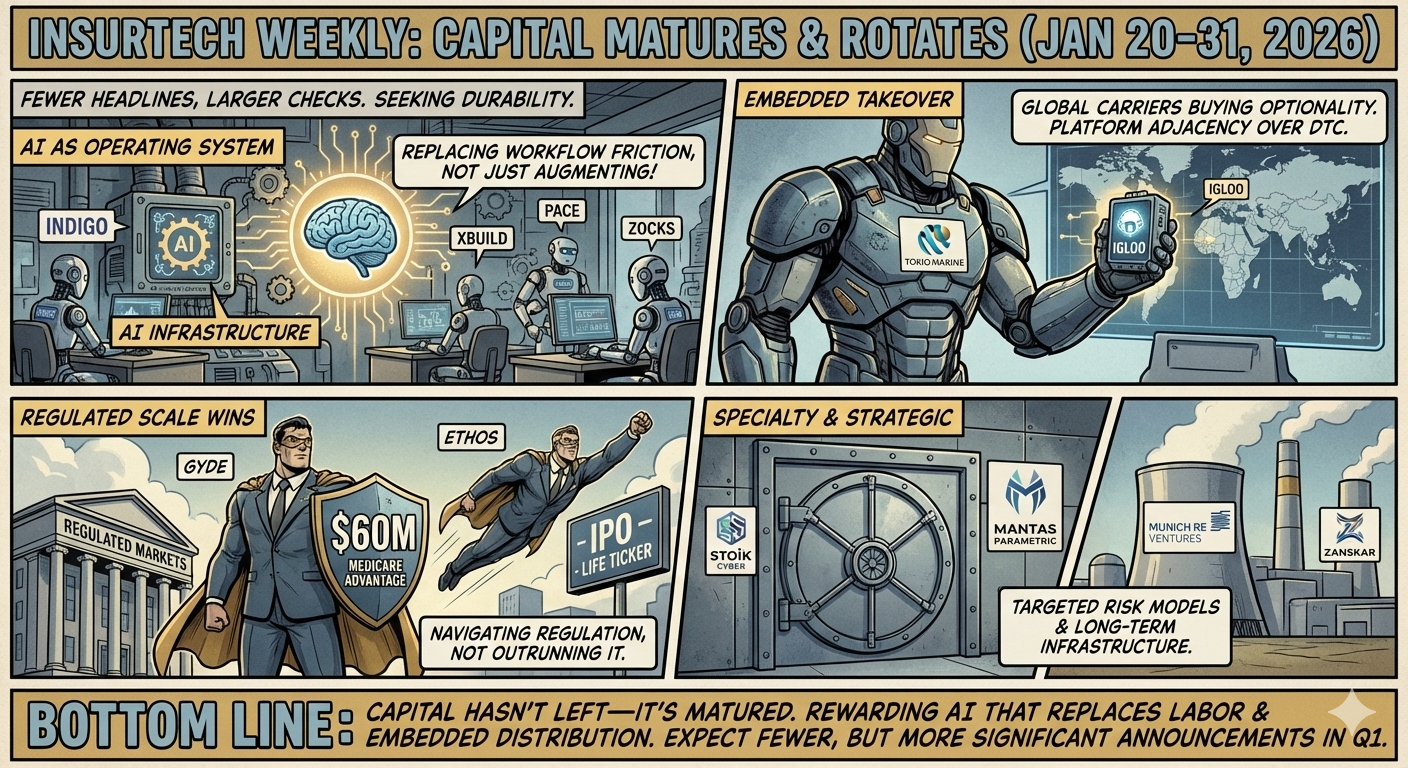

The final two weeks of January 2026 delivered $378 million in disclosed funding across insurance, insurtech, and insurance-adjacent sectors, concentrated in eight major transactions plus several strategic investments. Three mega-rounds dominate: Gyde's $60 million Series A for AI-native Medicare brokerage (Lightspeed-led), Indigo's $50 million Series B for medical malpractice AI underwriting (Rubicon Founders-led), and Zocks' $45 million Series B for financial advisor AI automation (Lightspeed and QED co-led). The period also witnessed Ethos Technologies' $200 million IPO on Nasdaq—the first major insurtech public offering of 2026—and TrueCar's $227 million take-private transaction led by founder Scott Painter with strategic insurance participation from Zurich North America.

The capital allocation pattern reflects investor conviction in three strategic themes: (1) AI-native infrastructure replacing manual workflows in brokerage, underwriting, and operations; (2) vertical specialization in underserved segments (medical malpractice, Medicare, startup insurance); and (3) embedded insurance distribution models integrated into employer benefits, financial platforms, and automotive ecosystems. Unlike earlier January deals emphasizing full-stack carriers (Corgi, Nirvana), weeks 4–5 pivot toward platform plays and distribution infrastructure—companies that enable existing market participants to adopt AI rather than displacing them entirely.

Major Investment Transactions

1. GYDE — AI-Native Medicare Brokerage at Scale

$60M | AI-powered brokerage platform | Medicare Advantage, employee benefits, individual health

Gyde launches with the largest Series A in Medicare brokerage history, deploying a roll-up strategy with an AI backbone that fundamentally differs from traditional consolidators. Rather than standardizing acquired agencies into uniform operations, Gyde preserves elite broker teams and layers proprietary technology—GydeOS (broker operating system) and Gia (intelligent assistant)—to automate administrative friction while elevating human expertise for complex advisory work.

Why it matters

- Capital as competitive weapon. $60M enables Gyde to acquire 20–30 best-in-class agencies over 24–36 months, consolidating 5–10% of the independent Medicare broker market while competitors remain fragmented.

- AI as force multiplier, not replacement. Brokers using GydeOS manage 2x–3x larger client books without proportional headcount, achieving unit economics traditional roll-ups cannot match through standardization alone.

- Strategic backing changes the game. Optum Ventures' participation provides direct access to UnitedHealthcare's ecosystem (the largest Medicare Advantage carrier), potentially unlocking preferential commission structures, exclusive product access, and co-marketing opportunities unavailable to independent brokers.

Competitive impact

- GoHealth, eHealth, SelectQuote face a credible competitor with superior technology, tier-1 venture backing, and a model that preserves the "local broker" trust factor that pure-play call-center eBrokers struggle to replicate.

- Independent Medicare brokers lacking capital for AI investment or scale face margin compression from three forces: (1) carrier commission cuts, (2) regulatory scrutiny of marketing practices, and (3) technology gap vs. well-capitalized platforms. Consolidation will accelerate.

- Traditional brokerage roll-ups (Hub International, BroadStreet Partners) must respond by acquiring or building AI capabilities—or accept that their "buy and standardize" playbook is being disrupted by "buy and augment" models.

Bottom line: Gyde proves that brokerage consolidation isn't dead—it's being rebuilt around AI infrastructure. The next wave of winners will preserve human relationships while automating everything else.

2. INDIGO — AI-Driven Medical Malpractice Underwriting

$50M | AI underwriting platform | Medical professional liability

Indigo's oversubscribed Series B marks a structural shift in medical malpractice insurance: proprietary AI (Lux platform) is now underwriting 20% of submissions automatically, achieving loss ratios competitive with century-old carriers while delivering quotes in minutes vs. days. Within 18 months of launch, Indigo insures nearly 1,000 physicians nationwide and surpassed $10 million in written premiums—growth velocity traditional carriers cannot match.

Why it matters

- Data flywheel advantage. Every physician Indigo underwrites feeds specialty-specific risk signals (procedure mix, patient demographics, peer benchmarking, historical claims patterns) back into Lux's machine learning models, improving predictive accuracy faster than competitors can respond. Traditional carriers relying on lagging actuarial tables updated quarterly cannot compete once Indigo reaches 10,000+ physician-years of data.

- Operational efficiency creates pricing power. Automated underwriting reduces cost per policy by 40–60% vs. manual review, allowing Indigo to profitably serve smaller practices and individual physicians that traditional carriers consider uneconomical due to high administrative cost.

- Strategic investor validation. Optum Ventures (UnitedHealth Group's VC arm) backing a medical malpractice platform signals that healthcare conglomerates view AI-driven liability insurance as critical infrastructure—potentially integrating malpractice coverage into broader physician risk management and value-based care models.

Competitive impact

- The Doctors Company, Coverys, MedPro Group, ProAssurance (traditional medical malpractice incumbents) face a three-front attack: (1) loss of low-touch, digitally native physicians to Indigo's faster quoting, (2) adverse selection risk as Indigo's AI cherry-picks low-risk profiles incumbents misprice, and (3) talent migration as top underwriters and brokers gravitate toward AI-enabled platforms.

- Broker economics shift. Indigo's digital-first distribution reduces broker dependency, pressuring wholesale and retail brokers to either (a) move upstream into true risk advisory (loss prevention, claims advocacy, practice management consulting) or (b) accept lower commission rates as digital channels commoditize policy placement.

- Acquisition clock starts. Within 36 months, Indigo becomes a strategic acquisition target for large diversified carriers (Chubb, Travelers, Zurich) or medical malpractice specialists seeking to acquire rather than build AI capabilities. Valuation estimate: $500M–$1B.

Bottom line: Medical malpractice is the canary in the coal mine. If AI can underwrite high-stakes, complex physician risk profitably, no specialty line is safe from algorithmic disruption.

3. ZOCKS — Agentic AI for Financial Advisors (and Insurance Agents)

$45M | AI workflow automation | Financial advisors, insurance agents

Zocks' $45M Series B (Lightspeed and QED co-led) positions the company as infrastructure for financial services distribution, automating meeting notes, client onboarding, account setup, and opportunity identification across 5,000+ financial firms. While not a pure-play insurance platform, Zocks' adoption by dual-licensed advisors (investment + insurance) and independent insurance agents makes it strategically relevant: it enables advisors to manage 3x larger client books while delivering proactive service (identifying clients with outdated life insurance, underinsured property, lapses in disability coverage).

Why it matters

- Distribution efficiency compounds. Advisors using Zocks save 10+ hours/week on administrative tasks, reallocating time to high-value advisory work (estate planning, insurance gap analysis, tax optimization). This productivity gain allows elite advisors to grow AUM and insurance premium volume without proportional headcount, improving economics vs. traditional advisory models.

- Enterprise adoption accelerates. Major broker-dealers and RIAs (Equitable Advisors, Osaic, Sequestra) deploying Zocks create network effects: as more advisors use the platform, integrations deepen (CRM, financial planning, portfolio management, insurance quoting systems), and switching costs increase.

- Insurance agents face adopt-or-decline decision. As AI-enabled advisors manage larger books and deliver superior client experience, traditional insurance agents lacking technology infrastructure will lose market share to dual-licensed advisors who bundle insurance with wealth management, retirement planning, and tax advisory.

Competitive impact

- Traditional insurance agents (captive and independent) relying on manual workflows face margin compression and client churn as AI-enabled competitors deliver faster service, proactive coverage reviews, and integrated financial planning.

- Insurance-focused workflow tools (Applied Epic, Agency Matrix, Hawksoft) face pressure to either (a) build or acquire agentic AI capabilities comparable to Zocks, (b) integrate with Zocks as a complementary layer, or (c) accept gradual displacement as advisors consolidate on fewer, AI-native platforms.

- Life insurance and annuity carriers benefit indirectly: Zocks' opportunity identification surfaces clients who need coverage updates, increasing policy sales volume through existing distribution without incremental marketing spend.

Bottom line: Financial services back-office automation is a $10B+ market opportunity. Zocks is becoming the system of work for advisors—and insurance agents either adopt or get left behind.

4. ORO — Employee Housing Benefits (with Insurance Embedded)

$3M | Employer-sponsored housing benefits | Homeowners insurance, mortgage insurance embedded

Oro's $3M seed (Slauson & Co. lead, Northwestern Mutual Future Ventures strategic) launches a new distribution channel for homeowners and mortgage insurance by embedding coverage into employer-sponsored housing benefits platforms. During pre-launch pilot, Oro helped eight employees become first-time homeowners and now supports 1,200+ employees across employer clients, positioning housing benefits as the "next evolution" of financial wellness alongside healthcare, student loan repayment, and mental wellness.

Why it matters

- Embedded distribution resets customer acquisition economics. Traditional homeowners insurance relies on retail agents, bank partnerships (forced-place insurance), or direct-to-consumer channels with CAC of $200–$500 per policy. Oro's employer-sponsored model accesses captive audiences (employees purchasing homes) with conversion rates 3x–5x higher and CAC below $100, fundamentally improving unit economics.

- Northwestern Mutual's strategic signal. As a $300B+ AUM life insurance and wealth management giant, Northwestern Mutual's investment indicates conviction that employer-sponsored housing benefits complement its core distribution model—advisors can deepen employer relationships and cross-sell life insurance, disability, and financial planning to employees utilizing housing benefits.

- Employer appetite for consolidated vendors. Employers seeking to simplify benefits administration prefer turnkey platforms (single vendor for housing assistance, mortgage referrals, insurance quoting, tax advisory) over fragmented point solutions, creating consolidation pressure across housing-adjacent services.

Competitive impact

- Traditional homeowners insurance retail agents face disintermediation risk as insurance quoting and enrollment embed directly into home-buying workflows, bypassing agents entirely.

- Mortgage lenders and title companies historically controlling homeowners insurance placement (via RESPA-compliant referrals) lose leverage as employer platforms bundle insurance with down payment assistance and mortgage education.

- Competitor housing benefit platforms (Landed, Gravy, Point) lacking insurance partnerships must either (a) partner with carriers to embed coverage, (b) white-label Oro's platform, or (c) concede insurance revenue to Oro and focus on mortgage/down payment services only.

Bottom line: If Oro scales to 10,000+ employers and 500,000+ employees, it becomes a meaningful homeowners insurance distribution channel—and incumbents either partner or compete for a shrinking pool of unaffiliated buyers.

5. STOÏK — European Cyber Insurance Consolidation Play

€20M (~$21.7M) | Cyber insurance + managed security | European SMEs

Stoïk's Series C (Impala and Opera Tech co-lead, Andreessen Horowitz participating) accelerates European cyber insurance consolidation. The company now protects 10,000+ businesses, generated €50M in gross written premiums in 2025, and grew 200% YoY across six countries with 2,000+ broker partners. Stoïk's bundled model—insurance + integrated cybersecurity prevention (managed EDR) + incident response (Stoïk-CERT)—creates switching costs and customer stickiness that traditional cyber carriers cannot replicate.

Why it matters

- Bundle creates defensibility. Customers depend on Stoïk's incident response capability, not just the insurance policy, making churn costly (replacing both insurance and security operations). This defensibility enables Stoïk to retain customers through market cycles and charge premium pricing vs. standalone cyber policies.

- SME market is underserved and large. European SMEs (revenues up to €1B) represent a €10B+ cyber insurance TAM, but traditional carriers struggle with SME economics (high distribution cost, low premium per policy, adverse selection). Stoïk's automated underwriting (replacing questionnaires with security assessments) solves the unit economics problem.

- Strategic acquisition target. 200% YoY growth, 10,000+ customers, and €50M GWP position Stoïk as a regional consolidation play. Large European insurers (AXA, Allianz, Zurich, Munich Re) seeking to enter or deepen SME cyber exposure may acquire Stoïk within 24–36 months at €300M–€500M valuation.

Competitive impact

- Traditional European cyber carriers (AIG, Chubb, Beazley, Coalition operating in Europe) face pressure on pricing, distribution efficiency, and value-added services. Stoïk's bundle model (insurance + prevention + response) shifts customer expectations: carriers offering insurance-only policies must either build or acquire adjacent capabilities.

- Regional cyber specialists lacking scale or bundled services face consolidation pressure—either acquired by Stoïk or larger players, or forced to niche down into specific verticals (financial services, healthcare, critical infrastructure).

- Broker economics change. Stoïk's 2,000+ broker partnerships create dependency: brokers selling Stoïk gain access to fast quotes and bundled services that improve close rates, but become reliant on Stoïk's platform and less willing to place business with traditional carriers lacking comparable digital workflows.

Bottom line: Stoïk is building the category-defining SME cyber platform in Europe. The question isn't if it gets acquired, but when and by whom.

6. XBUILD — AI Estimating for Property Claims

$19M | AI construction estimating | Property insurance claims

XBuild's Series A (N47 lead, Andreessen Horowitz participating) scales AI-driven construction estimating from roofing (initial focus) into HVAC, concrete, windows, and painting. In year one, XBuild processed 15,000+ projects worth $250M in construction volume, eliminating 40,000+ hours of manual estimation work—demonstrating clear ROI for carriers and contractors.

Why it matters

- Claims cycle time directly impacts customer satisfaction. Faster estimates accelerate claims settlement, reducing policyholder friction and improving Net Promoter Scores (NPS)—a critical competitive differentiator in commoditized homeowners insurance.

- Operational efficiency compounds at scale. Carriers processing 100,000+ property claims/year can eliminate 250,000+ hours of manual estimation (equivalent to 120+ FTEs), generating $10M–$15M annual cost savings and improving combined ratios by 1–2 points.

- Network effects from contractor adoption. As contractors adopt XBuild for estimating (faster proposal generation, integration with supplier pricing, project management workflows), carriers benefit from standardized estimates that reduce disputes and speed adjudication.

Competitive impact

- Legacy estimating software vendors (Verisk Xactimate, EagleView e-suite, CoreLogic) face disruption as AI-native platforms like XBuild deliver comparable accuracy at 50%+ lower cost and faster turnaround. Incumbents must either acquire AI capabilities or accept gradual displacement.

- Carriers and contractors lacking AI estimating face competitive disadvantage: slower claims cycles, higher operational cost, and lower customer satisfaction vs. competitors using XBuild.

- Third-party adjusters and estimating firms risk margin compression as automation reduces demand for manual estimation services, forcing them to move upstream into complex claims (litigation, large commercial losses) or accept smaller market share.

Bottom line: Property claims estimating is a $5B+ annual cost center for U.S. carriers. XBuild's 40,000+ hours saved in year one is a proof point—automation is now table stakes, not optional.

7. PACE — Agentic AI for Insurance Back-Office

$10M | AI operations automation | Insurance carriers, MGAs, brokers

Pace deploys agent-based AI to replace manual insurance operations (document processing, policy administration, claims coordination), enabling carriers and MGAs to reduce FTE requirements for administrative tasks by 30–50%. The $10M funds product scaling and enterprise carrier adoption.

Why it matters

- Labor cost is largest operational expense. For mid-size carriers and MGAs ($100M–$1B GWP), administrative labor represents 15–25% of operating expenses. A 30–50% FTE reduction generates $5M–$25M annual savings—enough to fund AI platform investment in 12–18 months.

- Margin compression forces automation. Carriers facing combined ratio pressure (rising claims severity, commission compression, regulatory cost) must reduce operational expenses to maintain profitability. Pace provides immediate ROI without requiring core system replacements.

- Talent scarcity accelerates adoption. Insurance operations roles (underwriting assistants, policy administrators, claims processors) face chronic talent shortages and high turnover. AI automation reduces dependency on hard-to-hire talent.

Competitive impact

- Carriers and MGAs lacking automation face margin disadvantage vs. competitors using Pace or similar platforms, creating consolidation pressure among smaller players unable to absorb technology investment.

- Brokers using Pace (or similar tools like Fulcrum) gain cost advantage, enabling them to either (a) cut fees and win on price, or (b) reinvest savings into service quality and differentiation.

- Legacy insurance software vendors (Vertafore, Applied Systems, Duck Creek, Guidewire) face pressure to either (a) build or acquire agentic AI capabilities, (b) partner with Pace as complementary layer, or (c) accept that next-generation platforms will bypass legacy systems entirely.

Bottom line: Insurance back-office automation is low-hanging fruit with measurable ROI. Carriers and MGAs not deploying agentic AI by end-2026 will face competitive disadvantage on cost and service speed.

8. MANTAS — Parametric Insurance for Cloud Downtime

$1.8M | Parametric cloud insurance | AWS, Azure, Google Cloud outages

Mantas offers parametric policies that trigger automatic payouts when cloud infrastructure experiences downtime, addressing a risk category traditional cyber and property policies exclude or undercover. The $1.8M seed funds product development and enterprise customer acquisition.

Why it matters

- Cloud downtime is uninsurable under traditional policies. Business interruption coverage requires physical loss or damage; cyber policies often exclude infrastructure outages caused by the cloud provider (vs. cyber attack). Mantas fills this gap with parametric triggers tied to public cloud SLAs.

- Enterprises need downtime protection at scale. A single hour of AWS outage can cost enterprises $1M–$10M+ in lost revenue, customer refunds, and SLA penalties. Parametric insurance provides immediate cash flow to offset losses without lengthy claims adjudication.

- Parametric model enables rapid scaling. No claims adjusters, no manual underwriting beyond initial risk assessment—policy triggers automatically based on public cloud status APIs, reducing operational cost and enabling capital-efficient scaling.

Competitive impact

- Traditional cyber and property carriers excluding cloud infrastructure risk face customer dissatisfaction as enterprises realize coverage gaps. Mantas positions itself as essential gap-filler that complements (not replaces) traditional policies.

- Specialty parametric insurers (Jump, Arbol, Descartes) focused on weather, supply chain, or event cancellation face potential competition if Mantas expands beyond cloud into adjacent parametric categories (payment processor downtime, logistics disruption, energy grid outages).

- Cloud providers (AWS, Azure, Google Cloud) offering SLA credits face customer pressure to either (a) partner with Mantas to offer bundled insurance, or (b) improve SLAs and uptime guarantees to reduce customer need for third-party coverage.

Bottom line: Parametric insurance for cloud downtime is a niche category today but could reach $500M–$1B in premium as cloud dependency deepens. Mantas is the early-mover specialist—but incumbents will notice if the market scales.

9. IGLOO — Embedded Insurance in Southeast Asia (Strategic Investment)

Strategic minority stake | Embedded insurance platform | Eight Southeast Asian markets

Tokio Marine's strategic investment in Igloo provides the Singapore-based embedded insurance platform with carrier backing, distribution partnerships, and product development support. Igloo distributes insurance through digital platforms (e-commerce, fintech, logistics, travel) across eight Southeast Asian markets.

Why it matters

- Embedded insurance reaches critical mass in Asia-Pacific. Igloo's Tokio Marine backing validates embedded insurance as a primary distribution channel (not experimental side project) in high-growth markets where digital-first consumers prefer bundled services over standalone insurance purchasing.

- Strategic carrier backing solves capacity and product constraints. Independent embedded insurance platforms struggle to secure carrier capacity and develop tailored products for platform partners. Tokio Marine's investment provides Igloo with guaranteed capacity, co-development resources, and distribution credibility.

- Asia-Pacific embedded insurance TAM is massive. Southeast Asia's 680M population, rapidly digitizing economy, and low insurance penetration (2–5% of GDP vs. 7–10% in developed markets) create $50B+ TAM for embedded insurance over next decade.

Competitive impact

- Traditional insurance agents in Southeast Asia face disintermediation as consumers purchase travel insurance via Grab, device protection via Lazada, and health micro-insurance via fintech apps—bypassing agents entirely.

- Competing embedded insurance platforms (CXA Group, Bolttech, Qoala) lacking strategic carrier partnerships face capacity constraints and must negotiate carrier relationships deal-by-deal, slowing product launches and increasing operational friction.

- Regional insurers without embedded strategies risk distribution obsolescence as digital platforms (e-commerce, fintech, mobility) control customer touchpoints and capture insurance revenue that historically flowed through agent channels.

Bottom line: Tokio Marine's Igloo investment is a strategic signal: large carriers view embedded insurance as essential distribution infrastructure in Asia-Pacific, not optional experimentation.

10. ETHOS TECHNOLOGIES — $200M IPO (Life Insurance Platform)

$200M IPO | Life insurance platform | Term and whole life

Ethos' Nasdaq debut (ticker: LIFE) marks the first major insurtech IPO of 2026, testing investor appetite for profitable insurtech businesses after years of private-market valuation reset. The company priced 10.5M shares at $19, valuing Ethos at $1.2B—60% below its 2021 peak of $2.7B. Trading opened at $16.84, down 11.4% on day one.

Why it matters

- Profitability validates insurtech as sustainable business model. Ethos reported $46.6M net income on $277.5M revenue (first three quarters of 2025), achieving 17% net margin—comparable to traditional life insurers and proving that digital-first life insurance can reach profitability at scale.

- Public markets remain skeptical of insurtech multiples. Despite profitability and 47% YoY revenue growth, Ethos trades at ~4.3x revenue vs. 10x–15x revenue multiples in 2021. This valuation compression reflects investor reassessment of insurtech TAM, competitive moats, and long-term margin profiles.

- Exit path for late-stage insurtechs. Ethos' successful IPO (raising $200M despite first-day trading weakness) demonstrates that profitable, scaled insurtechs can access public markets, providing exit alternative to strategic acquisition for companies achieving $200M+ revenue and positive cash flow.

Competitive impact

- Private insurtech peers (Lemonade, Root Insurance already public but struggling; Ladder, Bestow, others still private) face valuation pressure: if profitable Ethos trades at 4x revenue, loss-making peers must accept sub-3x revenue multiples or delay IPOs until profitability.

- Traditional life insurers (Northwestern Mutual, New York Life, MassMutual) gain validation that digital-first distribution is complementary to agent channels, not replacement—Ethos' profitability at scale proves digital acquisition can work without cannibalizing agent-driven premium.

- Life insurance agents face gradual market share erosion as digital-first platforms capture 5–10% of term life market over next 5 years, particularly younger, tech-savvy buyers preferring self-service digital journeys over agent consultations.

Bottom line: Ethos' IPO is a mixed signal—successful capital raise validates profitability and scale, but 60% valuation haircut and negative first-day trading reflect investor caution. Insurtech is viable, but no longer gets growth premiums.

11. TRUECAR — $227M Take-Private (Automotive Platform with Embedded Insurance)

$227M | Automotive marketplace | Embedded auto insurance via Zurich partnership

TrueCar's take-private transaction (founder Scott Painter-led, $2.55/share) includes strategic participation from Zurich North America (auto insurance) and In The Car (embedded insurance platform), signaling growing interest in embedded auto insurance distribution integrated into vehicle purchase workflows.

Why it matters

- Auto insurance at point-of-sale resets distribution economics. Traditional auto insurance relies on agents, direct-to-consumer advertising (GEICO, Progressive, State Farm TV/digital spend), or bank/dealer partnerships. TrueCar's embedded model intercepts customers earlier in purchase funnel (vehicle selection stage), enabling real-time quoting based on vehicle choice, driver profile, and financing terms—reducing CAC and improving conversion.

- Zurich's strategic participation validates embedded thesis. As a $70B+ global insurer, Zurich's investment indicates conviction that automotive marketplace platforms represent meaningful distribution channels for auto insurance, complementing traditional agent and direct channels.

- One-stop-shop experience improves customer satisfaction. Bundling vehicle search, financing (via PenFed Credit Union partnership), and insurance (via Zurich) into single workflow reduces friction, shortens purchase cycle, and increases customer lifetime value (LTV) per transaction.

Competitive impact

- Traditional auto insurance agents and direct-to-consumer carriers (GEICO, Progressive, State Farm) face disintermediation risk if embedded models capture 10%+ of new vehicle insurance placements (TrueCar touches ~10% of U.S. car buyers annually).

- Competing automotive marketplaces (CarGurus, Autotrader, Cars.com) lacking embedded insurance partnerships must either (a) partner with carriers to embed coverage, (b) white-label platforms like In The Car, or (c) concede insurance revenue to TrueCar and competitors.

- Auto dealers historically controlling insurance referrals (via F&I managers cross-selling GAP insurance, extended warranties) face channel conflict as embedded platforms offer insurance directly to consumers, bypassing dealer F&I departments.

Bottom line: If TrueCar generates $500M–$1B in auto insurance GWP through embedded distribution (achievable if 10%+ of transactions include insurance), it validates embedded auto insurance as viable alternative to traditional channels—forcing incumbents to respond or lose share.

12. SALVO HEALTH — $8.5M Series A (Hybrid GI Care with Insurance Integration)

$8.5M | Hybrid GI & metabolic care | Commercial insurance and Medicare coverage

Salvo Health's Series A (ManchesterStory and City Light Capital lead) scales a hybrid, AI-enhanced platform enabling brick-and-mortar gastroenterology (GI) practices to deliver continuous, multidisciplinary care (nutrition, behavioral health, nursing support) for chronic GI and metabolic conditions. The company partners with 801 GI providers (16% of independent U.S. gastroenterologists) and grew patients and revenue 800% YoY in 2025.

Why it matters

- Value-based care reduces total cost for payers. Salvo reports 79% reduction in GI-related ER utilization and 76% patient symptom improvement—metrics that translate to lower medical costs for commercial insurers and Medicare Advantage plans. If scaled, Salvo's model could reduce annual GI-related spending (estimated $100B+) by 10–20%, generating billions in savings for payers.

- Commercial insurance and Medicare coverage validates reimbursement model. Salvo care is covered by major commercial insurers and Medicare, indicating that payers view continuous GI care as medically necessary and cost-effective vs. episodic specialist visits and ER utilization.

- Women's health and mental health adjacency expands TAM. 83% of Salvo patients are women; many GI conditions co-occur with anxiety, depression, and metabolic disorders. Salvo's platform could expand into broader women's health and behavioral health categories, increasing TAM from GI ($100B+) to integrated women's health ($300B+).

Competitive impact

- Traditional telehealth platforms (Teladoc, Amwell) offering episodic virtual visits face competitive pressure from Salvo's hybrid model, which preserves brick-and-mortar relationships while layering continuous care—delivering superior outcomes and retention vs. standalone virtual care.

- GI practices without continuous care capabilities risk patient attrition to Salvo-enabled competitors offering integrated nutrition, behavioral health, and nursing support that improve outcomes and patient satisfaction.

- Commercial insurers and Medicare Advantage plans seeking to reduce GI-related medical costs may mandate or incentivize Salvo participation, creating network effect as more GI practices adopt the platform to remain in-network.

Bottom line: Salvo's 800% YoY growth and enterprise agreements with three of the four largest U.S. GI practices position it as category leader in GI-specific virtual care infrastructure. If outcomes data continues validating ER reduction and symptom improvement, Salvo becomes essential infrastructure for value-based GI care.

Competitive Landscape: Cross-Sector Displacement Dynamics

The AI Divide: Winners vs. Laggards

Winners (AI-Native Platforms):

- Gyde, Indigo, Zocks, Pace, XBuild achieve operational efficiency and customer experience improvements traditional competitors cannot match without wholesale technology rebuilds.

- Cost advantages: 30–60% lower operational cost per transaction/policy through automation.

- Customer experience: Quotes in minutes vs. days; proactive opportunity identification; self-service workflows.

- Data moats: Each transaction improves AI models, creating compounding accuracy and pricing advantages.

Laggards (Manual Workflow Dependency):

- Traditional carriers, brokers, and agents lacking AI capabilities face margin compression, customer churn, and talent migration to AI-enabled competitors.

- Strategic choices: (1) acquire AI platforms, (2) partner/white-label, (3) build in-house (expensive, slow), or (4) accept market share erosion.

Vertical Specialization Wins

Medical Malpractice (Indigo): Specialty-specific risk models outperform generalist carrier models.

Medicare Brokerage (Gyde): Product expertise, carrier relationships, and regulatory workflows create defensibility vs. horizontal platforms.

Startup Insurance (Corgi, prior weeks): Vertical focus builds data moat and underwriting expertise unmatched by generalist carriers.

Implication: Horizontal generalists (traditional multi-line carriers, broad-based brokers) lose share to vertical specialists with deeper expertise and AI tailored to segment-specific risk factors.

Embedded Distribution Disrupts Standalone Channels

TrueCar + Zurich + In The Car: Auto insurance embedded in vehicle purchase.

Oro + Northwestern Mutual: Homeowners insurance embedded in employer housing benefits.

Igloo + Tokio Marine: Insurance embedded in e-commerce, fintech, logistics platforms.

Implication: Standalone insurance agents and brokers face disintermediation as purchasing embeds into adjacent workflows (vehicle buying, home buying, benefits enrollment, financial planning). Distribution advantage shifts from agent relationships to platform integrations.