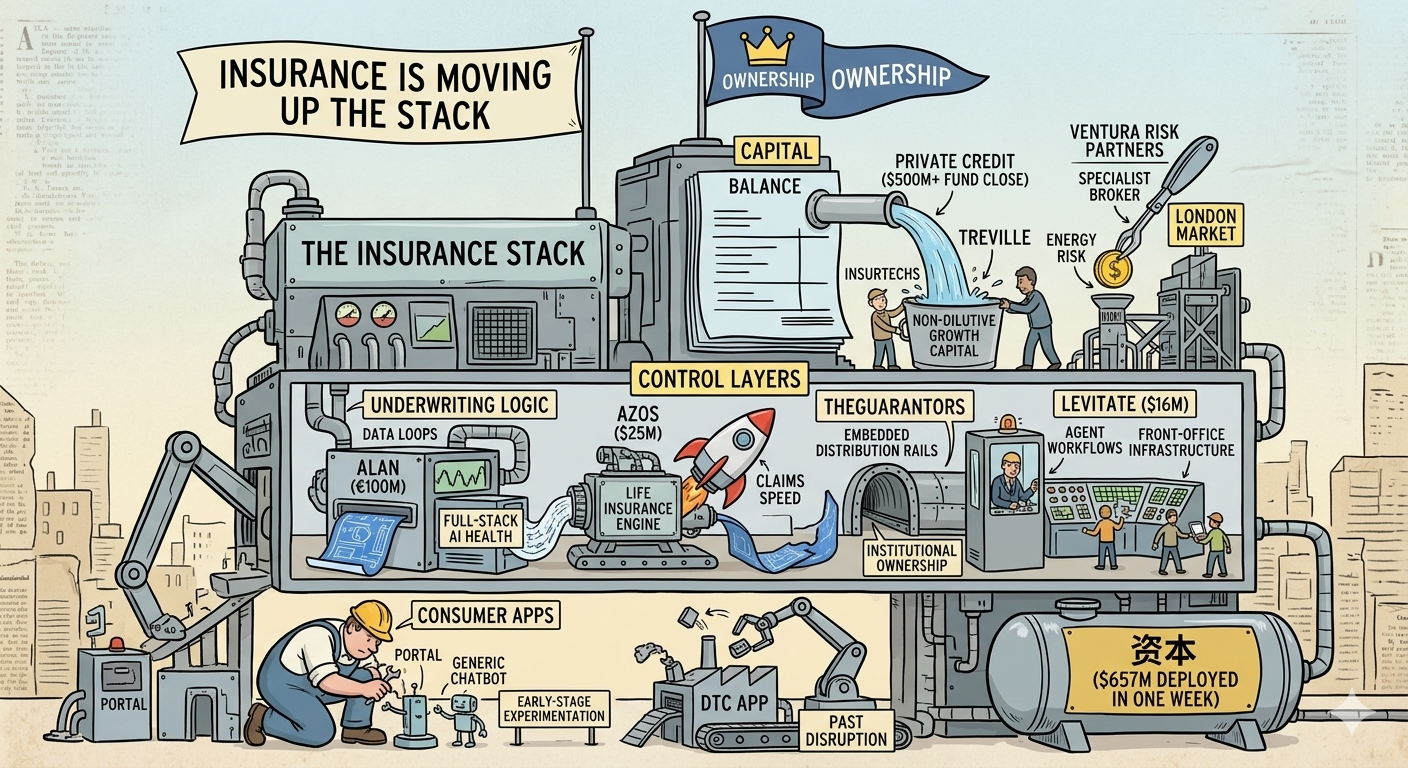

The past week saw ~$657M in disclosed capital flow into insurance and insurTech across eight transactions, with a clear shift toward late-stage growth equity, AI infrastructure, and capital solutions. Three mega-deals dominated: French health insurTech Alan raised €100M ($116M) at a €5–5.8B valuation, Warburg Pincus took a majority stake in lease-guarantee platform TheGuarantors (amount undisclosed), and Treville closed a $500M capital-solutions fund backed by insurers and institutions. The week also featured strategic specialist plays—Brazilian life insurTech Azos secured $24–25M for AI expansion, and B.P. Marsh seeded energy broker Ventura Risk Partners with equity plus a £2M loan. Growth investor Harbert Growth Partners led a $16M round into insurance CRM Levitate, with participation from Northwestern Mutual's venture arm, signaling carrier appetite for agent-facing AI tools.

Key themes:

- AI-native platforms win big – Alan, Azos, TheGuarantors all emphasize AI underwriting/operations

- Infrastructure over apps – Capital solutions (Treville), embedded rails (TheGuarantors) and specialist distribution (Ventura) dominate

- Strategic investors active – Northwestern Mutual Future Ventures, insurers backing Treville, Warburg Pincus control play

Detailed Deal Analysis

1. Alan (France) – €100M Growth Round at €5–5.8B Valuation

Date

- Announcement: March 10–12, 2026

- Execution: Round closed prior to announcement; specific date not disclosed

Investors & Target

- Target: Alan – French digital health insurer/insurTech platform combining insurance, telehealth, care navigation and wellness in one AI-powered app

- Lead investor: Index Ventures (growth fund)

- Other investors: Greenoaks, Kaaf Investments, SH Capital, Belfius (strategic Belgian bank/insurer), plus notable angels including Shopify CEO Tobi Lütke and Wealthsimple co-founder Mike Katchen

Amount of Funds

- €100M (~$115–116M), lifting post-money valuation to €5–5.8B

Use of Funds

- International expansion beyond France into Belgium, Spain, Canada and other markets

- AI-enabled health platform development – integrating insurance underwriting, care delivery, preventive health and data analytics in a unified digital experience

- Potential M&A and product expansion focused on B2B employee benefits and embedded health services

Competition

- European digital health/benefits players (digital health insurers, TPAs, HR/benefits platforms bundling insurance)

- In new markets (Canada, Spain), entrenched group benefits carriers and legacy brokers

- Traditional health insurers building digital channels vs. digital-native platforms

Impact on Competition

- Raises UX + integrated care bar: Competitors now face a fully digital, app-native stack combining insurance, telehealth and wellness—forcing incumbents to respond with AI-backed care navigation rather than just policy admin improvements

- Consolidator positioning: At €5B+ valuation and near-breakeven operations, Alan becomes a potential acquirer rather than target, squeezing smaller regional insurTechs in France/Benelux

- Validation of integrated model: Proves investors will back category leaders with real ARR, cross-border traction and path to profitability at growth-equity scale

2. Azos (Brazil) – $24–25M Series C for AI Life Insurance Expansion

Date

- Announcement: March 13–18, 2026

- Execution: Series C completed at time of disclosure; specific closing date not provided

Investors & Target

- Target: Azos – Brazilian insurTech focused on individual life insurance with fully digital distribution via 11,000+ partner brokers and 20+ physical city presences

- Lead investors: Kaszek and early Facebook investor Kevin Efrusy

- Other investors: Endeavor Catalyst and unnamed strategic backers

Amount of Funds

- $24–25M Series C (reports vary slightly by source)

Use of Funds

- AI expansion across underwriting, claims and broker support – automation and data-driven risk selection

- Scale operations in Brazil, deepen distribution via broker network and physical presence

- Broaden product set for underserved mass-market life insurance customers

Competition

- Dominant Brazilian life carriers: Bradesco, Prudential and other established players controlling most individual life market share

- Emerging Latin American digital life insurers and bancassurance partnerships targeting middle-class segments

Impact on Competition

- Scaled challenger status: Azos manages over $21B in insured capital and >1% of Brazil's individual life market—this round cements it as a credible threat to incumbents

- AI-driven speed advantage: Aims to pay claims in ~5 days vs. industry standard weeks/months, forcing incumbents to accelerate digitization and service levels to defend share

- Price and UX pressure: Increased capital enables competitive pricing and enhanced customer experience in Brazil's individual life segment, especially term life and income protection

3. TheGuarantors (US) – Warburg Pincus Majority Growth Investment

Date

- Announcement: March 18, 2026

- Execution: Described as majority investment; closing subject to customary approvals, timing not disclosed

Investors & Target

- Investor: Warburg Pincus – Leading global private equity/growth investor

- Target: TheGuarantors – US lease-guarantee insurTech offering residential lease guarantees and security-deposit alternatives via AI-powered underwriting platform

Amount of Funds

- Amount undisclosed; characterized as "majority growth investment" (control deal)

Use of Funds

- Scale platform and distribution across US rental ecosystem, broadening housing access for millions of renters

- Accelerate AI underwriting and expand data/analytics capabilities

- Deepen integrations with property managers and owners

Competition

- Other deposit-alternative/guarantee providers: Rhino, Jetty and traditional surety/guarantor offerings

- Incumbent renters' insurance writers not offering integrated lease-guarantee products

Impact on Competition

- Category leader positioning: Warburg's capital and operating expertise position TheGuarantors as scaled leader, making it harder for smaller guarantee insurTechs to compete on product breadth, AI underwriting and distribution relationships

- Consolidation catalyst: Could trigger M&A or strategic responses (partnerships, copycat products) from carriers and property-tech players as lease guarantees become standard in renting journey

- Embedded insurance validation: Control-style growth PE deal into AI-native risk infrastructure embedded in non-traditional insurance flow (residential leasing) validates "invisible insurance rails" thesis

5. Levitate (US) – $16M Growth Round with Strategic Insurance Investor

Date

- Announcement: March 17, 2026 on Coverager; funding disclosed publicly early March 2026

- Execution: March 2026 venture round; specific closing date not provided

Investors & Target

- Target: Levitate (Real Magic, Inc.) – AI-powered relationship marketing/light-CRM platform used heavily by insurance agents, financial advisors and relationship-heavy SMBs

- Lead investor: Harbert Growth Partners

- Other investors: Northwestern Mutual Future Ventures (strategic venture arm) and Bull City Venture Partners

Amount of Funds

- $16M venture round (Series C+ stage, total funding now ~$71M)

Use of Funds

- Accelerate AI roadmap and product development for automated, personalized outreach across email, text and social channels

- Expand team (product, engineering, go-to-market) and deepen penetration in core verticals including insurance and wealth management

Competition

- Horizontal CRMs and marketing tools: HubSpot, Salesforce, Mailchimp

- Niche agent-focused CRMs in P&C and life insurance

Impact on Competition

- Insurance-specific workflow advantage: Strategic capital from Northwestern Mutual enables sharpening of insurance-specific workflows, potentially displacing generic CRMs within agency and advisor channels

- Pressure on legacy vendors: Legacy agency-management vendors must add AI-driven relationship marketing features, not just policy admin

- Carrier demand signal: Northwestern Mutual's venture participation signals carrier appetite for front-office AI tooling

6. Treville – $500M Capital Solutions Fund Closing

Date

- Announcement: March 20, 2026

- Execution: Fund closed at >$500M at announcement; prior closings not dated publicly

Investors & Target

- Investors: Mix of insurers and institutional investors (names not disclosed)

- Target: Treville Capital Solutions Fund – Inaugural private credit/capital-solutions vehicle providing structured financing to middle-market companies including insurance/financials mandates

Amount of Funds

- "Over $500M" in committed capital

Use of Funds

- Asset-backed and structured credit solutions including warehouse lines and bespoke lending to sponsors and operating companies

- For insurance/insurTech: warehouse and credit provider—e.g., co-provides $95M warehouse to AI healthcare platform Nitra alongside Encina to scale receivables and card volume

Competition

- Other private credit funds and insurance-backed capital solutions providers: Ares, HPS, Apollo/Atelier-style strategies financing platforms, MGAs or distribution via credit rather than equity

Impact on Competition

- Alternative capital source: Adds insurer-friendly private credit player funding premium finance, warehouses and embedded-finance plays, giving insurTechs alternatives to bank lines or pure VC

- Deal flow competition: Increases competition among private credit funds targeting insurance-adjacent assets (premium finance, policy receivables, embedded lending)

Special Note

- This is a capital-solutions platform, not single startup round—can quietly power multiple insurTechs via warehouses and facilities, reflecting how insurers now deploy balance sheet via private credit rather than only equity funds

7. B.P. Marsh & Partners → Ventura Risk Partners

Date

- Announcement: March 20, 2026 on Coverager; investment announcement dated March 17–18, 2026 by B.P. Marsh

- Execution: Investment completed by mid-March 2026; effective on announcement (Ventura launched with B.P. Marsh backing)

Investors & Target

- Investor: B.P. Marsh & Partners Plc – Specialist investor in early-stage financial services/insurance businesses

- Target: Ventura Risk Partners Holdings Limited – Start-up energy insurance broker focused on placing North American energy risks into Lloyd's and London market

Amount of Funds

- 25% equity stake for nominal cash consideration, plus £2M loan facility to fund growth and working capital

Use of Funds

- Capital to build out brokerage, hire producers and support staff, secure regulatory and operational infrastructure to trade in Lloyd's/London market

- Loan facility backs early client acquisition and pipeline development for complex North American energy risks

Competition

- Established London-market energy brokers: Miller, Aon, Marsh, Howden placing upstream, midstream and downstream energy risks

Impact on Competition

- Specialist advantage: B.P. Marsh capital and governance support allow Ventura to punch above start-up weight, potentially winning niche energy accounts from larger brokers that may be less specialized or slower

- Niche-player strategy: Underlines B.P. Marsh approach of seeding specialist boutiques that chip away at global brokers in high-margin niches like energy

Special Cases: Two Standouts

Special Case 1: Alan – InsurTech at Mega-Valuation, Near Profitability

Alan's round is highly unusual because it combines late-stage growth capital with operational profitability in its core market and a €5–5.8B valuation for a still-private insurTech. This shows investors are willing to back category leaders with real ARR and cross-border traction, even as they remain cautious about earlier-stage insurTechs.

Why it matters for competition:

This is a signal event that effectively crowns Alan as a European "platform" player in health benefits, likely to be a future acquirer rather than target, and validates integrated care + insurance as a defensible, venture-backable model at scale. Competitors now face a well-capitalized adversary with proven unit economics, international expansion capacity, and strategic backing from both financial and strategic investors.

Special Case 2: Azos – AI-Centric Challenger in Concentrated Life Market

Azos' Series C is notable because it explicitly funds AI expansion at scale—underwriting, claims and broker tooling—in a market still dominated by a few large life insurers (Bradesco, Prudential). With >1% market share and >$21B insured capital already, the new capital accelerates a data-driven challenger that could structurally shift Brazil's individual life market toward faster, more digital experiences.

Why it matters:

This is a clear test case for how far a well-funded insurTech can move the needle in a traditionally low-penetration, oligopolistic life market using AI and hybrid (broker + digital) distribution. If Azos continues to scale and compress claims cycles (target: 5-day claims vs. industry weeks/months), it could force industry-wide service-level improvements or trigger defensive M&A by incumbents.

Sector Themes & Strategic Implications

1. AI-Native Platforms Win Big Capital

All major deals (Alan, Azos, TheGuarantors, Levitate) emphasize AI underwriting, operations or customer engagement. Investors are backing platforms that are AI-first, not AI-retrofitted.

2. Infrastructure Over Consumer Apps

The week saw capital flow to infrastructure and rails—capital solutions (Treville), embedded platform (TheGuarantors), specialist distribution (Ventura)—rather than direct-to-consumer insurance apps.

3. Strategic Investors & Control Deals

- Northwestern Mutual Future Ventures backing Levitate signals carrier appetite for agent-facing tools

- Warburg Pincus control stake in TheGuarantors shows PE willingness to take majority positions in scaled insurTech infrastructure

- Insurers anchoring Treville's $500M fund reflects balance-sheet capital deployment via private credit

4. International Expansion & Cross-Border Plays

- Alan expanding to Canada, Spain, Belgium

- Azos deepening Brazil footprint with potential LATAM expansion

5. Embedded & "Invisible" Insurance Growth

TheGuarantors (lease guarantees embedded in rental process) represents embedded insurance rails becoming critical infrastructure.

Market Impact Summary

| Deal | Primary Impact | Secondary Effect |

|---|---|---|

| Alan €100M | Validates integrated health platform model at mega-valuation; positions Alan as acquirer | Pressures European health insurers to match AI + care integration or lose talent/members |

| Azos $25M | Accelerates AI-driven claims/underwriting in concentrated Brazil life market | Forces incumbents (Bradesco, Prudential) to improve service levels or face share loss |

| TheGuarantors (Warburg) | Control PE validates lease-guarantee category; consolidation likely | Smaller deposit-alternative players face capital disadvantage; may trigger M&A |

| Levitate $16M | Strategic carrier VC (Northwestern Mutual) backs agent AI tooling | Legacy AMS vendors must add AI marketing or risk displacement by specialized tools |

| Treville $500M | Insurer balance sheets deploy via private credit fund; alternative to VC for insurTech | Increases competition for premium finance, warehouses; more non-dilutive capital available |

| Ventura (B.P. Marsh) | Specialist energy broker seeded with equity + loan | Niche brokers can compete with global players if well-capitalized; validates specialist strategy |

Competitive Landscape Shifts

For Incumbents:

- Must match AI speed and UX or risk losing talent, customers and producers to well-funded challengers (Alan, Azos impact)

- Embedded distribution becoming table stakes—need partnerships with SaaS platforms or risk disintermediation (TheGuarantors impact)

- Front-office AI tooling now expected by agents/advisors—carriers without agent-facing AI may lose distribution (Levitate impact)

For InsurTech Competitors:

- Scale matters: Late-stage deals (Alan, TheGuarantors) show investors backing category leaders with traction; smaller players face capital disadvantage

- Specialist positioning works: Niche plays (Ventura energy) can attract capital if deeply specialized

- AI is minimum viable: All funded companies emphasize AI underwriting/operations/engagement—non-AI platforms increasingly unfundable

For Investors:

- Growth equity and control deals dominate: VC/PE shifting from seed/Series A to later-stage growth and majority investments (Warburg, Harbert, Index)

- Strategic co-investment rising: Carrier venture arms (Northwestern Mutual) and insurers (Treville LPs, Belfius in Alan) actively deploying

- Infrastructure thesis validated: Capital flowing to rails/platforms (Treville credit, TheGuarantors guarantees) vs. direct carriers

#InsurTech #VentureCapital #PrivateEquity #InsuranceInnovation #AI #EmbeddedInsurance