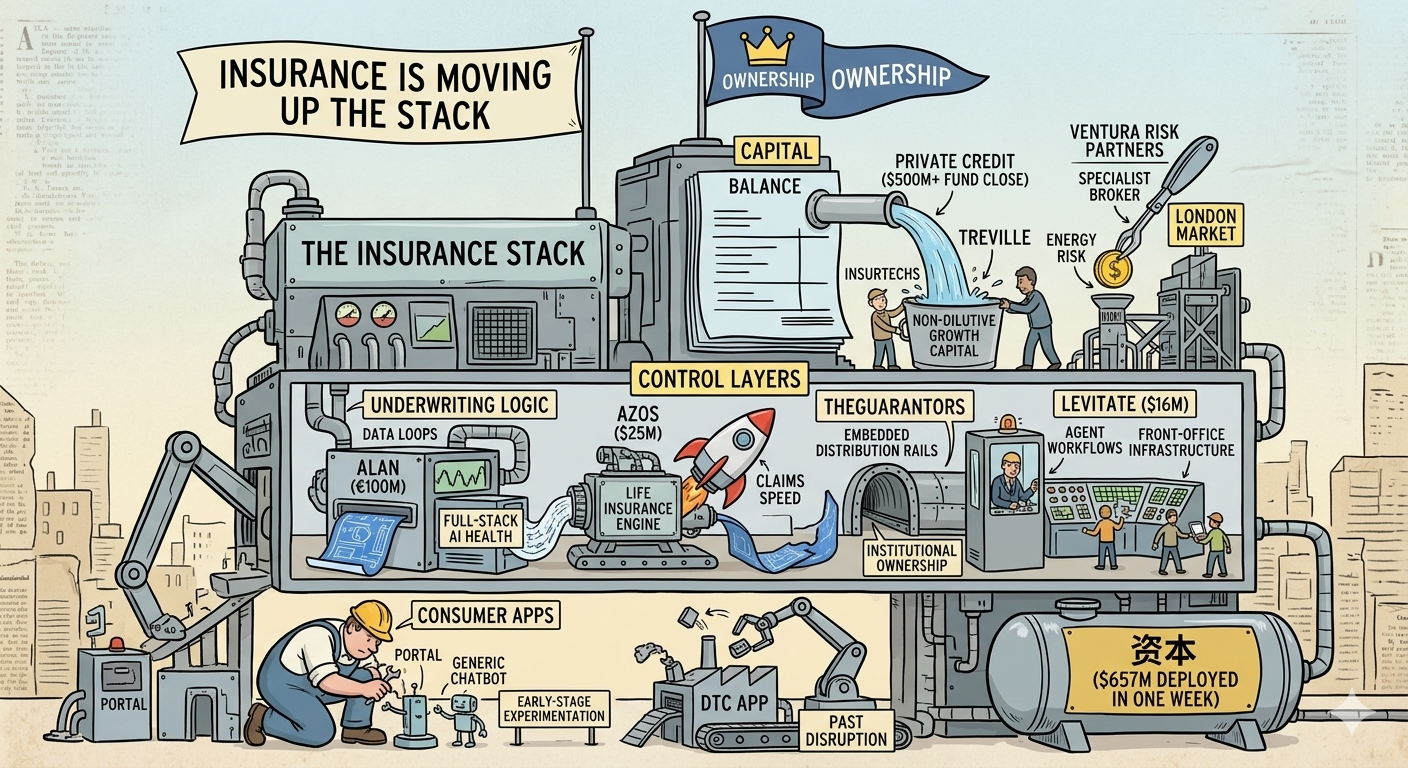

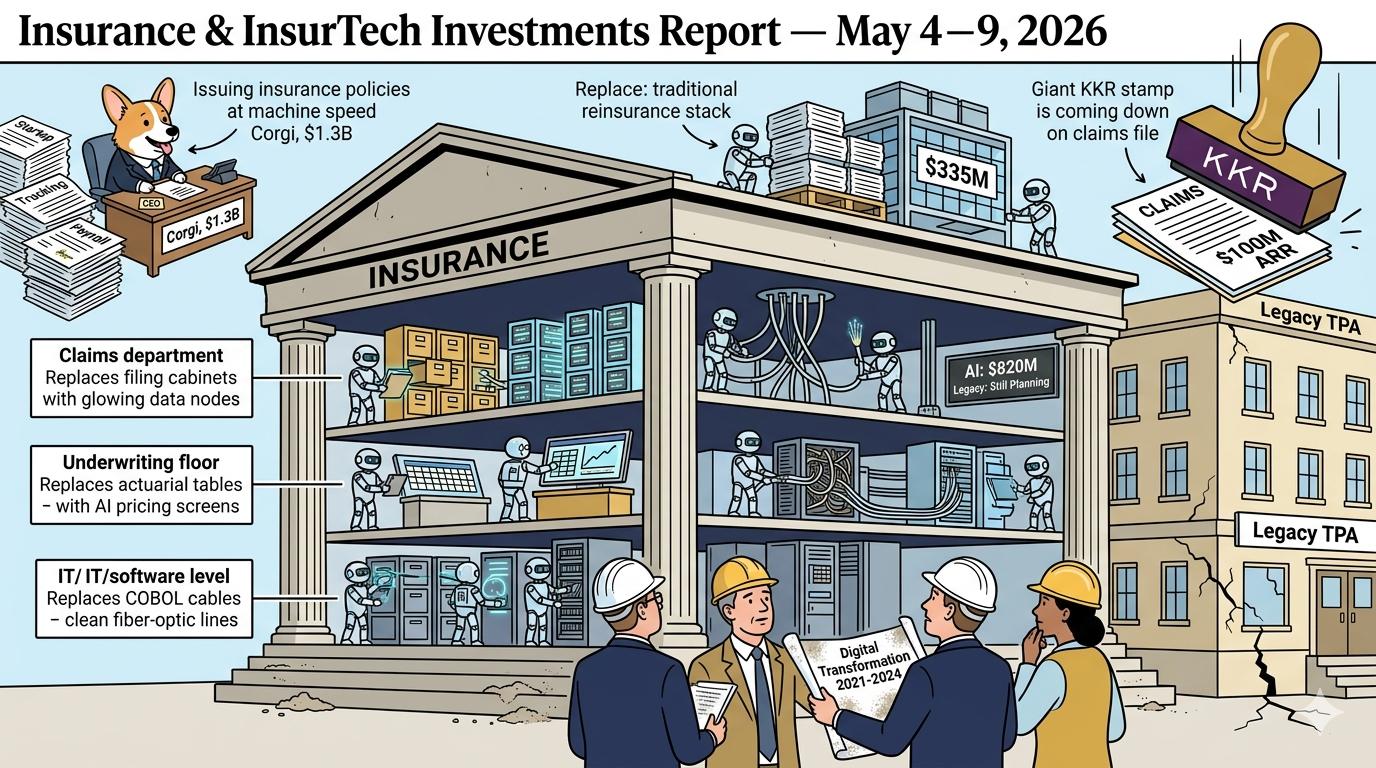

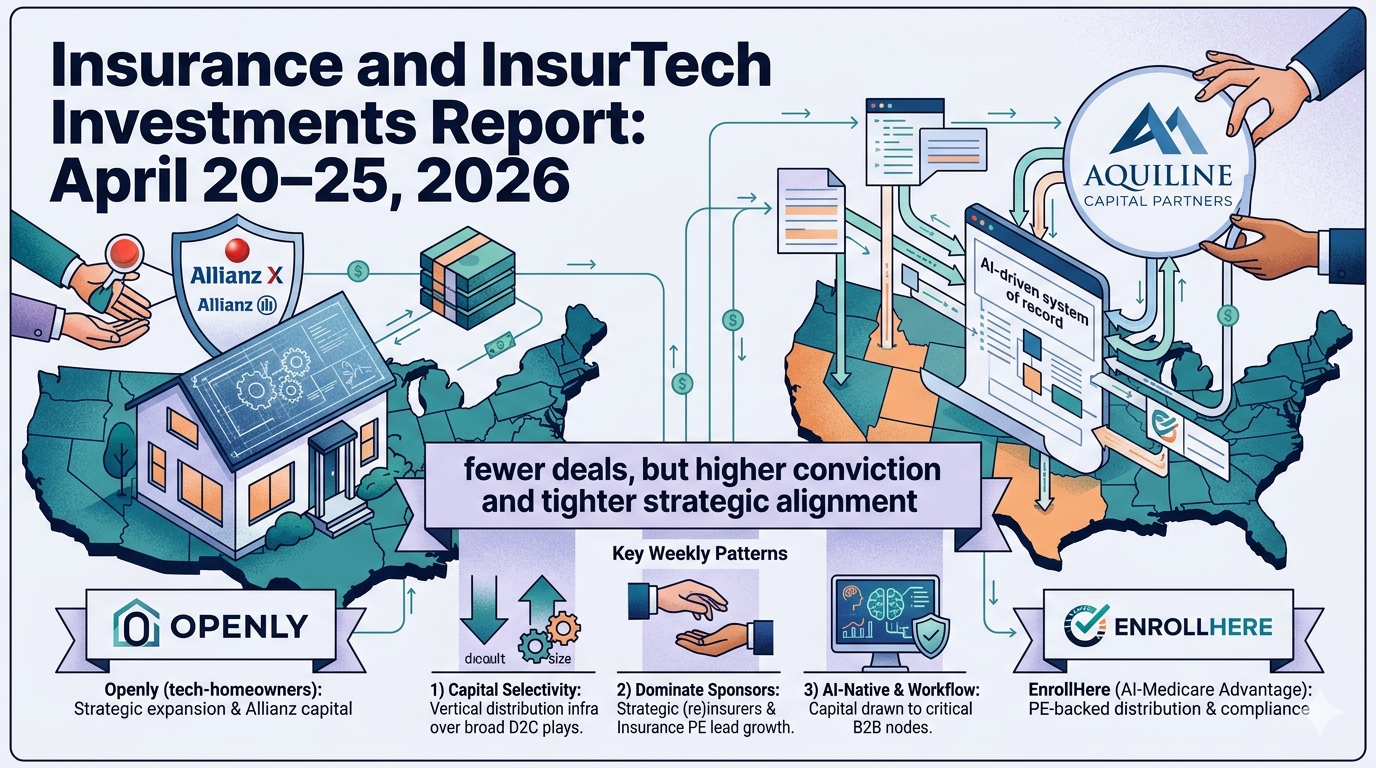

This week’s activity reinforces a sharp, ongoing reallocation of capital across insurance and insurtech: fewer deals, but higher conviction and tighter strategic alignment. Investors—especially carriers and specialist private equity—are concentrating capital behind platforms that control distribution, underwriting signal, or balance sheet access, rather than funding broad, undifferentiated D2C plays.