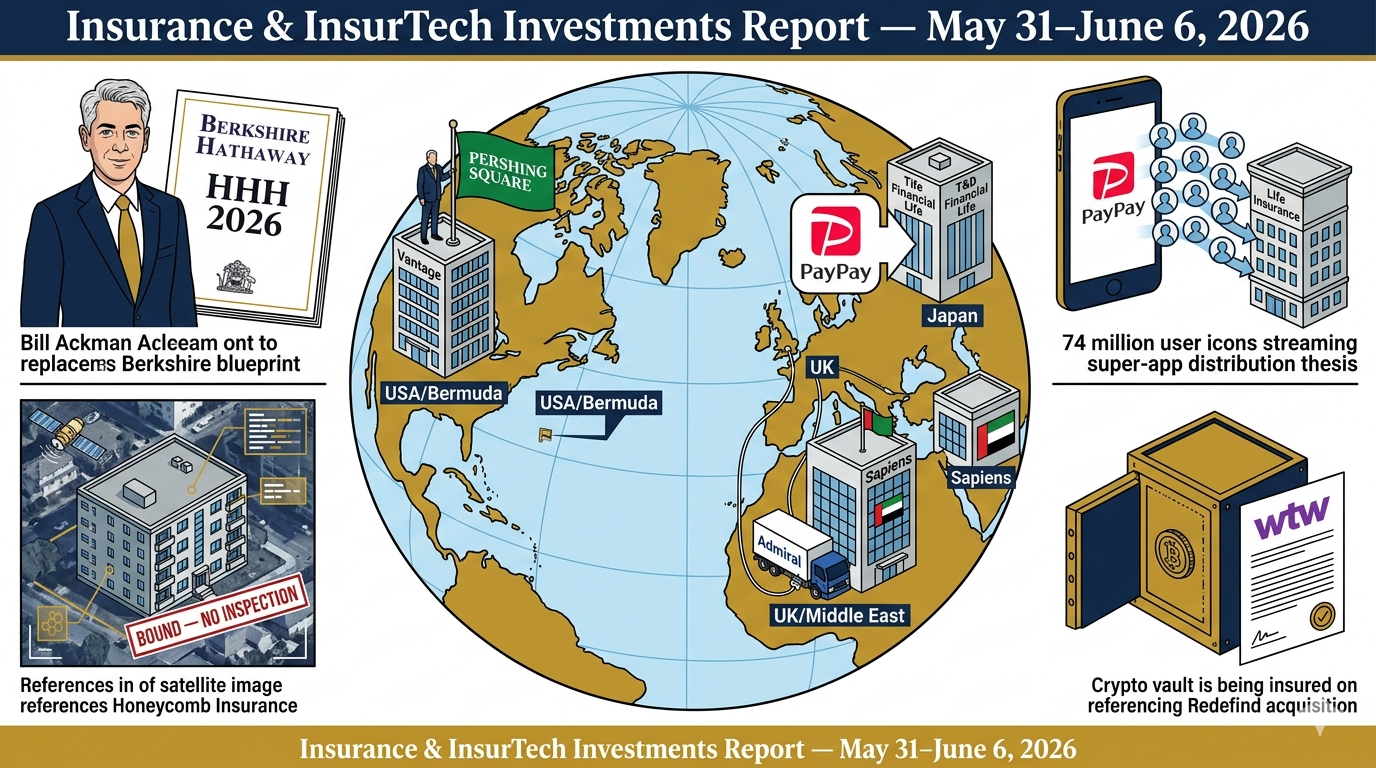

$3.1B+ in disclosed investment activity | 6 transactions | The week the insurance industry went global

Four countries. Three continents. One week. The Howard Hughes / Vantage close marks Bill Ackman's formal entry into specialty insurance as a capital compounder. PayPay's ¥134B acquisition of T&D Financial Life brings 74 million Japanese app users to the doorstep of life insurance — with SoftBank's distribution machine behind it. ADIA investing in Sapiens signals Abu Dhabi sovereign wealth entering insurance software at scale. Admiral completing its Flock acquisition absorbs AI-native fleet telematics directly into one of the UK's largest motor insurers. WTW acquiring Redefind puts the world's largest advisory broker into crypto insurance infrastructure. And Honeycomb raises $40M to underwrite apartment buildings without sending a human to the site. The unifying thesis: insurance is becoming a platform business, absorbing technology and capital from categories it has never competed in before.

1. Howard Hughes Holdings / Vantage Group Holdings (USA / Bermuda)

$2.1B Acquisition Close | Bill Ackman's Berkshire Thesis — Specialty Reinsurance as Capital Compounder Date: June 4, 2026

What Happened

Howard Hughes Holdings Inc. (NYSE: HHH) closed its previously announced $2.1 billion all-cash acquisition of Vantage Group Holdings Ltd., a Bermuda-based specialty insurance and reinsurance company backed by Carlyle Group and Hellman & Friedman. The transaction was announced December 18, 2025. Vantage was founded in 2020 and scaled rapidly into a diversified specialty insurer, reinsurer, and partnership capital organization. HHH Executive Chairman Bill Ackman (Pershing Square Capital Management) is the architect of the deal — explicitly framed as the foundation of HHH's transformation into a diversified holding company modeled after Berkshire Hathaway. Financing: HHH cash on hand plus $1 billion non-voting exchangeable perpetual preferred stock issued to Pershing Square Holdings, Ltd. (LSE: PSH). Additionally, HHH committed a $200 million capital infusion to Vantage at close to reinforce the insurer's balance sheet and underwriting flexibility. Pershing Square Capital Management assumes management of Vantage's investment portfolio on a fee-free basis — a deliberate policyholder-alignment signal. Greg Hendrick (CEO of Vantage) continues in the role. Former Arch Capital CEO Marc Grandisson joins HHH's Board. HHH Insurance Holdings, LLC is the acquiring subsidiary.

- Acquirer: Howard Hughes Holdings Inc. (NYSE: HHH) — Bill Ackman, Executive Chairman

- Target: Vantage Group Holdings Ltd. — specialty insurer/reinsurer, founded 2020

- Sellers: Carlyle Group + Hellman & Friedman (exiting sponsors)

- Investment manager for Vantage portfolio: Pershing Square Capital Management (fee-free)

Use of Funds

- Carlyle and H&F receive exit proceeds after a six-year build

- HHH deploys $2.1B plus $200M capital infusion to anchor specialty insurance platform

- Pershing Square manages Vantage investment portfolio — expected to compound toward equity investments over time, subject to rating agency and regulatory constraints

Strategic Thesis

This is the Berkshire Hathaway blueprint applied by someone who has studied it closely and said so explicitly. Ackman's thesis: a specialty insurance platform generates a float that, when invested by a world-class capital allocator at no fee, compounds far faster than a conventional insurer. Vantage provides the underwriting platform — disciplined specialty P&C and reinsurance, modern infrastructure, advanced analytics. Pershing Square provides the investment management — fee-free, aligned, with a documented track record. HHH provides the balance sheet and the public market vehicle. The $200M capital infusion at close is the signal that Ackman intends to grow Vantage's underwriting capacity, not merely hold it. Marc Grandisson's board appointment brings the institutional credibility of Arch Capital's builder directly into HHH's governance — the most respected specialty insurance executive in Bermuda, signaling to the market that this is a serious underwriting enterprise, not a financial engineering exercise.

Why It Matters

- The Berkshire Hathaway float model — invest insurance float at compounding returns through disciplined capital allocation — is the most value-creative structure in financial services history; Ackman is now explicitly executing it with a next-generation specialty platform

- Fee-free investment management from Pershing Square is the key structural detail: every basis point of investment return goes to policyholders and shareholders, not to Pershing Square — an alignment signal that traditional insurer-asset manager structures cannot match

- Marc Grandisson's board appointment is institutional credibility validation from the person who built Arch Capital from a post-9/11 startup into a $30B+ specialty insurance leader — the exact playbook Ackman is attempting to replicate

Competition

- Direct comparable structures: Markel Corporation (underwriting + Markel Ventures), Fairfax Financial (underwriting + equity investments), W.R. Berkley, RenaissanceRe

- Category competitors: Bermuda-class specialty reinsurers (Arch, RenaissanceRe, Everest Re, Axis Capital)

- Emerging competitive dynamic: Other capital allocators — hedge fund managers, family offices, PE firms — studying the HHH/Vantage structure as a template for entering specialty insurance

Market Consequences

HHH/Vantage establishes a new category of specialty insurance competitor: the capital allocator-owned specialty platform. The competitive advantage is not underwriting edge alone — it is investment return on float, compounded at Pershing Square's historical performance, at zero fee drag. Traditional Bermuda specialty reinsurers (Arch, Everest, Axis) compete for the same risks but manage their investment portfolios conventionally. Over a five-to-ten year horizon, the float investment differential compounds significantly. Carlyle and H&F's exit after six years validates both the Vantage underwriting model and the Bermuda specialty re/insurance valuation environment — two institutions that have deployed capital across every sector chose specialty insurance as a compelling return category. The transaction represents one of the largest recent exits for a Bermuda-founded re/insurance company and signals continued PE confidence in the sector's fundamentals.

Bottom line: Bill Ackman just built a Berkshire Hathaway. The float is Vantage's specialty underwriting. The investment manager is Pershing Square. The fee is zero. That structure, compounded over a decade, is extraordinarily difficult to compete against.

2. PayPay / T&D Financial Life Insurance (Japan)

¥134.3B (~$840M) | 70.2% Stake Acquisition — 74 Million Users Enter Life Insurance Date: June 4, 2026 (agreement; closing targeted October 1, 2027)

What Happened

PayPay Corporation — Japan's dominant cashless payment service, a subsidiary of SoftBank Corp., with 74 million registered users as of May 2026 — announced its acquisition of a 70.2% stake in T&D Financial Life Insurance Company from T&D Holdings, Inc. for ¥131,985 million ($825M) in cash consideration, with total estimated investment including expenses of ¥134,338 million ($840M). The remaining ownership: OneIM Indigo Holdings Ltd. (affiliate of One Investment Management, led by former SoftBank executive Rajeev Misra) acquires 14.9%; T&D Holdings retains 14.9%. T&D Financial Life had ordinary revenue of ¥912,827 million ($5.7B) and net income of ¥8,221 million ($51M) in FY ended March 2026 — net income nearly doubled from ¥5.6B the prior year. The company holds 3% of Japan's life insurance market by premium share, with total assets of ~¥1.96 trillion ($12.2B). Closing targeted October 1, 2027, subject to regulatory approvals and T&D Financial Life's IFRS accounting transition. Post-deal, PayPay has a call option on additional shares and T&D Holdings has a put option after three years.

- Acquirer: PayPay Corporation (SoftBank subsidiary)

- Target: T&D Financial Life Insurance Company (70.2% stake)

- Seller: T&D Holdings, Inc.

- Co-investor: OneIM Indigo Holdings (14.9%)

Use of Funds

- T&D Holdings receives ~¥132B in cash, concentrating strategic focus on Taiyo Life and Daido Life core operations

- PayPay deploys life insurance across its existing payments, banking, credit card, and securities infrastructure for 74M users

- T&D Financial Life gains SoftBank technology resources (AI in call centres, health and senior-care initiatives) and PayPay's digital distribution capabilities

Strategic Thesis

Japan has approximately ¥15 trillion in household financial assets — vast, aging, and historically intermediated through complex offline distribution. PayPay has 74 million registered users and already delivers payments, banking, credit cards, and securities to a digitally active base. Adding life insurance completes the "super-app" financial services stack — the same trajectory WeChat Pay, GrabPay, and other Asian super-apps have executed across Southeast Asia. The strategic insight is demographic: Japan's "100-year life era" creates structural demand for long-term financial protection products, and PayPay reaches exactly the generation that will need them but has been underserved by traditional agency distribution. T&D Financial Life's ¥912B in ordinary revenue is not the prize — it is the license, the product shelf, and the regulatory infrastructure. PayPay provides the 74 million users and the digital delivery mechanism that traditional insurance companies cannot build from scratch. Rajeev Misra's OneIM co-investing alongside PayPay — at 14.9% — is the signal that this transaction has SoftBank's broader strategic network behind it, not just PayPay's balance sheet.

Why It Matters

- 74 million PayPay users represents approximately 60% of Japan's working-age population — the distribution reach for embedded life insurance is immediate and unprecedented in Japanese insurance history

- T&D Financial Life's net income nearly doubling year-over-year demonstrates that the underlying insurance operations are in excellent health — PayPay is not acquiring a distressed asset but a growing platform

- The IFRS transition requirement is the only meaningful condition precedent — once completed, it removes the accounting complexity that has historically made T&D Financial Life difficult to integrate into a digitally-native parent

Competition

- Direct competitors (Japan life insurance digital distribution): Rakuten Life Insurance (backed by Rakuten ecosystem), LINE Insurance, au Insurance (KDDI)

- Category competitors: Japan Post Insurance, Nippon Life, Dai-ichi Life, Meiji Yasuda Life — the traditional career agency-based incumbents

- Structural dynamic: Every major Japanese super-app (Rakuten, LINE, au/KDDI) is building an insurance distribution layer; PayPay's acquisition of a full carrier position (vs. distributor-only models) creates a structural difference

Market Consequences

Traditional Japanese life insurance distribution — the career agent system that has powered the industry for 70 years — faces a direct structural challenge from PayPay's 74 million user touchpoints. The career agent model is expensive, aging, and shrinking; PayPay's digital distribution is zero-marginal-cost per additional user and reaches consumers where they already transact daily. Nippon Life, Dai-ichi Life, and Meiji Yasuda all operate excellent carrier platforms but have struggled to build equivalent digital distribution reach. T&D Holdings' decision to sell a controlling stake — retaining 14.9% with a put option — is a rational capital allocation decision: monetize the distribution challenge, remain a beneficiary of the upside, and refocus on Taiyo Life and Daido Life where the career agency model remains strong.

Bottom line: Japan's largest payments app just bought a life insurer. 74 million users now have access to embedded life insurance through the app they use to buy coffee. The career agent model's decades-long structural decline just accelerated.

3. Honeycomb Insurance (USA / Israel)

$40M Series C | AI-Native Insurer for Apartment Buildings and Condo Associations Date: June 4, 2026

What Happened

Founded in 2019 by Itai Ben-Zaken (CEO) and Nimrod Sadot (President), Chicago-based Honeycomb Insurance is an AI-native property and casualty insurer specializing in apartment buildings and condo associations — the multi-unit residential commercial real estate segment. Honeycomb underwrites without physical site inspections, ingesting hundreds of data points per property from geospatial datasets, aerial imagery, and building history to price each risk individually. Exited 2025 with $275 million in gross written premium. Currently insures over $100 billion in assets. Offers coverage up to 40% cheaper for well-maintained buildings that traditional carriers overcharge or decline. The $40M Series C brings total funding to $95M.

- Lead investor: Zeev Ventures (Oren Zeev, Founding Partner — previously backed Houzz, TripActions, Papaya Global)

- Existing investors: Ibex Investors (follow-on)

- New investors: Peakline, Alpha Partners, Meitar Partners, Practical VC, Harris Barton (former San Francisco 49ers NFL champion)

Use of Funds

- Accelerate geographic coverage across additional U.S. states

- Improve agent-facing tools and distribution infrastructure

- Expand product offerings beyond apartment buildings and condo associations

- Enhance proprietary AI-driven underwriting platform

Strategic Thesis

Commercial real estate insurance for multi-unit residential properties — apartment buildings, condo associations, HOA boards — is a category where traditional carriers have two structural problems: they cannot price individual buildings accurately at scale (their models are aggregate, not building-specific), and their unit economics require physical site inspections that make small and mid-size buildings uneconomical to underwrite. Honeycomb's AI platform solves both: every building gets an individual risk profile built from aerial imagery and geospatial data, without a human inspection, at any scale. The result is a carrier that can offer materially lower premiums on well-maintained buildings (because the model can see they're well-maintained) while declining or pricing accurately the poorly-maintained ones that traditional carriers bundle together. $275M in gross written premium by end of 2025 — at $95M in total capital — is exceptional capital efficiency for an insurance carrier at this stage. Oren Zeev's framing — "an insurance company that has scaled rapidly while maintaining a lean operation... exceptionally rare in insurance" — is the investment thesis in one sentence.

Why It Matters

- $275M in gross written premium at $95M total capital raised is exceptional capital efficiency for a licensed insurance carrier — proof that the no-inspection AI underwriting model works at commercial scale, not just in pilots

- The 40% premium discount on well-maintained buildings relative to traditional carriers is a structural pricing advantage, not a competitive pricing strategy — it reflects superior risk selection, not margin sacrifice

- $100B+ in insured assets establishes Honeycomb as a significant market participant in commercial real estate insurance, not an early-stage startup

Competition

- Direct competitors: Steadily (landlord insurance), Goodcover, traditional commercial property carriers offering apartment programs (Lloyd's, Markel, Westfield)

- Category competitors: E&S property programs, regional commercial carriers, surplus lines platforms for multi-family

- Emerging competitive dynamic: Corgi (startup/commercial lines AI carrier), Shepherd (AI construction underwriting) — all represent AI-native full-stack carriers attacking different commercial property verticals simultaneously

Market Consequences

Traditional commercial property carriers underwriting apartment buildings face a competitor that prices individual buildings more accurately, charges less for better-maintained ones, and does not require physical inspections to generate a quote. The unit economics advantage is structural: Honeycomb's cost per underwritten building is a fraction of a traditional inspection-based workflow. At $275M GWP, Honeycomb is still a small participant in a market measured in hundreds of billions. But the growth trajectory — lean team, AI underwriting, no inspections, material price advantage on well-maintained assets — is the geometry of a market share capture story that compounds on itself. For agents and brokers serving landlords and condo associations, Honeycomb offers a carrier relationship that produces faster quotes and better prices for quality buildings — a straightforward distribution value proposition.

Bottom line: Honeycomb underwrites apartment buildings from satellite imagery without sending anyone to the property. It's 40% cheaper for well-maintained buildings. $275M in premium and $95M in total capital. That is not a venture story. That is an insurance company.

4. WTW / Redefind (UK / Global)

Undisclosed | Acquisition — Crypto Insurance Infrastructure Date: June 2, 2026

What Happened

WTW (NASDAQ: WTW) announced the acquisition of Redefind, a UK-based end-to-end web-based platform enabling individuals and institutions to purchase insurance for cryptocurrency and digital assets across all forms of custody. Redefind's founders Richard Daws (CEO) and Connor Edward joined WTW upon completion. Terms undisclosed. The platform uses cryptographic proof of ownership to make previously uninsurable digital assets insurable. Coverage model: non-custodial, cost-of-recovery — covering forensic investigation costs, asset tracing, and legal recovery expenses following digital asset theft or loss, rather than the market value of the assets themselves. Initially launching in the UK; broader market and product expansion planned. WTW reported Q1 2026 net income up 27% year-on-year to $303M, revenue up 8% to $2.41B, and EBITDA of $589M — a strong financial platform from which to execute this acquisition. This follows WTW's earlier 2026 acquisition of Newfront ($1.05B) as part of a systematic technology-forward strategy.

- Acquirer: WTW (Willis Towers Watson), via GB Affinity practice (Anthony Borgman, Head of GB Affinity; Alastair Swift, Head of Global Specialities)

- Target: Redefind — UK-based crypto insurance platform

- Founders retained: Richard Daws, Connor Edward

Use of Funds

- WTW deploys Redefind's platform through its Affinity practice and global distribution network

- Redefind gains WTW's carrier relationships, regulatory standing, and global client access

- UK launch immediately; global expansion to follow

Strategic Thesis

WTW's acquisition of Redefind is a calculated bet on timing, not technology. The crypto insurance market is projected at $9.5B in 2025 and growing at approximately 45% CAGR. The market is real, growing, and currently underserved: digital asset holders — institutions and individuals — have historically struggled to obtain credible, regulated insurance coverage because traditional policy structures cannot address the proof-of-ownership and cost-of-recovery challenges specific to digital assets. Redefind's cryptographic proof-of-ownership infrastructure solves the coverage eligibility problem that has kept traditional insurers out of this category. WTW is buying the platform and the technical foundation at a moment when institutional crypto adoption (Bitcoin ETFs, tokenized assets, stablecoin infrastructure) is making crypto insurance a mainstream enterprise procurement question rather than a niche request. The cost-of-recovery model — covering investigation and legal expenses rather than asset value — is the correct product design for a category where asset values are volatile: it avoids the moral hazard and adverse selection problems that have historically made crypto insurance uneconomical.

Why It Matters

- Cryptographic proof of ownership is the technical breakthrough that makes this category insurable at scale — Redefind built the infrastructure layer that no traditional broker has internally

- WTW's global Affinity distribution network and carrier relationships are the commercial accelerant: Redefind's platform can now be distributed to WTW's institutional and corporate client base immediately

- The cost-of-recovery model avoids the underwriting problems that have kept carriers out of direct crypto insurance (volatile asset values, adverse selection) — a structurally sound product design that is scalable and reinsurable

Competition

- Direct competitors: Coincover, Evertas (crypto-focused MGA), Marsh's digital asset practice, Aon's crypto coverage programs

- Category competitors: Lloyd's syndicates with digital asset appetite (Chaucer, Hiscox), specialist MGAs, self-insurance by large exchanges and custodians

- Emerging dynamic: As Bitcoin ETFs and tokenized assets become standard institutional portfolio components, every major broker will require a credible crypto insurance offering — WTW has moved first with purpose-built infrastructure

Market Consequences

Competing brokers — Marsh, Aon, Gallagher — will now face a WTW that has a proprietary technology platform for crypto insurance distribution, not just a coverage arrangement. The difference matters: WTW can iterate on the Redefind product architecture, expand coverage categories, and deepen cryptographic proof capabilities. Competitors without equivalent technology infrastructure are distribution channels, not platform owners. For crypto exchanges, custodians, and institutional digital asset managers that have struggled to obtain credible insurance coverage, WTW/Redefind represents the first broker-led solution with regulated infrastructure — the procurement conversation just became simpler. For Lloyd's syndicates currently writing crypto risks on bespoke arrangements, WTW's standardized platform creates both a distribution partner and eventually a competitive pressure on terms.

Bottom line: WTW just built the insurance infrastructure for the crypto economy. The timing — as institutional adoption reaches critical mass — makes this a market-defining move, not an experimental one.

5. Admiral Group / Flock (UK)

£80M (~$102M) Acquisition Close | AI Telematics Fleet Insurance Absorbed into Major Carrier Date: June 1, 2026

What Happened

Admiral Group (LSE: ADM) completed its previously announced acquisition of Flock, a UK-based digital commercial fleet insurance MGA with an AI-powered telematics platform. The deal was originally announced February 12, 2026, and closed following regulatory approval on June 1. The transaction values Flock's equity at £80M (~$102M). Ed Leon Klinger (Flock CEO) joins Admiral Pioneer's leadership team. As part of the close, Admiral becomes Flock's sole capacity provider — taking over from Acorn (taxi, since 2024) and Intact Insurance (fleet, since 2023, formerly Intact's first fleet business). Flock has built a digital platform using proprietary AI risk models trained on hundreds of millions of miles of real-world driving data, enabling usage-based insurance and safety rewards for commercial fleet operators across taxis, haulage, vans, and larger fleets (25+ vehicles). Since the announcement, Admiral has already launched its first major segment expansion — a new haulage fleet insurance product — demonstrating integration speed.

- Acquirer: Admiral Group (via Admiral Pioneer — the Group's venture-building subsidiary)

- Target: Flock — digital commercial fleet MGA, founded 2017 by Ed Leon Klinger

- Departing capacity providers: Acorn (taxi), Intact Insurance (fleet)

Use of Funds

- Admiral absorbs Flock's technology platform, team, and AI risk models into its commercial motor operations

- Flock expands product range under Admiral's balance sheet (haulage already launched)

- Admiral Pioneer uses Flock as its anchor fleet telematics capability for commercial motor growth

Strategic Thesis

Admiral's UK Insurance business insures approximately six million motorists — predominantly personal lines. Commercial motor (fleets, taxis, haulage) is the natural growth adjacency, and Admiral has historically lacked the fleet-specific data infrastructure to price it competitively against specialist carriers. Flock's AI models, trained on hundreds of millions of real driving miles, fill that gap immediately — providing Admiral with the usage-based underwriting capability for commercial fleets that would have taken years to build internally. The Admiral Pioneer structure is instructive: it piloted the partnership with Flock before acquiring it, using a venture-building model to validate the product-market fit and technology integration before committing £80M. That's the correct sequencing for a large carrier acquiring an AI-native MGA — pilot, validate, acquire, scale.

Why It Matters

- Flock's AI risk models were trained on hundreds of millions of real driving miles — a dataset that cannot be replicated without years of operating experience; Admiral acquires that dataset alongside the platform

- The immediate haulage product launch post-close demonstrates that the integration playbook is working at speed — Admiral is not running a two-year integration process, it is immediately expanding into new fleet segments

- Intact departing as capacity provider at close is the natural consequence of an MGA being acquired by a carrier — but it raises a question about Intact's commercial motor fleet strategy in the UK

Competition

- Direct competitors (UK fleet telematics insurance): Zego (van and fleet), By Miles, Veygo, Zurich Fleet (commercial motor division)

- Category competitors: Traditional fleet insurers (RSA, Zurich, Allianz) without equivalent telematics data infrastructure

- Carrier acquisitions of fleet insurtechs: Root (U.S., telematics personal auto), Nationwide/SmartRide — Admiral's Flock acquisition follows the same strategic logic in commercial motor

Market Consequences

Specialist UK fleet insurers — Zurich Fleet, RSA Commercial, Allianz Commercial — now face a competitor that has the data infrastructure to price commercial fleets on actual observed driving behavior, not historical actuarial tables. Admiral's six million personal motor customers provide a natural cross-sell base for fleet and commercial motor products, particularly for small businesses that already insure their personal vehicles with Admiral. The departure of Intact as Flock's capacity provider is a net negative for Intact's UK commercial motor fleet exposure — they lose a growing flow of fleet business that was scaling under Flock's platform. For UK fleet operators evaluating telematics-based insurance, Admiral/Flock is now the largest carrier-backed option available.

Bottom line: Admiral bought Flock's six years of driving data and AI risk models for £80M. Haulage products are already live. That is acquisition integration done correctly — and it signals Admiral's commercial motor ambitions are real.

6. ADIA / Sapiens International (Netherlands / Global)

Undisclosed | Abu Dhabi Sovereign Wealth Fund Becomes Significant Minority Shareholder in Insurance Software Leader Date: June 1, 2026

What Happened

Sapiens International Corporation N.V. (NASDAQ: SPNS) announced that a wholly owned subsidiary of the Abu Dhabi Investment Authority (ADIA) has invested in Sapiens and become a significant minority shareholder. Financial terms not disclosed. This investment follows Sapiens' acquisition by Advent International (global PE firm) in 2025. Alongside the ADIA investment, Sapiens announced: relocation of its global headquarters to Space House, Holborn, London (which also functions as an AI Customer Experience Lab); launch of its Insurance Agentification programme — AI tools for automating workflows across underwriting, claims, and policy management (products: Agentic Claims, Agentic Underwriting, Agentic Policy, built on a Central Agentic Framework with a governed insurance ontology); and plans for a second AI Customer Experience Lab in the U.S. focused on North American insurance markets later in 2026. Sapiens serves 600+ insurance companies globally. Douglas Hallstrom (Managing Director, Advent) confirmed the investment as a "further step in Sapiens' growth under Advent's ownership and the acceleration of its AI strategy for the insurance sector."

- Investor: ADIA (Abu Dhabi Investment Authority) — wholly owned subsidiary

- Existing majority owner: Advent International

- Sapiens leadership: Ron Zuckerman (CEO, confirmed continuing)

Use of Funds

- Accelerate AI strategy, including Insurance Agentification programme buildout

- Expand teams, products, and operating infrastructure globally

- Support new London HQ and U.S. AI Customer Experience Lab development

Strategic Thesis

ADIA is one of the world's largest sovereign wealth funds, managing an estimated $1 trillion+ in assets. Its investment in Sapiens is not a small PE transaction — it is a sovereign wealth fund taking a significant minority position in the dominant global provider of insurance operating software. The strategic logic: insurance technology infrastructure at scale has the characteristics ADIA seeks — recurring revenue from mission-critical systems with high switching costs across 600+ global carrier clients, secular growth from digital transformation and AI adoption, and a global footprint that benefits from diversified insurance market exposure. Advent's ownership provides the governance and operational oversight; ADIA provides the capital depth and sovereign-grade long-term holding horizon. The Insurance Agentification launch timing is deliberate — Sapiens is announcing sovereign backing at the same moment it launches its AI product offensive, signaling to 600+ carrier clients that the company has the capital and commitment to lead the insurance AI transition.

Why It Matters

- ADIA becoming a significant minority shareholder in Sapiens is a vote of confidence from one of the world's most sophisticated institutional investors in insurance software as a durable, compounding asset category

- The Insurance Agentification programme — Agentic Claims, Agentic Underwriting, Agentic Policy — positions Sapiens not just as a core system provider but as the AI orchestration layer that sits above those systems

- The London HQ move and U.S. AI lab announcement signal a deliberate global expansion acceleration — Sapiens is not consolidating, it is expanding its geographic footprint in the same week it announces sovereign capital backing

Competition

- Direct competitors: Guidewire Software, Duck Creek Technologies, Majesco, Insurity (core insurance systems)

- Category competitors: Accenture/Everest insurance consulting implementations, Salesforce Financial Services Cloud for insurance, ServiceNow insurance workflows

- Emerging dynamic: Blitzy (autonomous software development), Pace (AI operations agents), and Notch (AI governance for insurance) are all building adjacent layers that compete with Sapiens' agentic ambitions from below

Market Consequences

Guidewire and Duck Creek — the two dominant U.S. P&C core system vendors — now face a better-capitalized, ADIA-backed competitor with a global footprint and an explicit AI product offensive. Sapiens' 600+ carrier clients globally provides the deployment base for rapid Insurance Agentification adoption — if Agentic Claims and Agentic Underwriting gain traction, Sapiens captures the AI workflow layer above its existing core systems, deepening the moat and compressing the window for standalone AI agent competitors. For insurance carriers currently deciding whether to build or buy AI operations infrastructure, ADIA's investment in Sapiens is a market signal: the vendor with the deepest existing core system relationships and sovereign backing is the safest long-term partner for AI workflow investment.

Bottom line: Abu Dhabi's sovereign wealth fund just backed the world's largest insurance software company. The Insurance Agentification programme now has sovereign capital behind it. That is a different competitive statement than another VC round.