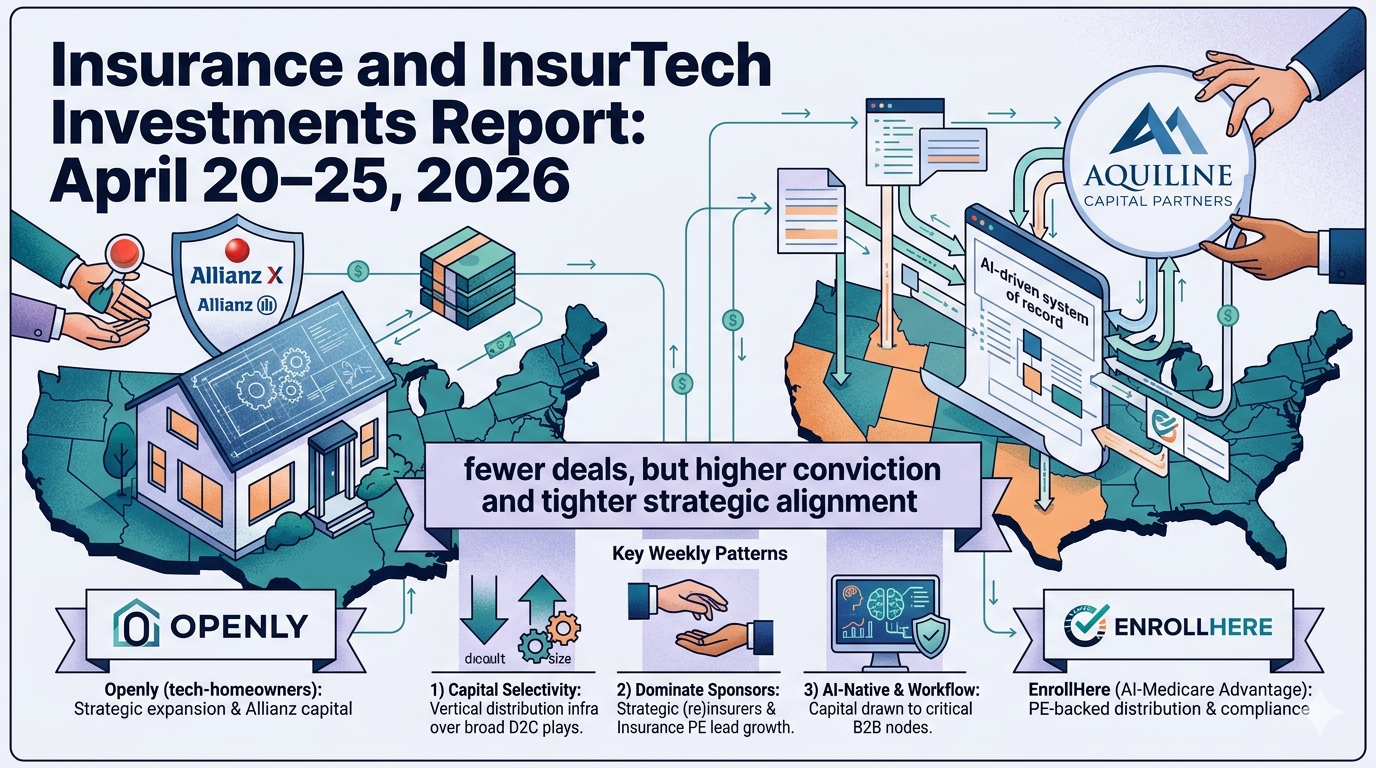

This week’s activity reinforces a sharp, ongoing reallocation of capital across insurance and insurtech: fewer deals, but higher conviction and tighter strategic alignment. Investors—especially carriers and specialist private equity—are concentrating capital behind platforms that control distribution, underwriting signal, or balance sheet access, rather than funding broad, undifferentiated D2C plays.

Openly – growth round + Allianz strategic expansion

1. Dates (announcement / execution)

- Press release time‑stamp: 22 April 2026

- Execution: Announced as a “closed” growth investment round; closing occurred shortly before the announcement (no separate signing/closing dates disclosed).

2. Investors and target

- Target: Openly, Boston‑based tech‑enabled homeowners insurer distributed via independent agents in the U.S.

- Investors in this round:

- Existing investors: Eden Global Partners, Advance Venture Partners, Gradient (lead).

- Strategic investor: Allianz X (strategic investment arm of Allianz).

- Capacity/partner: Allianz Re via an expanded long‑term reinsurance partnership announced alongside the equity round.

3. Amount of funds

- This week’s announcement describes a “growth investment round” but does not disclose the amount.

- A prior January 2025 growth financing totalled $193m (combining $123m equity led by Eden Global and a $70m senior note from Allianz X), which provides context but is a separate transaction.

4. Use of funds

- Scale Openly’s U.S. homeowners footprint and support rapid expansion into additional states.

- Invest in technology and data capabilities to improve underwriting, pricing accuracy and agent experience, leveraging Allianz Re’s expanded reinsurance support.

- Strengthen the balance sheet to manage catastrophe‑exposed property risk while keeping growth momentum.

5. Competition

- Direct insurtech / MGA peers in homeowners: Hippo, Kin, Branch, Slide and Lemonade’s home segment, plus regional MGAs writing cat‑exposed home risks. This group broadly targets digital or agent‑assisted home insurance in the U.S. P&C space.

- Incumbent multi‑line carriers still dominate homeowners but often lack Openly‑style cloud‑native underwriting platforms for independent agents.

6. Impact on competition

- The Allianz X equity plus expanded Allianz Re capacity gives Openly a capital + reinsurance bundle, enabling it to keep writing in cat‑exposed states where some insurtech peers have scaled back or rely on more expensive retro.

- Independent agents get more stable capacity and a modern quoting/underwriting platform, which can pull high‑value distribution away from smaller home MGAs and less tech‑enabled carriers, raising their acquisition costs and potentially compressing margins.

7. Why it’s a special case

- Strategic architecture: Allianz is simultaneously a major equity backer (via Allianz X) and long‑term reinsurer (via Allianz Re), effectively locking in both capital and risk‑sharing around Openly’s growth.

- Signal to market: It underlines the broader trend of (re)insurers stepping into roles once filled by VC/PE, using minority stakes plus reinsurance and distribution synergies as the core value proposition.

EnrollHere – Aquiline backs AI‑driven Medicare Advantage distribution

1. Dates (announcement / execution)

- Public announcement: 20 April 2026

2. Investors and target

- Target: EnrollHere Inc., AI‑powered platform and system of record for insurance distribution, focused on Medicare Advantage enrollment for agencies, field marketing organizations (FMOs) and carriers.

- Investor: Aquiline Capital Partners (specialist financial‑services and insurance‑focused private equity).

3. Amount of funds

- Amount not disclosed in the press material or secondary coverage; described simply as an investment from Aquiline.

4. Use of funds

- Advance EnrollHere’s technology for Medicare Advantage distribution, including improving enrollment quality, strengthening compliance, and increasing lifetime value.

- Scale the platform as a system of record for agencies and FMOs, expanding customer base and enhancing AI‑driven workflow and compliance controls.

5. Competition

- Competes with other Medicare Advantage distribution platforms and lead‑management/CRM systems used by agencies and FMOs, as well as internal tools developed by large carriers.

- Also overlaps with broader health‑insurtech platforms that focus on senior distribution, enrollment quality and CMS compliance tooling.

6. Impact on competition

- A specialized AI system of record with fresh PE backing can set a higher bar on compliance, traceability and enrollment quality, putting pressure on legacy CRM/lead tools that are not purpose‑built for Medicare Advantage.

- For MA carriers, tighter integration with EnrollHere may reduce mis‑selling and post‑sale remediation costs, indirectly advantaging carriers that adopt the platform over those that continue with fragmented or manual distributor tooling.

7. Why it’s notable

- Illustrates PE’s continued interest in vertical distribution infrastructure rather than full‑stack insurance risk, aligning with the broader shift of insurtech capital toward workflow, compliance and AI‑driven B2B.

- The focus on MA compliance and lifetime value taps into regulatory pressure and audit scrutiny in U.S. senior‑health distribution – areas that are budget‑protected even in tighter funding markets.

Not pure capital raises, but strategically relevant

Orbway – becomes licensed agent with Ensuro capacity

- Orbway became a licensed insurance agent; Ensuro is the initial capacity partner.

- While no funding is disclosed, this is effectively a distribution / capacity alignment: Orbway gains regulatory permission to act as an intermediary, while Ensuro (a capital provider with programmable or alternative‑capital DNA) gets a new fronting/distribution partner.

- Competitive effect: adds another option in the alternative‑capacity / on‑chain or tech‑enabled capacity space; competes with other fronting carriers and capacity providers that partner with digital MGAs and agents.

Anthemis portfolio outcomes – exits vs wind‑downs

- This is not a single financing but rather a portfolio‑level re‑rating: the mixed outcomes underscore that even a specialist insurtech VC is managing through an environment with both successful exits and failures, reinforcing the current capital‑selective mood.

These items support your narrative about where capital is flowing (and being pulled back) even when a discrete raise is not reported.

Honeycomb Insurance hiring push – signal, not a transaction

- Honeycomb Insurance accelerating U.S. hiring to support insurtech expansion; this is clearly read by equity investors as a signal of continued growth and capital availability, but no fresh funding round is disclosed.

- In context of March/April data showing global insurtech funding at its lowest monthly level of 2026 so far, a hiring ramp‑up suggests Honeycomb either has sufficient prior capital or expects near‑term growth in premium and fee income to fund expansion.

Weekly pattern and competitive takeaways

Over April 20-25 window, the most concrete capital events in insurance/insurtech are:

- Openly – strategic growth round (amount undisclosed) led by existing investors, with Allianz X and Allianz Re deepening their equity + reinsurance partnership.

- EnrollHere – undisclosed‑size growth investment from Aquiline to scale an AI system‑of‑record for Medicare Advantage distribution.

Capital is highly selective and thesis‑driven

- Global insurtech funding in March 2026 dropped to the lowest monthly level so far this year (about $237m across 10 deals), confirming that investors are writing fewer, more targeted checks.

- Against that backdrop, both Openly and EnrollHere fit a narrow thesis: capital goes to platforms that control critical infrastructure nodes (independent‑agent home distribution, Medicare Advantage enrollment and compliance) rather than broad, undifferentiated D2C brands.

Strategics and specialist PE are now the dominant sponsors

- Gallagher Re’s latest Global InsurTech Report shows (re)insurers made more insurtech investments in 2025 than in any prior year, overtaking traditional VC and PE as the largest investor group.

- This week continues that pattern: Allianz X / Allianz Re around Openly and Aquiline around EnrollHere exemplify strategic (re)insurers and insurance‑focused PE leading the important later‑stage and growth deals, with generic multi‑sector VC largely absent.

AI‑native and workflow infrastructure remain the core magnet for capital

- Beinsure’s 2026 funding analysis shows roughly two‑thirds of 2025 insurtech capital went to AI‑focused firms, and ~78% of Q4‑2025 funding involved companies with a material AI component.

- EnrollHere is explicitly positioned as an AI‑powered system of record for Medicare Advantage distribution, while Openly’s value proposition emphasizes data‑driven underwriting and agent‑facing technology, aligning both deals squarely with investors’ preference for AI‑powered B2B infrastructure rather than pure risk‑taking.

Competitive implications: pressure on undifferentiated carriers and “thin” insurtechs

- In U.S. homeowners, Allianz’s equity plus reinsurance package gives Openly a structurally cheaper and more stable capital stack in catastrophe‑exposed states than smaller MGAs and some venture‑backed full‑stack insurtechs, which may rely on more expensive retro or have already pulled back capacity.

- In Medicare Advantage, a PE‑backed, AI‑native system of record like EnrollHere raises the bar on enrollment quality and compliance; agencies and carriers that remain on generic CRMs and fragmented workflows will likely face higher mis‑selling risk and remediation expense, weakening their competitive position over time.

Labor and portfolio signals support the same narrative

- Honeycomb’s current U.S. hiring push (without a new raise attached) is a secondary signal that investors are comfortable funding disciplined, property‑focused insurtechs that have already proven their unit economics, even as overall monthly funding volumes remain subdued.

- At the same time, portfolio‑level updates like Anthemis’ mix of exits and wind‑downs underscore that even specialist VCs are actively pruning, reinforcing that capital will concentrate in a small set of AI‑native infrastructure and specialty plays rather than the broader 2020–2021 insurtech cohort.