$1.97B+ in disclosed investment activity | 6 transactions | Valuation compression, AI operations, and a Korean insurer's American arrival

The week's defining story is not any single deal — it is the speed at which the insurance capital market is moving. Corgi doubled its valuation in three weeks and raised again. Pace attracted Thrive Capital, Sequoia, and PruVen Capital to an AI operations platform that didn't exist eighteen months ago. Nationwide absorbed a $16 billion Universal Life block from MassMutual without adding staff. DB Insurance completed the first acquisition of a U.S. insurer by a Korean carrier in history. And Great-West Lifeco committed $150M to an AI fund alongside Power Corporation. Every one of these transactions would have been the headline deal of its week in any prior year. This week they happened simultaneously.

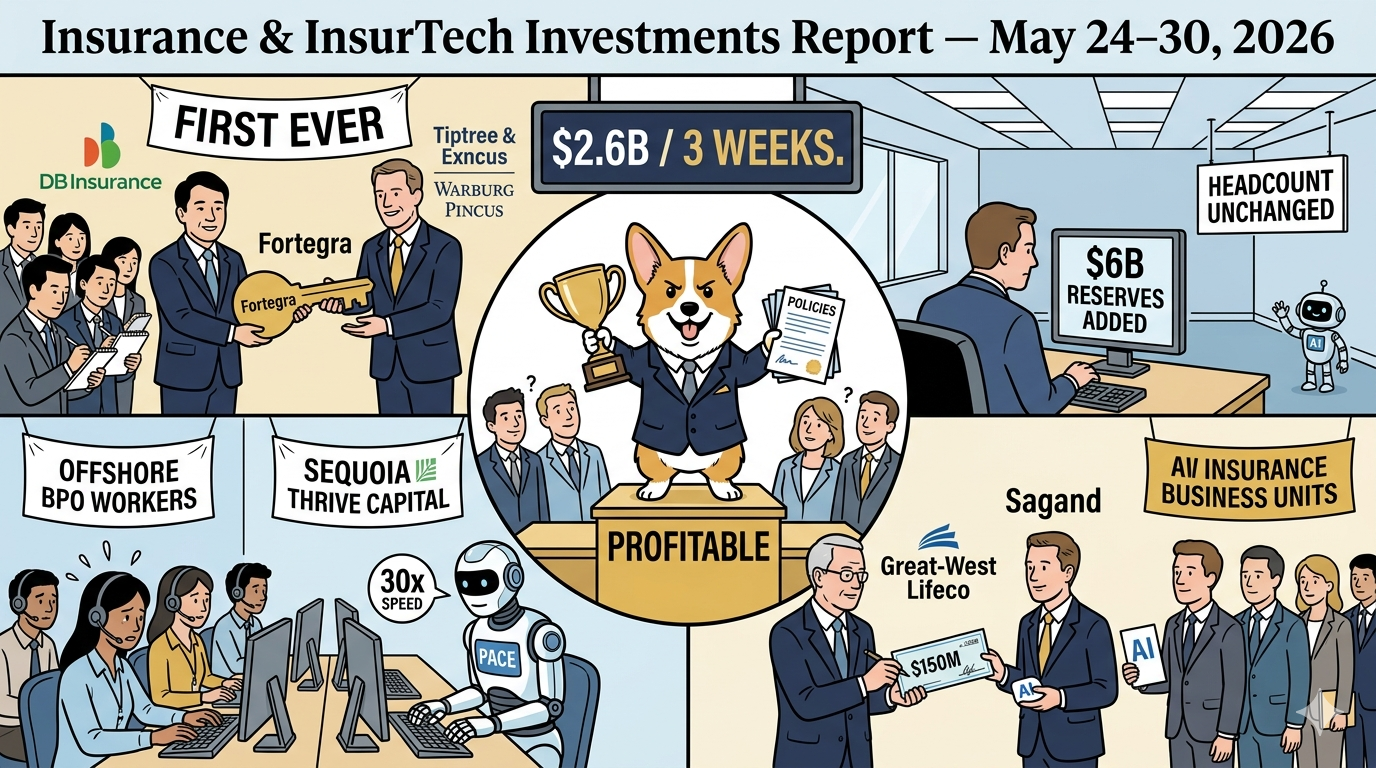

1. Fortegra / DB Insurance (USA / South Korea)

$1.65B Acquisition Close | First U.S. Insurer Acquisition by a Korean Carrier Date: May 29, 2026 (closed)

What Happened

The Fortegra Group, a Jacksonville, Florida-based specialty insurer founded 1978, was acquired by DB Insurance Co., Ltd. — South Korea's leading property and casualty insurer — for $1.65 billion in cash. The deal was originally announced September 26, 2025, received shareholder approval in December 2025 (81% of votes cast), and closed May 29, 2026. Sellers: Tiptree Inc. (NASDAQ: TIPT, majority holder) and Warburg Pincus (minority). Fortegra will operate independently as a wholly owned subsidiary of DB Insurance under existing leadership. Richard Kahlbaugh (Chairman and CEO of Fortegra) and Michael Barnes (Chairman and CEO of Tiptree) both confirmed Fortegra will pursue geographic expansion into U.S., Europe, UK, and Asia under DB's capital umbrella. Fortegra reported $3.07B in gross written premiums and $140M net income in its last full reporting year. Ki-Hyun Park, Head of Global Business at DB Insurance, described the deal as "the first-ever purchase of a U.S. insurer by a Korean non-life insurer."

- Acquirer: DB Insurance Co., Ltd. (Korea's largest non-life insurer)

- Sellers: Tiptree Inc. (majority) + Warburg Pincus (minority)

- Financial advisors: Wells Fargo (MassMutual/Tiptree exclusive financial advisor), Sidley Austin LLP (Nationwide legal counsel), Skadden (MassMutual legal), Oliver Wyman (actuarial)

Use of Funds

- Tiptree receives ~$1.12B estimated gross proceeds, strengthening its balance sheet and enabling a new $20M share repurchase program

- DB Insurance gains a U.S. specialty insurance platform for global expansion beyond Korea

- Fortegra retains capital backing to pursue geographic expansion across U.S., Europe, and Asia

Strategic Thesis

This is the Korean insurance market's arrival on the global M&A stage. DB Insurance is Korea's largest non-life insurer — a dominant domestic player with capital strength and global ambitions but no established U.S. footprint. Fortegra provides exactly what a Korean carrier needs for international expansion: a proven U.S. specialty platform with $3B+ in gross written premiums, established carrier relationships, and a management team that built it. The structure — Fortegra operating independently under existing leadership — signals DB Insurance has bought a platform to grow, not a book to integrate and rationalize. For Tiptree and Warburg Pincus, the exit represents the culmination of a multiyear build-and-scale strategy in specialty insurance that generated strong returns. The deal is historic not for its size but for what it represents: the globalization of the U.S. specialty insurance M&A market has begun.

Why It Matters

- This is the first acquisition of a U.S. insurer by a Korean non-life carrier — a market precedent that signals Asian insurance capital's readiness and capacity to compete for U.S. specialty assets

- Fortegra's $3.07B GWP and $140M net income give DB Insurance an immediately material U.S. operating presence, not a foothold — it arrives as a significant player

- The structure (independent operation, existing management retained) is the correct template for cross-border specialty insurance acquisitions, where carrier relationships and distribution trust are the primary assets

Competition

- Direct competitors (U.S. specialty insurer acquirers): Ryan Specialty, Markel, Arch Capital, W.R. Berkley — all competing for the same specialty program and distribution assets

- Category competitors: Other Asian carriers evaluating U.S. specialty acquisitions — Tokio Marine (already active in U.S.), MS&AD (via Mitsui Sumitomo stake in W.R. Berkley), Sompo (Philadelphia Consolidated acquisition history)

- Emerging dynamic: Korean financial institutions accelerating overseas M&A as domestic market saturation increases — DB Insurance, Hanwha, Samsung Fire & Marine all studying international acquisition targets

Market Consequences

The precedent matters more than the deal itself. Korean insurance capital has now demonstrated it can complete a major U.S. specialty acquisition from announcement through regulatory approval through close. The playbook exists. The deal structures are understood. The regulatory pathways have been navigated. Other Korean carriers — Hanwha Life, Samsung Fire & Marine, KB Insurance — will study this transaction closely. For U.S. specialty insurance assets, Asian carrier capital is now a credible, active, and well-capitalized competing buyer alongside the established PE-backed and strategic acquirers. That expands the buyer universe and, structurally, supports valuations for well-run U.S. specialty platforms.

Bottom line: DB Insurance just wrote the playbook for Korean carrier expansion into U.S. specialty insurance. Every Korean non-life insurer with global ambitions is reading it this week.

2. Nationwide / MassMutual — $16B Universal Life Reinsurance Block

$16B Face Value Block Reinsurance | Life Insurance Capital Optimization Date: May 28, 2026 (announced)

What Happened

Nationwide has reached an agreement with MassMutual to reinsure a block of fixed Universal Life insurance policies with secondary guarantees. The block covers more than 30,000 policyowners with a total face value of nearly $16 billion and will increase Nationwide Financial's reserves by $6 billion. The transaction is expected to close in Q2 2026. MassMutual will continue administering the policies and remain the policyholder point of contact. Nationwide expects to absorb the block without adding staff — a statement about AI and operational efficiency as much as capital capacity. Kirt Walker (CEO of Nationwide) and Craig Hawley (President of Nationwide Financial) made the announcement. Nationwide was designated the third largest life insurance writer in the U.S. in 2025. Additionally, Nationwide has appointed Barings — a MassMutual subsidiary — as one of its investment managers for this specific block, adding a third dimension to the relationship. Legal counsel: Skadden (MassMutual), Sidley Austin (Nationwide). Financial advisor: Wells Fargo (MassMutual).

- Reinsurer (assuming risk): Nationwide Financial

- Cedant (transferring risk): MassMutual

- Investment manager for the block: Barings LLC (MassMutual subsidiary)

Use of Funds

- MassMutual optimizes capital allocation, freeing reserve capacity for other uses

- Nationwide deploys its strong capital position into reserve growth, adding $6B without adding headcount

- Barings gains a new investment management mandate, deepening the MassMutual-Nationwide relationship

Strategic Thesis

This is the life insurance industry's capital optimization machine running at full speed. MassMutual holds a block of Universal Life policies with secondary guarantees — a capital-intensive, long-duration liability that consumes significant reserves. Offloading the risk to Nationwide's balance sheet through reinsurance frees capital that MassMutual can redeploy into higher-return activities while retaining the customer relationship and administration revenue. Nationwide, with its strong capital position and life insurance scale ambitions (third largest U.S. writer in 2025), gets $6B in reserve growth and a demonstration that it can absorb major blocks efficiently. The Barings appointment as investment manager is the most strategically interesting element: it ties the MassMutual-Nationwide relationship together across three dimensions — cedant, reinsurer, and asset manager — creating a durable, mutually reinforcing commercial relationship that is hard to unwind and creates alignment for future transactions.

Why It Matters

- The Barings investment management appointment confirms the MassMutual-Nationwide-Barings trilateral relationship established with MS&AD's $1.44B Barings investment two weeks ago — Barings is rapidly becoming the institutional asset manager at the center of major life insurance capital transactions

- "Without adding staff" is a direct statement about Nationwide's operational AI and automation maturity — a $6B reserve increase absorbed at existing headcount implies technology-enabled capacity that competitors running manual operations cannot match

- For Universal Life policyowners: MassMutual retains administration and remains the point of contact — the policyholder relationship is preserved even as the underlying risk is transferred

Competition

- Competing life reinsurers: Reinsurance Group of America (RGA), Munich Re Life, SCOR Life, Global Atlantic (KKR), Athene (Apollo), Pacific Life

- Category dynamic: Block reinsurance transactions are accelerating as carriers manage long-duration UL liabilities under LDTI accounting changes — Nationwide is positioning as an active acquirer of these blocks

Market Consequences

Life carriers holding large UL blocks with secondary guarantees are watching this transaction closely. MassMutual demonstrates the mechanics of a clean block transfer: policyholder continuity, management retained, capital optimization achieved. The LDTI accounting change (effective for large public companies FY2023, now embedded) has made UL block reserve requirements more volatile and more capital-intensive. Carriers with well-positioned balance sheets — Nationwide, Athene, Global Atlantic — will increasingly compete for these blocks. Those with weaker capital positions who hold large UL liabilities will face growing pressure to transact. Barings' appointment as investment manager on the block adds a commercial intelligence layer: Barings gains real-time visibility into the performance of Nationwide's reserve portfolio, which informs both its asset management decisions and its parent MassMutual's future transaction appetite.

Bottom line: MassMutual recycled $6B in reserve capacity without losing a single policyholder relationship. Nationwide added $6B in reserves without adding a single staff member. This is what mature capital optimization looks like in life insurance.

3. Corgi (USA)

$106M Series B1 at $2.6B Valuation | AI-Native Full-Stack Carrier — Second Raise in Three Weeks Date: May 28, 2026

What Happened

Corgi Insurance Services announced a $106 million Series B1 round at a $2.6 billion valuation — exactly three weeks after its $160 million Series B at a $1.3 billion valuation on May 6. Total capital raised is now $378 million across seed, Series A, Series B, and Series B1 since the company's founding. Founded by Nico Laqua (CEO) and Emily Yuan (COO, former OpenAI product manager). Customers include Deel and Artisan. Nico Laqua disclosed in conjunction with the announcement that Corgi was profitable last month — the first public profitability claim from the company. New verticals named for expansion: trucking (previously announced), small business, and sports. Embedded insurance capabilities are being built to allow other platforms to offer Corgi-underwritten coverage directly.

- Lead investor: TCV (same lead as Series B three weeks prior)

- Participating investors: Prime Capital, Zone 2 Ventures, Oliver Jung, Leblon Capital, Kindred Ventures, Quadri Ventures, First Order Fund, Vocal Ventures, Nordstar, GSBackers, Repeat Ventures, 8188 Capital

Use of Funds

- Continued expansion of full-stack insurance platform into trucking, small business, and sports verticals

- Build out embedded insurance capabilities for platform distribution

- Accelerate modernization of commercial insurance infrastructure

Strategic Thesis

The valuation doubling in three weeks demands a direct explanation — and TechCrunch asked it directly. Investor Kanyi Maqubela of Kindred Ventures cited "momentum." The more structural answer: Corgi disclosed profitability, and a profitable AI-native full-stack carrier at $378M in total capital with $2.6B valuation and multiple expansion verticals is a genuinely different investment thesis than the same company at $1.3B three weeks earlier. Profitability changes the risk profile fundamentally. An AI-native insurer that is already generating more than it spends — in an industry where most challengers require years of loss-funded growth — suggests the underlying unit economics of AI-native underwriting are working. The embedded insurance expansion is the second strategic signal: Corgi is no longer only a direct carrier; it is building the infrastructure for other platforms to distribute Corgi-underwritten coverage, which creates a B2B2C channel that compounds without proportional customer acquisition cost.

Why It Matters

- Profitability disclosed at this scale and this stage is rare in insurtech — it changes the risk-adjusted investment thesis and justifies the accelerated valuation step-up

- Three raises in five months ($108M Series A, $160M Series B, $106M Series B1) with the same lead investor (TCV) across both B rounds signals extraordinary conviction, not momentum investing

- The embedded insurance buildout positions Corgi as distribution infrastructure, not just a carrier — the addressable market expands from commercial insurance customers to every platform that wants to offer commercial coverage to its users

Competition

- Direct competitors: Vouch Insurance, Next Insurance, Embroker, Coalition (D&O/cyber overlap)

- Category competitors: Traditional commercial carriers (Chubb, Hartford, Nationwide), commercial MGAs

- Emerging competitive dynamic: Coalition, Cowbell, and At-Bay have also raised at aggressive valuations — but none has disclosed profitability at this stage or raised at this velocity

Market Consequences

TechCrunch's observation that "the investor set in both rounds is the same" and the valuation doubling "is unusual enough to raise questions" is fair — but the profitability disclosure is the answer to those questions. A profitable AI-native carrier that is also building embedded distribution infrastructure is pursuing a market structure, not a market share. The commercial insurance market is $500B+ in U.S. premium. Corgi at $2.6B valuation and profitable represents less than 0.5% of that. The runway is not the question. The pace of execution is. Every quarter Corgi sustains profitability while expanding verticals, the traditional carrier case for why an AI-native full-stack model doesn't work gets harder to make.

Bottom line: Corgi was profitable last month. That sentence changes everything about the investment thesis — and explains the valuation doubling that three weeks alone cannot justify.

4. Pace (USA)

$46M Series B | AI Operations Platform for Insurers (PruVen Capital + Thrive + Sequoia) Date: May 27, 2026

What Happened

Founded by Jamie Cuffe (CEO and Founder), Pace is a New York-based AI operations platform for insurers and brokers. Founded 2024. The platform deploys AI agents that navigate internal insurance applications, reason across documents, and conduct phone calls to automate back-office workflows — submission intake, policy servicing, claims handling, and data entry. Since launching last year, Pace has autonomously completed more than 250,000 critical insurance workflows. Live production clients include Prudential Financial, WTW (Willis Towers Watson), The Mutual Group, and Newfront. At Prudential, Pace automates thousands of hours of manual work across policy servicing and issuance. In partnership with Ryze Claim Solutions, Pace has cut claim cycle times by 30%. At Convex US, AI agents accelerate data ingestion for new business and renewals. The company launched last year with a $10M Series A from Sequoia Capital (announced January 2026 via Fortune).

- Co-leads: Thrive Capital + Sequoia Capital

- Participating investors: Emergence Capital, PruVen Capital (watchlist hit — PruVen is one of the 35 tracked funds)

Use of Funds

- Scale AI agentic workforce to tens of millions of insurance operations tasks in 2026

- Expand from U.S. into Europe and global markets

- Deepen production deployments across Prudential, WTW, Mutual Group, Newfront

Strategic Thesis

Pace is attacking insurance's $70 billion back-office outsourcing market — the BPO spend that carriers and brokers route to offshore operations centers for manual processing of submissions, policy changes, claims intake, and data movement. Jamie Cuffe's framing is precise: "The Internet gave rise to outsourcing. Now AI can do what was being outsourced offshore." The insight is not new, but Pace's execution evidence is unusually strong for a company launched eighteen months ago: 250,000+ autonomous workflow completions, Prudential as a live production client, and a 30% claims cycle time reduction at Ryze Claim Solutions are outcomes, not pilots. Thrive Capital and Sequoia co-leading is the institutional signal — Thrive's Philip Clark described the moment as when "the most important high-value parts of the knowledge economy are being augmented and automated." PruVen Capital's participation links Pace directly to the multi-insurer LP syndicate behind PruVen — carriers including TIAA, Lincoln Financial, Mutual of Omaha, and Nippon Life whose operations teams are the exact buyers of what Pace sells.

Why It Matters

- PruVen Capital participating connects Pace to the insurance carrier LP network behind PruVen — TIAA, Lincoln Financial, Mutual of Omaha, Nippon Life, Generali, WTW are all Pace's natural enterprise customers, and PruVen's investment creates a direct commercial pathway

- 250,000+ autonomous workflow completions from a company founded eighteen months ago demonstrates production-scale AI operations in live insurance environments — this is not a demo, it is a deployed system

- Sequoia backing Pace's Series A (January 2026) and co-leading its Series B (May 2026) — four months later — is an extremely fast graduation that signals extraordinary production performance data in between

Competition

- Direct competitors: Gradient AI, Ushur, Unqork (insurance workflow automation), Duck Creek Technologies

- Category competitors: Offshore BPO providers (Conduent, EXL Service, WNS Holdings — all serving insurance back-office), internal RPA implementations (UiPath, Automation Anywhere deployed at carriers)

- Emerging dynamic: Reserv (claims-focused, KKR-backed, $100M ARR) and Pace (operations-broad, Sequoia/Thrive-backed) are converging on adjacent problem sets from different angles

Market Consequences

Offshore BPO providers serving insurance — Conduent, EXL Service, WNS Holdings — face a direct structural threat. Their model: charge per FTE-equivalent for manual processing. Pace's model: deploy AI agents that complete the same tasks faster, cheaper, and with full auditability at a fraction of the per-unit cost. Carriers that have historically justified offshore BPO on cost grounds now have a domestic AI alternative that reduces cycle time, improves data quality, and eliminates the offshore compliance complexity. PruVen's involvement accelerates carrier adoption through its LP network. For carriers not yet evaluating AI-native operations platforms, the Prudential and WTW reference sales are now the market benchmark — a board question about why equivalent deployments haven't been initiated is a predictable consequence.

Bottom line: Pace is automating the $70 billion that insurance currently pays humans to move data around. Prudential and WTW are already live. The offshore BPO providers that serve insurance back-offices just got their Reserv moment.

5. Great-West Lifeco / Sagard AI Fund (Canada)

$150M Combined Investment | Carrier-Anchored AI Fund for Financial Services Date: May 20, 2026

What Happened

Power Corporation of Canada, Great-West Lifeco Inc. (TSX: GWO), and IGM Financial Inc. (TSX: IGM) announced a combined US$150 million investment in the newly established Sagard AI Fund LP — a closed-end vehicle focused on backing AI companies accelerating adoption across financial services and other sectors. Paul Desmarais III is Sagard's Chairman and CEO. Evan Kerr has joined Sagard as general partner to lead the fund, having previously served as a lead investor at Georgian (Toronto-based growth capital). Parinaz Sobhani, former head of AI at Georgian, joined Sagard two years prior in a similar capacity. Sagard manages more than $46 billion in assets across venture capital, private equity, private credit, and real estate. The fund will provide the Power group with AI market intelligence, commercial partnership opportunities, pilot projects, and application opportunities across its group of companies — Great-West Lifeco (insurance, retirement, wealth), IGM Financial (wealth and asset management), and other Power subsidiaries.

- Investors: Power Corporation (anchor), Great-West Lifeco Inc., IGM Financial Inc.

- Fund GP: Sagard (Paul Desmarais III, Chairman/CEO; Evan Kerr, General Partner)

- Total combined commitment: US$150 million

Use of Funds

- Back AI companies accelerating adoption across financial services globally

- Provide Power group access to AI market intelligence and commercial partnerships

- Enable pilot projects and application opportunities across Great-West, IGM, and other Power subsidiaries

Strategic Thesis

Great-West Lifeco is Canada's largest life insurer with $3.3 trillion in total client assets and approximately 40 million customer relationships globally through Irish Life, Empower Retirement, and Canada Life. The $150M Sagard AI Fund is not a passive financial investment — it is an intelligence network and a commercial sourcing mechanism. The Power group is deploying capital into a fund structure managed by its own alternative asset arm (Sagard) to gain proprietary access to the AI companies most relevant to insurance, wealth management, retirement, and financial advice — the exact verticals where Great-West and IGM compete. This is Northwestern Mutual's Fund III thesis (capital plus distribution access) applied at the Canadian insurance conglomerate level. The Evan Kerr appointment — from Georgian, which backs AI-first enterprise software companies — ensures the fund is sourcing from the right networks. Paul Desmarais III's stated position — "being a firm that stays in the status quo is not going to work in the future" — is an unusually direct acknowledgment from a major traditional insurer that the competitive threat from AI adoption is existential, not incremental.

Why It Matters

- Great-West Lifeco's $3.3T in client assets makes it one of the largest insurance and retirement platforms in the world — an AI fund anchored by this distribution scale offers portfolio companies commercial access that pure-VC-backed competitors cannot match

- The Georgian DNA (Evan Kerr, Parinaz Sobhani) signals a deliberate strategy to source AI companies at the intersection of enterprise software and financial services — where insurance AI is converging

- The combined Power Corporation structure — insurer (Great-West) + wealth manager (IGM) + alternative asset manager (Sagard) — creates a deployment channel for AI portfolio companies that spans the entire financial services value chain

Competition

- Comparable carrier-led AI funds: Northwestern Mutual Future Ventures Fund III ($150M, April 2026), MS&AD Ventures ($100M Fund V), Allianz X (~€1.5B total)

- Pure-play insurtech VCs: Anthemis, Brewer Lane, MTech Capital — all lacking equivalent distribution channel access

Market Consequences

Canadian insurance technology ecosystem gains a major anchor investor with direct deployment access. AI companies in enterprise fintech and insurtech now have another carrier-backed fund competing for their growth rounds — with a distribution channel spanning 40 million customers globally. For traditional Canadian life insurance competitors (Sun Life, Manulife, iA Financial), a Great-West-backed AI fund sourcing and piloting technology across all financial services verticals represents an accelerating competitive AI capability gap. Sun Life's Sun Life Asia Ventures and Manulife's investment activities are smaller and less systematically structured than the Sagard AI Fund's mandate.

Bottom line: Canada's largest life insurer just launched the Northwestern Mutual Fund III playbook — capital plus a 40-million-customer distribution channel. The AI companies that get into this portfolio don't just get funding. They get a go-to-market.

6. Benefitbay (USA)

$18M Series A | Broker-First ICHRA Platform Date: May 21, 2026

What Happened

Founded by Brandy Thompson (Founder and CEO), Kansas City-based benefitbay® is a leading Individual Coverage Health Reimbursement Arrangement (ICHRA) platform serving top brokerages, employers, and employees nationwide. The company closed an $18 million Series A led by Ten Coves Capital. Alongside the financing, Kevin Mullins was named President and CFO. The company has more than 40,000 covered lives on its platform, approximately 60 employees, and 40% year-over-year employee growth. Also disclosed: a prior investment from KCRise Fund III in late March. Ten Coves Capital, the lead investor, backed HealthEquity from early growth through its 2014 IPO — the most relevant prior investment for validating the ICHRA infrastructure thesis.

- Lead investor: Ten Coves Capital (Darien, CT — growth equity, fintech/insurance/benefits focus)

- Participating investors: KCRise Fund III (Kansas City regional VC, prior round)

- Prior investors: Right Side Capital Management, Comeback Capital, Allos Ventures, Invest Nebraska, Nelnet Ventures

Use of Funds

- Expand payments infrastructure underpinning ICHRA reimbursement flows

- Add direct carrier and payroll integrations

- Enhance broker enablement tools — the primary distribution channel

Strategic Thesis

ICHRA is the structural answer to the group health insurance cost crisis. Traditional group premiums have outpaced employer absorption capacity for a decade. ICHRA converts the employer obligation from "pick a group plan and pay the premium" to "define a contribution amount and let employees shop." The employer controls cost. The employee gains choice. The broker gains a new advisory category. Benefitbay is the infrastructure layer that makes ICHRA operationally viable at scale — handling the reimbursement flows, carrier integrations, compliance documentation, and broker enablement that ICHRA requires but that no legacy system was built to support. Brandy Thompson built this company around the infrastructure problem, not the consumer acquisition problem. Ten Coves' track record backing HealthEquity — the HSA infrastructure company that grew from private to a $7B+ public company — is the exact analogical investment thesis: the infrastructure layer for a new account-based benefits category, not the consumer product sitting on top of it.

Why It Matters

- ICHRA adoption is accelerating among large employer groups — benefitbay reports that large brokerages are now building dedicated ICHRA practices and bringing 1,000-life-and-above groups to market, a significant scale threshold

- Ten Coves' HealthEquity track record is the most relevant prior investment in the benefits infrastructure category — the managing partners understand how infrastructure companies in this space compound in value

- The broker-first positioning is strategically correct — ICHRA requires broker advocacy and implementation expertise; bypassing brokers (as some pure DTC ICHRA platforms attempt) forfeits the distribution channel that brings employers to the product

Competition

- Direct competitors: Zorro (ICHRA platform), Take Command Health, PeopleKeep, SANA Benefits

- Category competitors: Traditional group health plan administrators (Alight, HealthEquity, Benefitfocus), PBMs attempting to extend into defined contribution health

- Emerging dynamic: As ICHRA adoption scales, the dominant infrastructure provider will have network effects from carrier relationships and payroll integrations — benefitbay is building that layer first

Market Consequences

For traditional group health insurers — Cigna, UnitedHealth, Aetna, Anthem — ICHRA adoption represents a structural threat to the group premium revenue model. As employers shift from defined benefit to defined contribution health, the carrier relationship migrates from employer-driven to employee-driven. The incumbent carriers built for the group model face a channel fragmentation that requires entirely different distribution, product, and pricing infrastructure. For brokers, ICHRA represents an advisory services opportunity rather than a placement fee — a potentially higher-margin relationship if platforms like benefitbay provide the operational infrastructure that makes broker ICHRA practices scalable.

Bottom line: ICHRA is the defined contribution revolution coming for group health insurance. Benefitbay is building the infrastructure layer for it — with the investor that backed HSA infrastructure from seed to IPO.