$129.5M+ in disclosed capital | 4 primary transactions + 2 special situations + 1 market context | AI governance hits unicorn status, Firemark completes its resilience stack, and brokerage consolidation runs at structural velocity

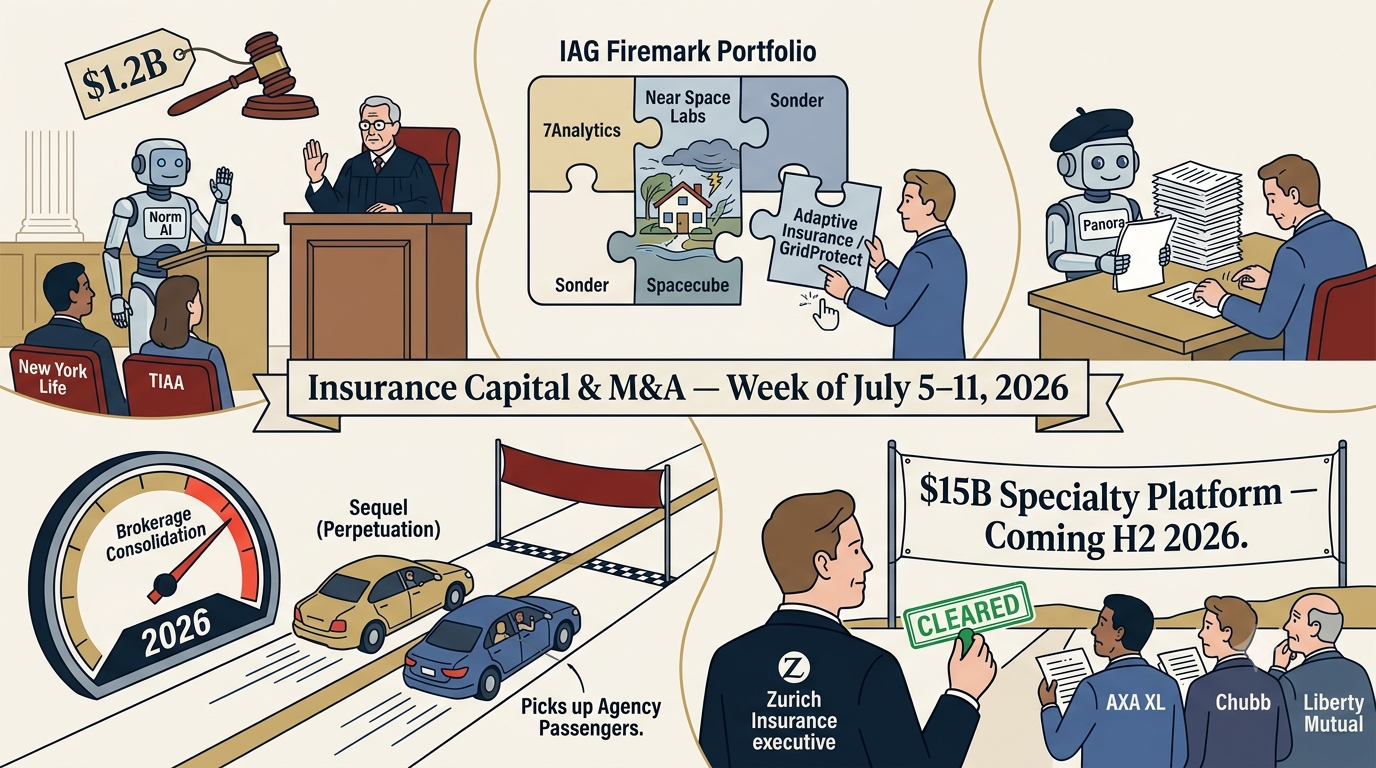

Three primary deals, a regulatory milestone, a French AI broker seed round, and a brokerage consolidation context note define a week where strategic depth outweighs capital volume at every layer of the insurance stack. Norm AI crossed a $1.2 billion valuation with New York Life and TIAA as named strategic investors. IAG Firemark Ventures made its fifth consecutive weekly investment in Adaptive Insurance, completing its deliberate disaster resilience architecture. Mile Auto acquired Insurance House, combining AI-native pay-per-mile pricing with 62 years of Southeast agency distribution into a $100M premium platform. Zurich's £8.1B Beazley acquisition cleared the European Commission. Panora raised a $4.5M seed to automate European broker workflows. And Sequel and ALKEME both closed brokerage consolidation deals in the same week, from opposite ends of the succession model spectrum.

1. Norm AI (USA)

$120M Series C at $1.2B Valuation | Agentic Legal and Regulatory Compliance — New York Life and TIAA as Strategic Investors Date: July 7, 2026

What Happened

Founded in 2023 by Piper Merriam (CEO), New York-based Norm AI raised a $120 million Series C at a $1.2 billion valuation, crossing the unicorn threshold in under three years. The round was led by Khosla Ventures (Samir Kaul, Managing Director), the first institutional investor in OpenAI. Additional participants include Blackstone, Bain Capital Ventures, Craft Ventures, Coatue, Vanguard, New York Life (via New York Life Ventures), TIAA, Tony James (former President and COO of Blackstone), Jeff Hammes (former Chairman of Kirkland & Ellis), and Fenwick LLP. Total funding since founding: $260M+. Norm AI builds what it calls "agentic law" — embedding legal and regulatory reasoning into AI agents that can execute compliance workflows, govern other AI systems, and deliver legal services to institutional clients. Its affiliated AI-native law firm, Norm Law LLP, employs senior attorneys who supervise AI agents rather than managing associate pyramids, pricing services on outcomes rather than billable hours. Client base: organizations representing more than $30 trillion in combined assets under management, spanning global banks, hedge funds, insurance companies, and asset managers. New York Life uses Norm AI to automate regulatory compliance reviews. The Series C proceeds fund continued hiring of senior attorneys and AI engineers, expansion of legal practice area coverage, and development of supervisory AI agents for regulated enterprise deployments.

- Lead: Khosla Ventures (Samir Kaul, Managing Director)

- Strategic insurance investors: New York Life (via New York Life Ventures), TIAA

- Financial investors: Blackstone, Bain Capital Ventures, Craft Ventures, Coatue, Vanguard

- Individual investors: Tony James (former Blackstone President/COO), Jeff Hammes (former Kirkland & Ellis Chairman)

- Institutional investor: Fenwick LLP (law firm as investor)

Use of Funds

- Hire senior attorneys and AI engineers at scale

- Expand Norm Law LLP's practice area coverage across regulated industries

- Build supervisory AI agents that govern other AI systems in regulated environments

- Accelerate Microsoft 365 Copilot compliance agent deployment

Strategic Thesis

Two insurance carriers — New York Life and TIAA — made a deliberate decision to invest in the company that automates the regulatory compliance reviews they are most exposed to. That is not a passive financial investment. It is a procurement decision dressed as a venture investment. New York Life Ventures already uses Norm AI in production for regulatory compliance reviews. The investment extends that relationship into equity participation, giving New York Life access to Norm AI's product roadmap and supervisory AI agent development before competitors with purely financial relationships.

The supervisory agent thesis is the most consequential element of the Norm AI platform for insurance. As carriers deploy AI in underwriting, claims, fraud detection, and customer service, the regulatory question that follows immediately is: who governs the AI? Who ensures the AI's decisions comply with applicable regulations? Who maintains the audit trail that regulators will eventually require? Norm AI's supervisory agents answer that question by sitting above AI deployments and verifying outputs against codified regulatory rules. For carriers deploying AI at scale, Norm AI is not optional infrastructure. It is the compliance layer that makes AI deployment defensible.

Blackstone's dual role — as investor and as the most prominent disclosed client — provides the institutional credibility that financial services clients require before trusting a two-year-old company with regulatory compliance at institutional scale. The precedent Blackstone sets for other alternatives managers and insurance companies evaluating Norm AI is worth more than its financial commitment.

Why It Matters

- New York Life and TIAA investing as strategic participants confirms that insurance carriers view AI-native regulatory compliance infrastructure as a procurement priority, not an exploratory technology bet

- The supervisory agent layer Norm AI is building — AI that governs AI in regulated environments — is the missing infrastructure that has slowed enterprise AI deployment across insurance and financial services, where "what happens if the AI is wrong" is a threshold question before any deployment can proceed

- Blackstone's simultaneous role as investor and the platform's most prominent named client creates a reference sale dynamic that compresses the procurement evaluation cycle for other institutional clients evaluating Norm AI

Competition

- Direct competitors (AI legal and compliance): Harvey (legal AI, $11B valuation, $200M Series G March 2026), Legora (legal research AI), Casetext (acquired by Thomson Reuters)

- Category competitors: Big Four consulting AI governance practices, traditional legal tech (Relativity, Kira Systems), in-house legal team expansion

- Insurance-specific competitive dynamic: dodoAI (Japan, Week 26), Trussed AI (Week 25), and Norm AI represent three distinct national implementations of AI governance infrastructure emerging simultaneously — each backed by insurance carriers as strategic investors

Market Consequences

The pattern across four consecutive weeks is now impossible to ignore: insurance carriers are investing in AI governance infrastructure globally. Nassau Financial backed Trussed AI (US, Week 25). Mitsui Sumitomo Insurance Venture Capital backed dodoAI (Japan, Week 26). New York Life and TIAA backed Norm AI (US, Week 28). Three different platforms. Three different architectures. Three different geographies. One consistent conclusion: the carriers deploying AI at scale recognize that governance infrastructure is not optional — it is the compliance prerequisite that regulators will eventually require and that procurement decisions already demand.

For insurers still deploying AI without a governance layer, the New York Life and TIAA investments are a market signal: two of the largest and most risk-conscious life insurance companies in the United States have concluded that AI governance infrastructure is a strategic priority, not a future consideration. The regulatory timeline is compressing.

Norm AI just hit $1.2 billion. New York Life uses it in production. TIAA invested alongside. An AI system that governs other AI systems in regulated environments is no longer a research project. It is a $1.2 billion enterprise with two insurance carriers inside the cap table.

2. Adaptive Insurance (USA)

$5M | Climate Specialty MGA — IAG Firemark's Fifth Consecutive Weekly Investment Date: July 7, 2026

What Happened

Founded in 2024 by Mike Gulla (CEO and Co-Founder) and Arik Yelovitch (CTO and Co-Founder), Austin, Texas-based Adaptive Insurance is a specialty MGA and insurtech platform building AI-driven insurance and technology solutions for climate and weather risks that traditional insurance has either restricted, exited, or never addressed. The company closed an additional $5 million in financing from new and existing investors, bringing total funding to $10 million. New investors include IAG Firemark Ventures (Alex Guyer), Sunna Ventures, Room & Pillar, and Connecticut Innovations. Existing investors Congruent Ventures and Seraphim Space participated alongside private stakeholders. Adaptive's current product suite: GridProtect (first parametric insurance for short-duration power outages, triggering predefined payouts based on verified outages using real-time third-party data), Wind and Hail Deductible Buy-Back (residential and commercial), residential flood insurance (broader coverage and higher limits than NFIP), and Commercial Equipment Breakdown. Adaptive also powers Tokio Marine HCC's Restaurant Recovery program through its proprietary technology platform. The round will support expansion of the specialty product portfolio, growth of agent and partner distribution, and continued development of Adaptive's proprietary climate intelligence platform.

- New investors: IAG Firemark Ventures, Sunna Ventures, Room & Pillar, Connecticut Innovations

- Existing investors: Congruent Ventures, Seraphim Space

Use of Funds

- Expand specialty product portfolio into additional climate and infrastructure risk categories

- Grow agent and partner distribution network nationally

- Continue development of proprietary climate intelligence platform

Strategic Thesis

IAG Firemark Ventures has now made five consecutive investment announcements in five weeks: Sonder (mental health, Week 25), Spacecube (physical recovery, Week 26), and now Adaptive Insurance (climate specialty products, Week 28). Add 7Analytics (flood prediction) and Near Space Labs (aerial imagery) from earlier in 2026 and the Firemark portfolio spans the complete disaster risk lifecycle: predict, detect, support, recover, and now product. Adaptive fills the product layer — the actual insurance coverage for the risks that Firemark's data and recovery platforms identify and address.

Alex Guyer at IAG Firemark Ventures stated the investment rationale directly: "Consumers and businesses increasingly need insurance solutions that can adapt to risks that are evolving faster than traditional products were designed to address." That sentence is a precise description of the three structural problems Adaptive is solving. Traditional policies don't cover short-duration power outages (GridProtect addresses this). NFIP flood coverage is inadequate for most residential flood risk (Adaptive's flood product addresses this). Wind and hail deductibles have escalated to levels that make them unaffordable to bear (the buy-back product addresses this). Each product targets a gap created by the collision between accelerating climate risk and the slow pace of traditional insurance product development.

The Seraphim Space participation is the most forward-looking signal in the investor list. Seraphim Space is a specialist venture fund focused on space technology applications — the same satellite observation infrastructure that ICEYE deploys and that Firemark's Near Space Labs investment provides. Parametric insurance powered by satellite-verified event data is the most natural convergence of the space and insurance capital flows that have been building throughout 2026. Adaptive's GridProtect product already uses real-time third-party data for outage verification. The infrastructure to verify flood, wind, and hail events from satellite and aerial data is becoming commercially available. Adaptive is positioned at that convergence point.

Why It Matters

- IAG Firemark Ventures' fifth consecutive investment completing its disaster resilience portfolio confirms that the Firemark strategy is deliberate, systematic, and fully articulated: the Adaptive investment fills the product coverage layer that was the only gap remaining in the prediction/detection/support/recovery stack

- GridProtect is the first parametric insurance product specifically for short-duration power outages — a risk that is simultaneously growing (grid stress, extreme heat, storm frequency) and currently uninsured by any traditional product in the market

- The FEMA context Adaptive cites is structurally important: FEMA cancelled $600M in Flood Mitigation Assistance grants across 36 states in 2025, increasing the burden on private insurance to fill the gap that government programs are vacating

Competition

- Direct competitors (climate specialty MGA): Kin Insurance (cat-exposed homeowners), Neptune Flood (NFIP alternative flood), Swell Energy (parametric home energy), Jumpstart Insurance (earthquake parametric)

- Category competitors: Traditional specialty carriers with climate product lines, NFIP for flood, FAIR plans for property of last resort

- Emerging dynamic: The parametric insurance category is expanding rapidly as verified event data from satellites and IoT sensors enables products that pay automatically based on observable triggers rather than assessed damage — a structurally superior claims experience for both insurers and policyholders

Market Consequences

FEMA's $600M in cancelled flood mitigation grants, Swiss Re's $181B global protection gap figure for 2024, and the accelerating withdrawal of admitted carriers from climate-exposed markets collectively describe a structural supply shortage in climate risk coverage that is growing faster than any individual carrier can address. Adaptive's approach — build parametric products for specific risk categories using verified third-party data triggers — is the most capital-efficient response to that shortage. Each parametric product Adaptive launches eliminates the claims assessment cost that makes traditional insurance uneconomical for the same risk category. GridProtect pays automatically on verified outage data. The flood product uses verified precipitation and inundation data. The administrative cost structure is fundamentally lower, enabling Adaptive to price competitively in categories where traditional carriers cannot.

IAG Firemark Ventures just made its fifth investment in five weeks. The portfolio now spans prediction, detection, psychological support, physical recovery, and climate product. Adaptive fills the final layer. The architecture is complete.

3. Mile Auto / Insurance House (USA)

Undisclosed | AI-Native Pay-Per-Mile MGA Acquires 62-Year-Old Southeast Agency — $100M Combined Premium Date: Effective July 1, 2026 / Announced July 10, 2026

What Happened

Mile Auto, Inc. — an Atlanta-based AI-driven managing general agent founded in 2017 by Fred Blumer (CEO), Jim Cook, Joe Fuller, and Scott Nelson — announced its acquisition of The Insurance House, Inc., a Georgia-based MGA with 62 years of operating history (founded 1964), effective July 1, 2026. The combined organization represents nearly $100 million in annual premium and serves 55,000+ policyholders through 1,600 independent insurance agencies across 10 states. Mile Auto contributed patented AI and computer vision technologies enabling privacy-focused, mileage-based insurance pricing without telematics devices, smartphone GPS tracking, or additional hardware — customers photograph their odometer monthly, and Mile Auto's computer vision validates the mileage. Insurance House contributes six decades of MGA expertise, established carrier relationships with Southern General Insurance Company (fronting carrier, relationship continues), and a Southeast independent agency distribution network. Both brands will continue operating independently. Mile Auto's partnership with Cimarron Insurance Company also continues for its existing product portfolio. Financial terms not disclosed.

- Acquirer: Mile Auto (AI-native pay-per-mile MGA)

- Target: Insurance House (62-year-old Southeast MGA, fronted by Southern General)

- Mile Auto investors: Ulu Ventures, Emergent Ventures, Thornton Capital, Sure Ventures

- Exclusive distribution: Porsche Auto Insurance (Mile Auto is exclusive provider)

Use of Funds

- Expand geographic reach and product availability under combined platform

- Deploy Mile Auto technology across Insurance House's 1,600-agency distribution network

- Accelerate product innovation using combined premium volume and data scale

Strategic Thesis

Mile Auto's acquisition of Insurance House is the clearest example this week of the technology-distribution combination thesis that is reshaping the MGA category. Mile Auto has the technology: patented computer vision for odometer validation, AI-driven mileage-based pricing that saves low-mileage drivers up to 40% on premiums, and a product design that is privacy-compliant without requiring any hardware or app installation. What it has not had at scale: the independent agency distribution network that moves auto insurance volume in the Southeast. Insurance House has exactly that: 62 years of agency relationships, 1,600 independent agencies, and a trusted carrier partnership with Southern General that provides the fronting capacity Mile Auto's product needs in that distribution channel.

The $100M combined premium threshold matters. Under $100M in combined premium, MGAs are generally viewed as pre-institutional — they are interesting but not yet investable at growth equity scale. At or above $100M, the asset quality profile changes: carrier capacity is easier to negotiate, reinsurance access improves, and the business becomes a recognizable institutional asset. Mile Auto's acquisition of Insurance House is not just a distribution deal. It is a deliberate crossing of the institutional scale threshold that positions the combined entity for the next capital event at a meaningfully different valuation anchor.

Fred Blumer's framing is precise: "Mile Auto contributes industry-leading technology and broad distribution, while Insurance House brings decades of market experience and trusted agency relationships. Together, we're creating a stronger organization." That sentence describes the MGA combination thesis in one formulation: neither technology alone nor distribution alone creates institutional value at the scale the combined entity achieves.

Why It Matters

- $100M in combined annual premium is the threshold at which MGA platforms become institutionally investable as growth equity assets — Mile Auto crossed it through acquisition rather than organic growth, which is faster and more capital-efficient when the target brings verified distribution relationships

- Mile Auto's computer vision odometer technology is device-free and privacy-preserving, which addresses the primary objections that consumers have raised against usage-based insurance programs requiring telematics hardware or continuous GPS monitoring

- The Porsche Auto Insurance exclusive distribution relationship gives Mile Auto a premium brand anchor that most independent MGAs cannot access, providing a second distribution channel alongside the independent agency network

Competition

- Direct competitors (usage-based and pay-per-mile auto insurance): Metromile (acquired by Lemonade), Root Insurance, Clearcover, Kin, By Miles (UK)

- Category competitors: Traditional auto insurance carriers with UBI programs (State Farm Drive Safe & Save, Nationwide SmartRide, Progressive Snapshot)

- Emerging dynamic: AI-native pricing combined with traditional agency distribution is becoming the competitive template for MGA market entry at scale — Carbon Underwriting (Lloyd's, last week), Corgi (commercial lines, May), and Mile Auto/Insurance House all represent variants of the same combination thesis

Market Consequences

Independent agency distribution networks — the 1,600 agencies that Insurance House has cultivated over 62 years — are being absorbed into technology-native MGA platforms at an accelerating pace. For traditional regional MGAs without equivalent technology infrastructure, the combination thesis creates a competitive challenge: agencies increasingly prefer MGA partners that offer better pricing tools, faster quote generation, and more competitive products alongside established carrier relationships. Mile Auto's computer vision pricing technology can deliver all three. The Southeast auto insurance market, where Insurance House has operated for six decades, now has a combined platform that can price risk more precisely than traditional competitors, distribute through established agency relationships, and cross-sell to Porsche owners through an exclusive premium brand channel.

Mile Auto acquired 62 years of Southeast agency relationships and crossed the $100M premium threshold in one transaction. The technology was already there. The distribution was the missing piece. Now both are in the same entity.

Special Situation: Zurich / Beazley — EU Clearance

£8.1B (~$10.8B) | European Commission Clears World's Largest Specialty Insurance M&A Date: July 7, 2026 (EU clearance)

The European Commission cleared Zurich Insurance Group's £8.1 billion all-cash acquisition of Beazley plc under the simplified merger review procedure, concluding the transaction "would not raise competition concerns." This removes the most significant outstanding regulatory hurdle for the deal announced March 2, 2026 (after two rejected proposals in January at 1,230p and 1,280p per share, with the accepted offer at 1,335p per share). Beazley shareholders voted 99.9% in favor in April 2026.

What remains before closing: UK FCA/PRA approval (underway, PRA leads), Swiss FINMA clearance, Lloyd's of London consent, and court sanction of the Scheme of Arrangement. Closing remains targeted for H2 2026.

Why it matters for the market:

The combined entity will write approximately $15 billion in specialty gross written premiums annually, becoming the world's leading specialty underwriter with Beazley's Lloyd's platform as the London market anchor. The strategic rationale centers on three assets Beazley brings: its cyber insurance franchise (Full Spectrum Cyber combining coverage, incident response, and proactive security services), its Lloyd's platform (direct access to London market syndicate capacity), and its specialty underwriting expertise in cyber, marine, professional liability, and complex property.

Zurich's CEO Mario Greco stated at announcement: "Together with Beazley, we will create the world's leading specialty underwriter." The deal is expected to unlock $150M in annual cost savings by 2029 and $1B+ in incremental revenue opportunities in the medium term, funded through $3B in existing cash, $2.9B in new debt, and a $5B capital raise completed in March 2026.

The competitive consequence: The combination of Zurich's global distribution network with Beazley's specialty underwriting depth creates a $15B specialty platform that AXA XL, Chubb, Liberty Mutual, and Travelers will all measure themselves against. In cyber specifically, Beazley's Full Spectrum Cyber product — one of the most comprehensive cyber insurance offerings globally — becomes deployable through Zurich's worldwide corporate client relationships.

Zurich just cleared its biggest regulatory hurdle for the acquisition that will make it the world's largest specialty underwriter. The transaction is on course. The insurance industry's specialty competitive landscape is about to reorganize around a $15B platform.

4. Panora (France)

$4.5M Seed | AI Platform for B2B Insurance Brokers — European Expansion Date: July 7, 2026

Founded by Diane Roujou du Paty (CEO), Paris-based Panora raised a $4.5M seed round led by ISAI, with participation from Kima Ventures, 100in, 199 Ventures, and fintech angel investors. Panora builds an AI platform for B2B insurance brokers, covering three interconnected workflows: quote management (launching quote requests directly from the platform), policy analysis and comparison (uploading policy documents for AI extraction and structuring of coverage terms), and client proposals (converting analysis into professional, client-ready recommendations). Currently live in France, Belgium, and the UK. The seed capital funds team expansion and new European market entry beyond the current three-country footprint.

Why it matters: Panora is attacking the same problem that Carbon Underwriting (Lloyd's data platform, last week) and Outmarket AI (US brokerage automation, Week 20) are addressing from different angles — the broking workflow has not been meaningfully digitized despite decades of effort. The difference with AI-native platforms is the document comprehension layer: Panora can ingest policy documents, extract and structure coverage terms without manual data entry, and generate client proposals in one workflow. For European brokers operating across multiple markets with different policy form conventions and regulatory languages, that capability reduces both staff time and error rates on comparative analyses. ISAI's backing is notable: the Paris-based venture fund has a strong track record in B2B SaaS with Qonto, Doctrine, and Swile among prior portfolio companies.

A French AI platform for insurance brokers just raised its seed round with the investor that backed Qonto. The quote-to-proposal workflow that most European brokers still run on email and spreadsheets is the target.

Market Context: Brokerage Consolidation Accelerates

Sequel / Watkins | ALKEME / Eight Agencies | July 7 and July 1, 2026

Two brokerage consolidation announcements this week provide useful context for the week's broader theme of intentional capital allocation at every layer of the insurance distribution stack.

Sequel Insurance Agencies / Watkins Insurance Group (July 7)

Sequel Insurance Agencies — SIAA's dedicated perpetuation entity launched in 2025, backed by Odyssey Investment Partners — acquired Watkins Insurance Group, adding five Austin and Central Texas office locations and 160+ colleagues to the platform. Sequel now represents more than $550M in premium across its network. Patrick Watkins (CEO) remains in his role. The strategic differentiator: Sequel is explicitly not a conventional PE-backed consolidator. It offers agency owners a succession route that preserves brand, staff, and client relationships — a deliberate alternative to the rebrand-and-integrate model. Watkins, with more than 70 years in Central Texas, chose continuity over exit proceeds.

The model is significant: MarshBerry has reported insurance brokerage valuations at approximately 19% above their 10-year average, and multi-generational agencies are increasingly weighing succession against sale. Sequel's perpetuation-first proposition reaches owners who would not sell to a conventional consolidator at any price.

ALKEME Insurance / Eight Agencies (Q2 2026 wrap-up, announced July 1)

ALKEME Insurance — ranked Top 25 brokerage by Insurance Journal and the No. 3 fastest-growing broker in Business Insurance's Top 100 — announced eight agency acquisitions completed across Q2 2026, spanning seven states: New Jersey, Arizona, Georgia (two), Texas, New York, Colorado, and California. The agencies span commercial lines, personal lines, Medicare benefits, environmental specialty, apartment building coverage, and surplus lines — a deliberately diversified book-of-business acquisition strategy rather than a single-line roll-up. ALKEME has now completed over 80 acquisitions since founding in 2020.

The combined signal: Independent agency consolidation is running at sustained pace in the US market. Two structurally different models — Sequel's perpetuation-preservation approach and ALKEME's national footprint aggregation — are both active simultaneously, reaching different segments of the seller population. For founders and PE sponsors evaluating distribution assets, the breadth of buyer appetite across models and premium sizes is widening the exit opportunity set.

Brokerage consolidation is running at structural velocity, not cyclical pace. Sequel's perpetuation model and ALKEME's national aggregation are both active simultaneously — reaching different sellers with different succession priorities.