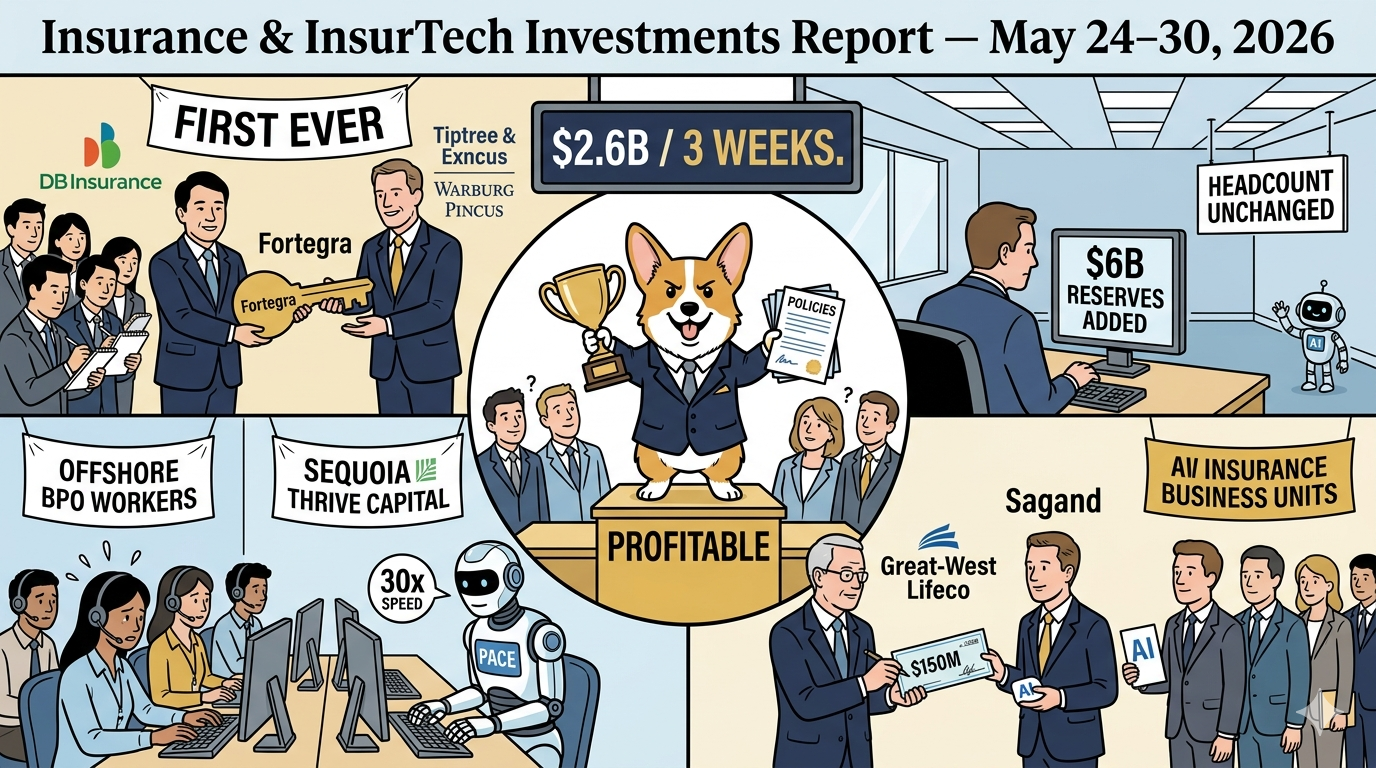

Six deals. $1.97B deployed. A Korean insurer made history. An AI carrier turned profitable. Nationwide absorbed $6B in reserves without hiring a single person.

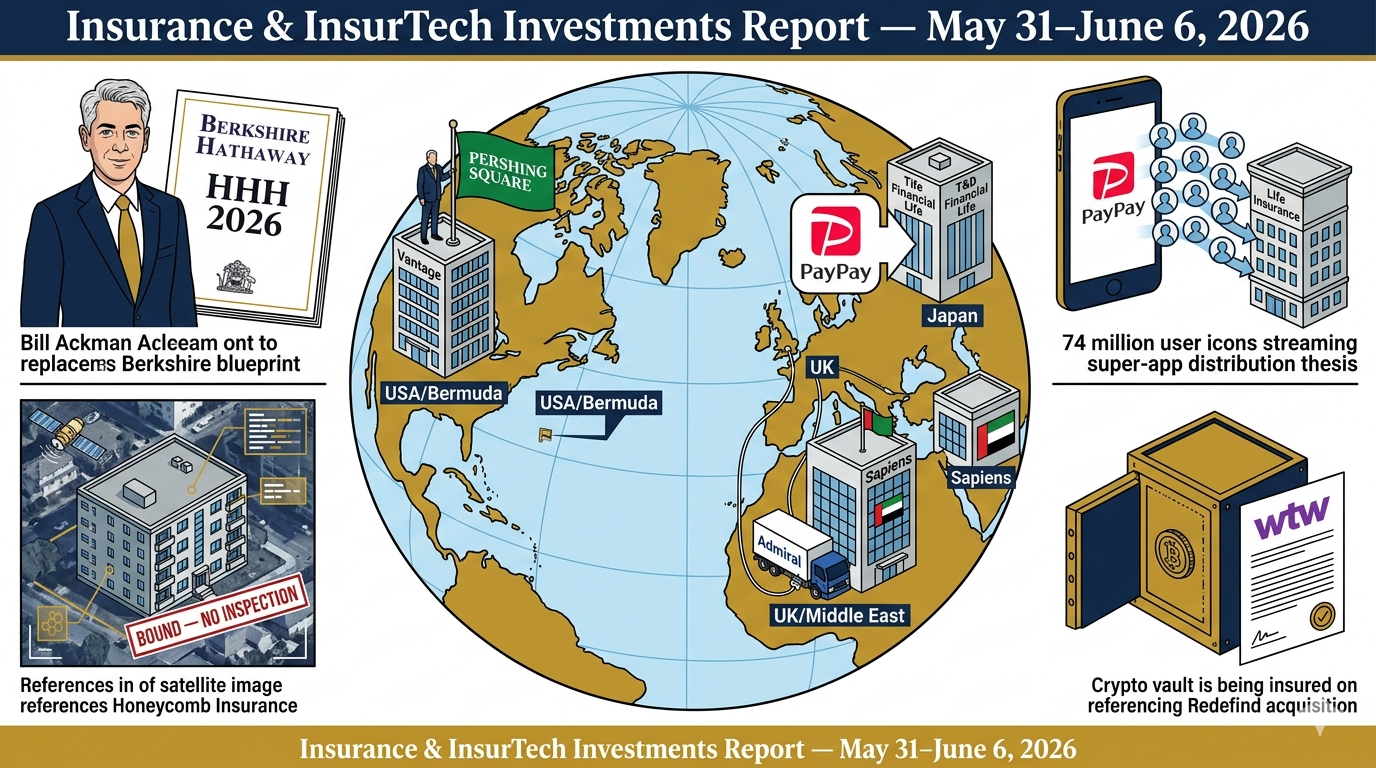

Six deals. $3.1B deployed. Bill Ackman built his Berkshire. PayPay bought a life insurer for 74 million users. Abu Dhabi backed insurance software. The world noticed insurance this week.

## Week of May 10–16, 2026

$1.75B+ disclosed | 7 transactions | Largest capital week of 2026

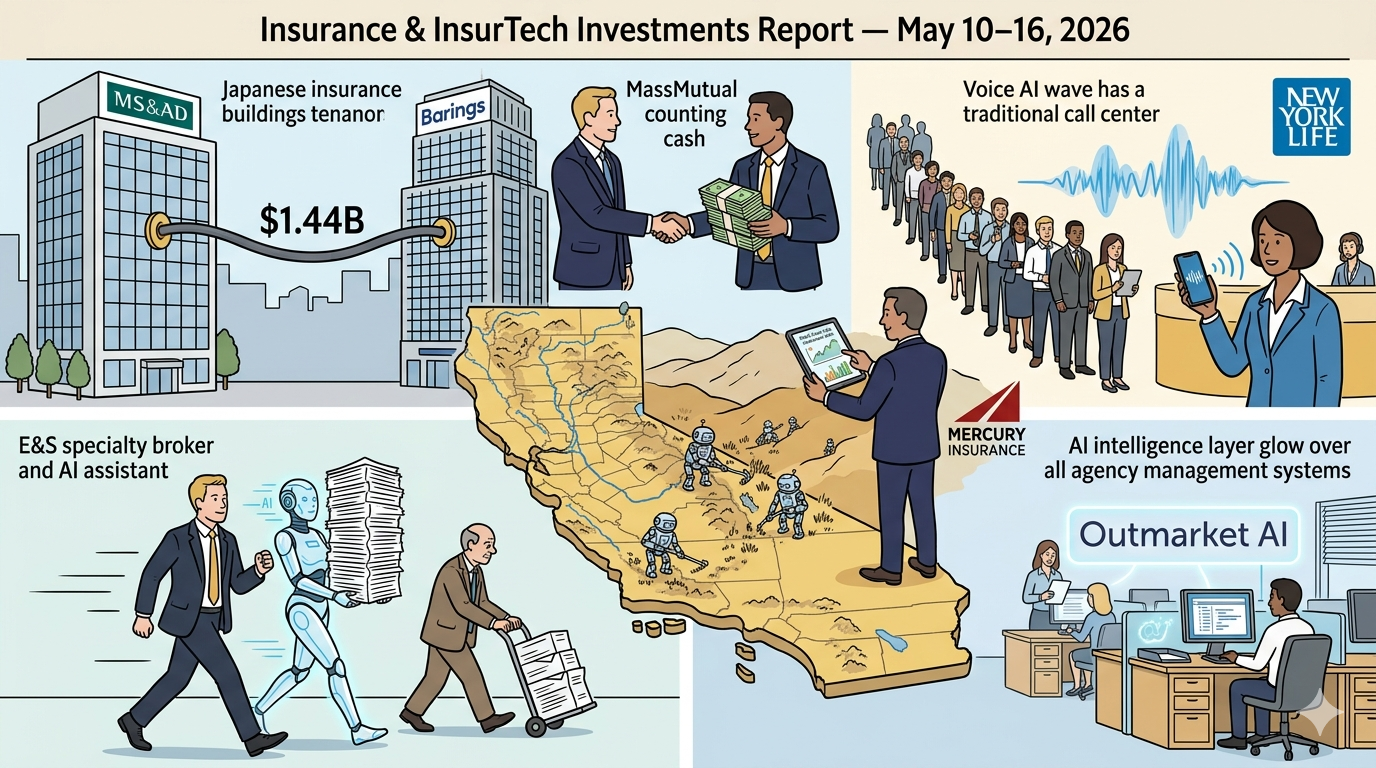

The week's headline number is $1.75 billion — but the composition is more important than the total. Three distinct capital themes converged simultaneously: AI is being embedded into the distribution layer of insurance (Novella, Outmarket AI, Vapi), carriers are moving upstream into physical risk reduction rather than just pricing for it (Mercury/BurnBot), and the global insurance-asset management convergence is producing its largest single transaction of the year (MS&AD/Barings). The brokerage consolidation machine continues in the background — Shepherd and ALPS both added scale quietly. This is not a week of isolated deals. It is a week where three structural shifts in insurance all moved at once.

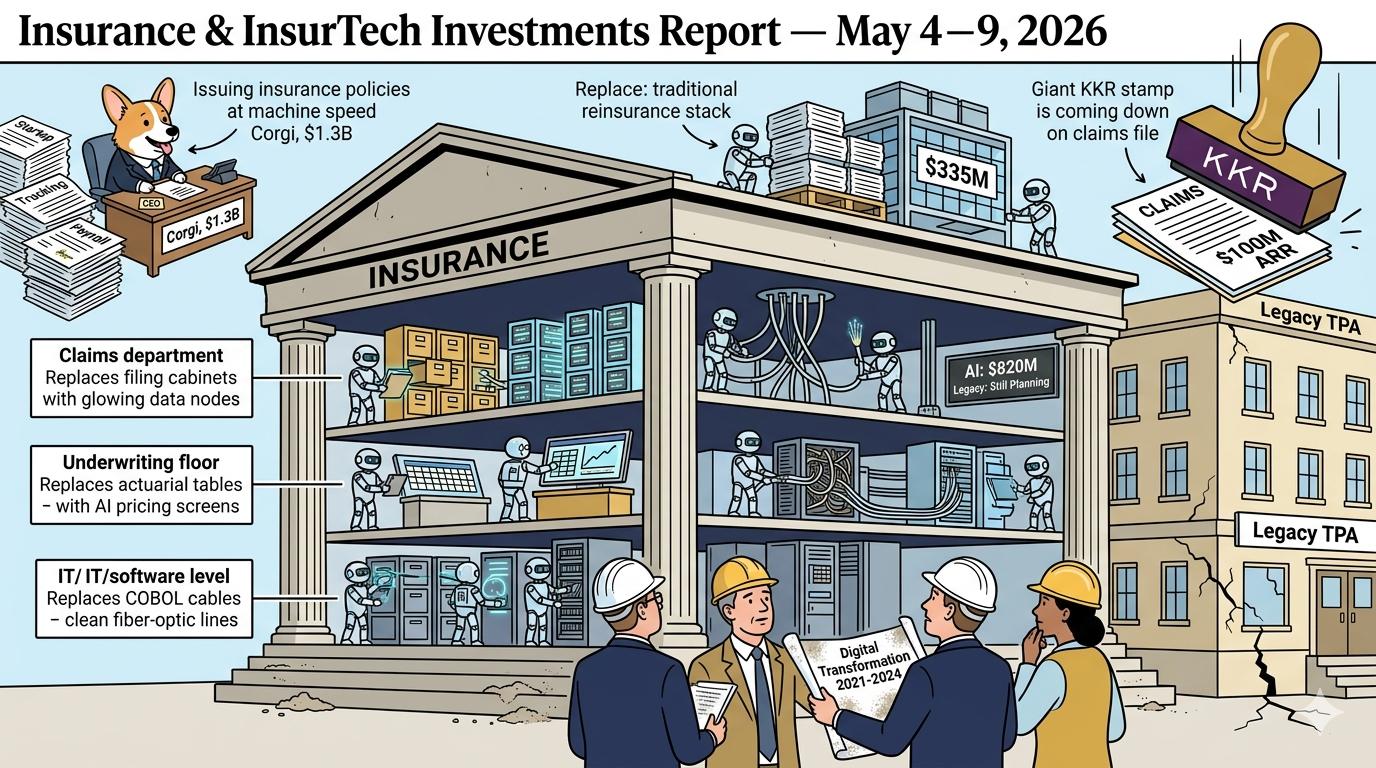

$820M disclosed | 4 transactions | Heaviest week of 2026 by capital deployed

Every deal this week is AI-native. Every deal attacks a different layer of the insurance infrastructure stack: claims administration, carrier underwriting, software modernization, and catastrophe capital. Gallagher Re's Q1 2026 report, released simultaneously, confirms the macro: global insurtech funding reached $1.63B in Q1, with AI-focused firms capturing 95% of all capital deployed. This week alone represents half of that quarterly total in five days. The insurance industry is not experimenting with AI. It is funding the companies that will make the current operating model obsolete.

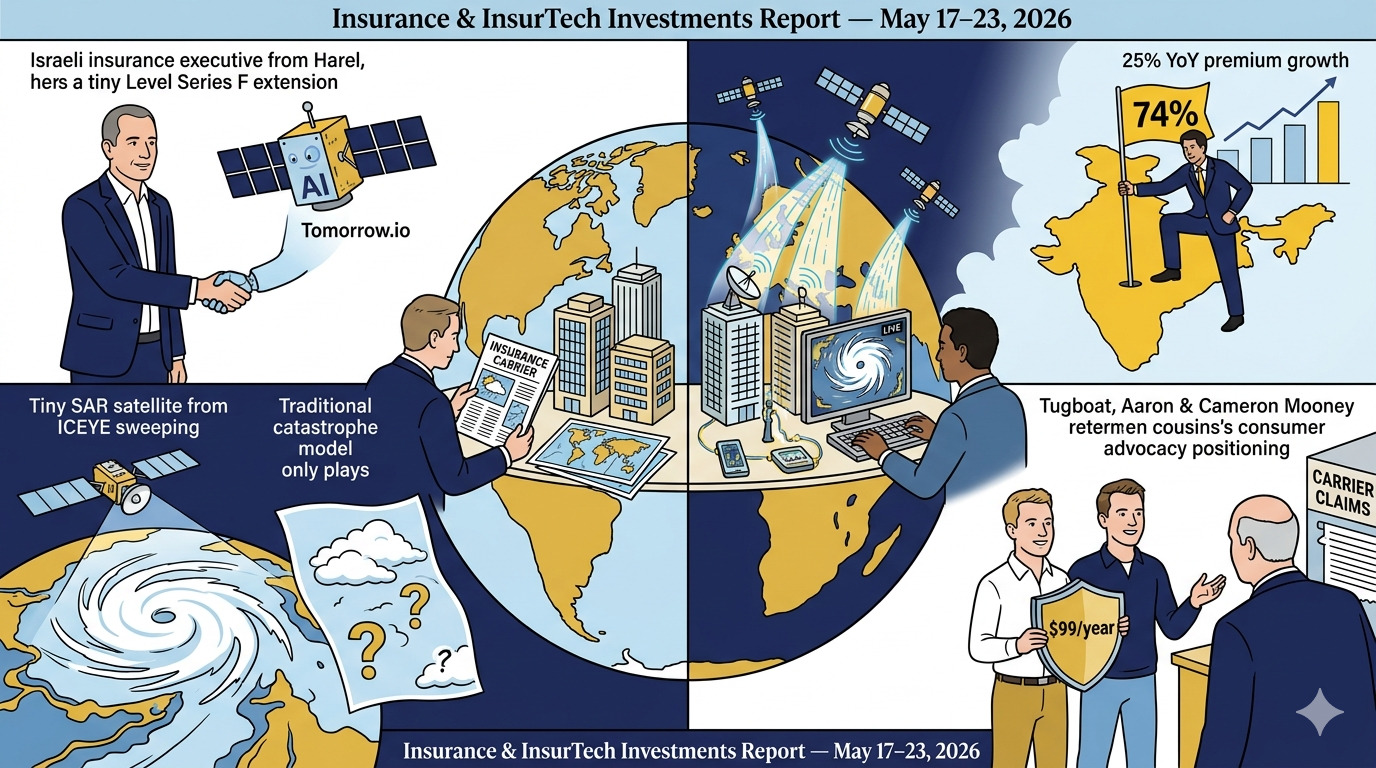

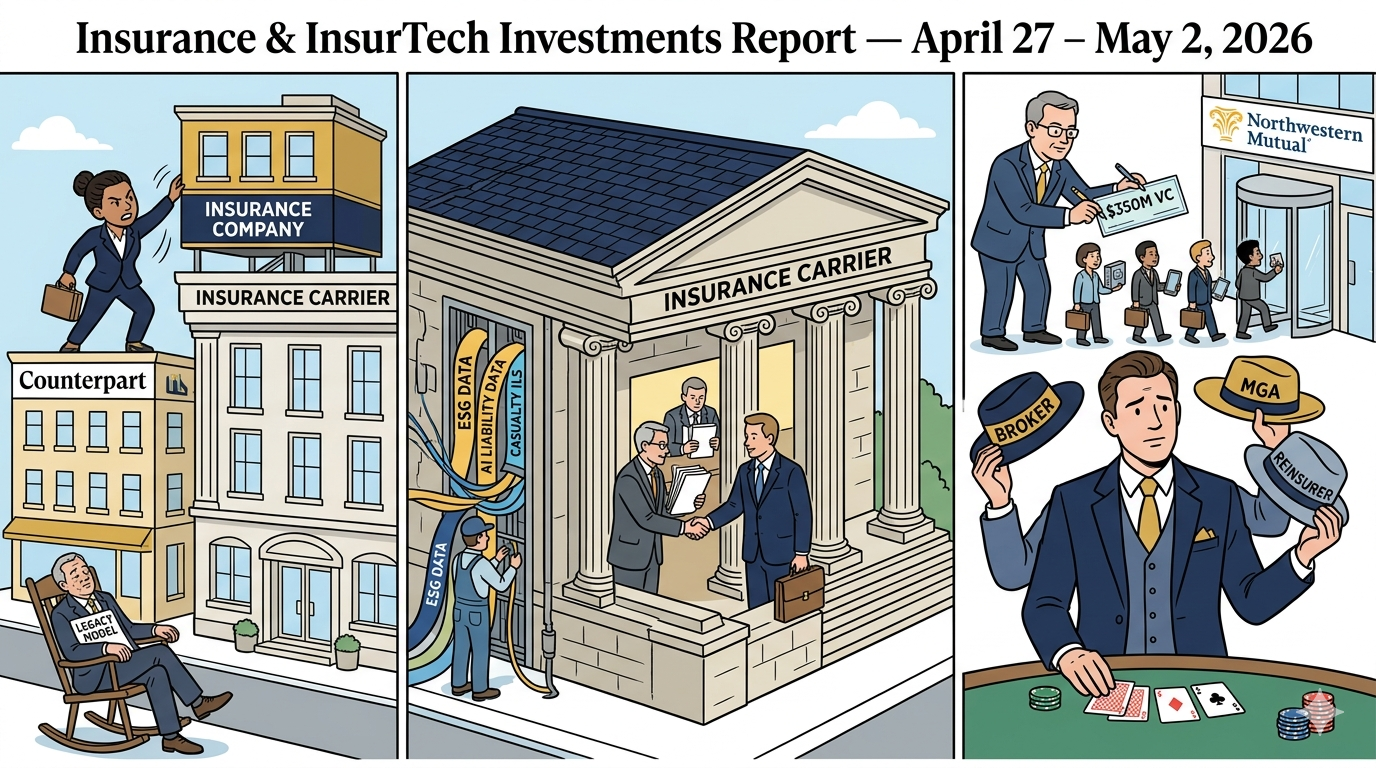

This wasn’t a big week. It was a decisive one.

Across six transactions, the signal is clear: insurance is consolidating around control—of data, distribution, capital, and underwriting.

From Counterpart taking risk onto its own balance sheet, to Northwestern Mutual turning venture into a distribution strategy, to Baldwin completing a fully integrated insurance stack—this is no longer about incremental innovation.

It’s about who owns the system

Capital this week flowed decisively toward AI-driven infrastructure and tightly integrated distribution models, with standout rounds in claims, TPA, and Medicare platforms. At the same time, both early-stage MGAs and scaled brokers attracted funding, reinforcing a market where owning workflow, data, and carrier alignment—not just distribution—defines competitive advantage.

$820M disclosed | 4 transactions | Heaviest week of 2026 by capital deployed

Every deal this week is AI-native. Every deal attacks a different layer of the insurance infrastructure stack: claims administration, carrier underwriting, software modernization, and catastrophe capital. Gallagher Re's Q1 2026 report, released simultaneously, confirms the macro: global insurtech funding reached $1.63B in Q1, with AI-focused firms capturing 95% of all capital deployed. This week alone represents half of that quarterly total in five days. The insurance industry is not experimenting with AI. It is funding the companies that will make the current operating model obsolete.

This wasn’t a big week. It was a decisive one.

Across six transactions, the signal is clear: insurance is consolidating around control—of data, distribution, capital, and underwriting.

From Counterpart taking risk onto its own balance sheet, to Northwestern Mutual turning venture into a distribution strategy, to Baldwin completing a fully integrated insurance stack—this is no longer about incremental innovation.

It’s about who owns the system