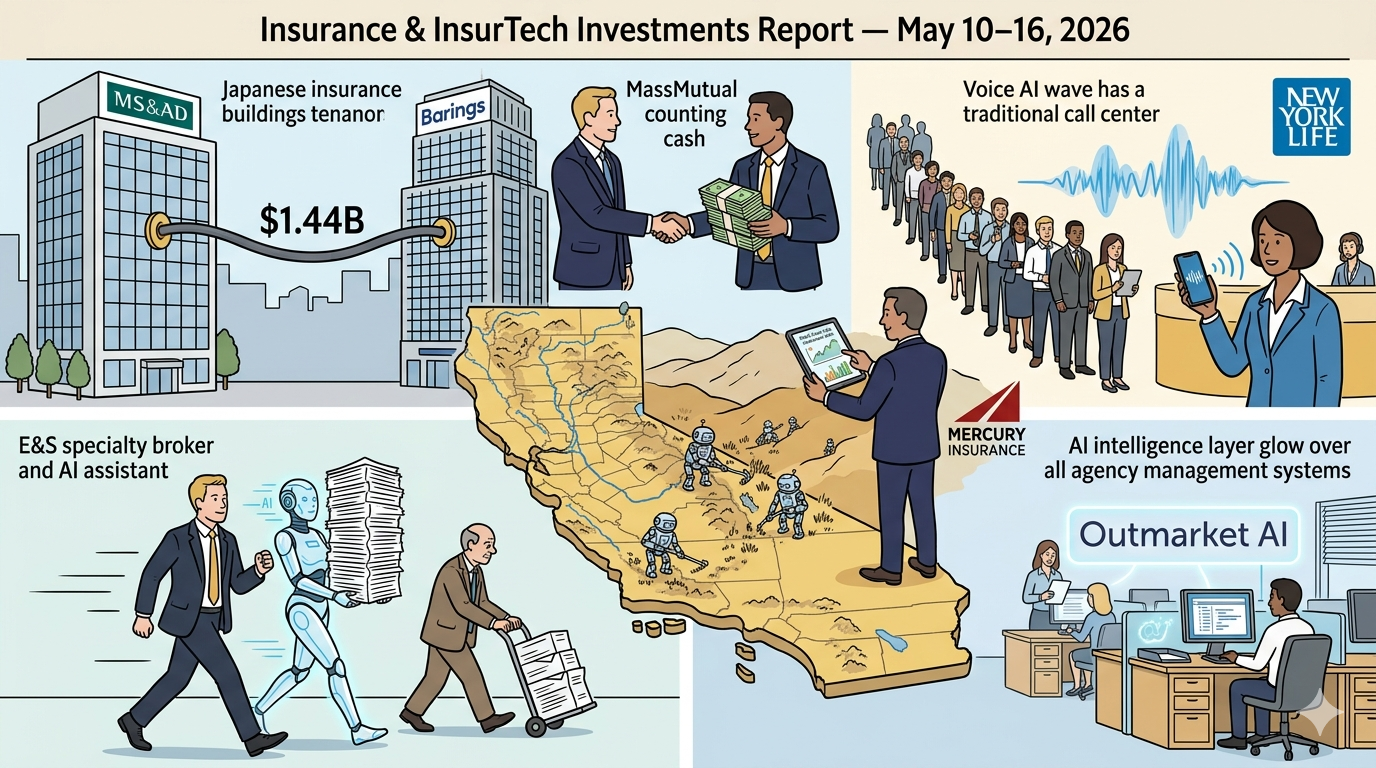

## Week of May 10–16, 2026

$1.75B+ disclosed | 7 transactions | Largest capital week of 2026

The week's headline number is $1.75 billion — but the composition is more important than the total. Three distinct capital themes converged simultaneously: AI is being embedded into the distribution layer of insurance (Novella, Outmarket AI, Vapi), carriers are moving upstream into physical risk reduction rather than just pricing for it (Mercury/BurnBot), and the global insurance-asset management convergence is producing its largest single transaction of the year (MS&AD/Barings). The brokerage consolidation machine continues in the background — Shepherd and ALPS both added scale quietly. This is not a week of isolated deals. It is a week where three structural shifts in insurance all moved at once.