1. Loxa – £2.7m Seed Round for EU Embedded Insurance Expansion

Date

- Announcement: March 12, 2026

- Execution: Seed round closed in three tranches prior to announcement (exact close dates not disclosed)

Investors and Target

- Target: Loxa, a UK-based insurtech focused on embedded insurance distribution via retail partners and e-commerce platforms

- Investors: Angel investors and family offices, including the Lazaroo-Hood Group; full syndicate not publicly disclosed

Amount of Funds

- Total raise: £2.7 million (~$3.4 million)

Use of Funds

- EU market expansion, particularly building presence in continental Europe beyond the UK

- Growing retail partner network to embed insurance at point-of-sale

- Enhancing technology platform for seamless policy servicing and distribution analytics

Competition

- Embedded insurance orchestrators: Qover (Belgium), Element (UK/EU), Wefox's distribution technology arm

- B2B2C insurance platforms serving retailers, vertical SaaS, and affinity partnerships

- Traditional bancassurance and affinity programs with slower, less data-driven integration

Impact on Competition

- Raises technical and operational bar for embedded distribution in EU retail, forcing rivals to improve API integration speed, data analytics, and regulatory multi-market capabilities

- Puts pressure on traditional affinity models that lack real-time data and customer engagement features

- Positions Loxa as an attractive infrastructure partner for insurers seeking rapid retail distribution scale without building proprietary platforms

2. Gangkhar – $4.25m Seed Round for AI-Native Embedded Protection in Emerging Markets

Date

- Announcement: March 9–12, 2026

- Execution: Seed round closed shortly before announcement (exact signing date not disclosed)

Investors and Target

- Target: Gangkhar, an AI-native embedded protection infrastructure platform targeting emerging markets, particularly Latin America; led by former Chubb executive Federico Spagnoli

- Investors: Seed round led by Anthemis, with participation from Accion Venture Lab, Sancor Ventures, Seedstars, EWA Capital, Simma Capital, and other fintech/insurtech investors

Amount of Funds

- Total raise: $4.25 million

Use of Funds

- Accelerate AI-driven product development and optimization capabilities for embedded insurance

- Scale embedded protection infrastructure globally, with primary focus on Latin American markets

- Expand partnerships with insurers and distribution channels in under-penetrated emerging markets

- Build regulatory capabilities and carrier relationships leveraging founder's deep carrier experience

Competition

- Other embedded insurance infrastructure providers targeting emerging markets and financial-inclusion segments

- Regional MGAs and carriers offering traditional distribution without AI-driven underwriting or real-time data integration

- Fintech super-apps in LatAm building insurance features in-house rather than partnering with specialized infrastructure providers

Impact on Competition

- Gangkhar's combination of pedigree capital (Anthemis, Accion) and founder expertise (ex-Chubb) positions it as a credible partner for tier-1 carriers seeking embedded distribution in emerging markets

- Forces regional competitors to match AI sophistication, data integration speed, and regulatory compliance—or risk losing carrier partnerships

- Impact-investing participation (Accion, Seedstars) signals that financial inclusion via embedded insurance is now a proven VC thesis, not just a CSR narrative

3. Jazz – $61m Growth Round with MassMutual Ventures

Date

- Announcement: March 11, 2026

- Execution: Growth round likely closed in Q1 2026, pre-announcement

Investors and Target

- Target: Jazz, an insurance/insurtech-related platform (context suggests digital distribution, risk management, or financial-wellness with insurance adjacency)

- Investors: Syndicate including MassMutual Ventures (confirmed participant); other co-investors not fully disclosed

Amount of Funds

- Total raise: $61 million

Use of Funds

- Heavy scaling: sales, marketing, and geographic expansion typical of $50m+ growth rounds

- Product development and expansion into adjacent coverage types or embedded offerings

- Strengthening partnerships with insurers and potentially building out enterprise sales teams for B2B2C distribution

Competition

- Other well-funded growth-stage platforms in digital distribution, financial wellness, or AI-enabled intermediary segments

- Traditional insurers and brokers whose customer relationships Jazz may intermediate or disintermediate

- Competing insurtechs at similar scale seeking to become category-defining brands in their niches

Impact on Competition

- With $61 million in new capital, Jazz can invest aggressively in brand, product velocity, and market share—potentially crowding out smaller players in its segment

- Strategic backing from MassMutual Ventures (a carrier-affiliated VC) suggests Jazz has proven its ability to drive real distribution or premium volume for carriers, raising expectations for competitors to show similar traction

- Competitors may need to respond with sharper pricing, more personalized products, or their own strategic carrier partnerships to maintain relevance

4. Kayna – €1.5m ($1.7m) Seed Round for Embedded Insurance in Vertical SaaS

Date

- Announcement: March 10–11, 2026

- Execution: Seed round closed in early 2026

Investors and Target

- Target: Kayna, an Irish insurtech providing embedded insurance infrastructure for business software companies and vertical SaaS platforms

- Investors: Seed round led by Delta Partners, with participation from existing investors MiddleGame Ventures and Aperture, plus new investors including Leo Capital and others

Amount of Funds

- Total raise: €1.5 million (~$1.6–1.7 million)

Use of Funds

- Expansion into UK and US markets, establishing commercial presence in both geographies

- Building embeddable insurance APIs and workflow integrations tailored to vertical SaaS (e.g., field services, professional services, construction tech)

- Regulatory and compliance work to support multi-market embedded distribution across EU, UK, and US

- Early go-to-market with key vertical SaaS partners and initial hires in target markets

Competition

- Embedded insurance orchestration platforms: Loxa, Qover, and other B2B2C embedded APIs targeting vertical software

- Incumbent carriers' white-label programs that integrate manually into software ecosystems

- Larger insurtech infrastructure providers expanding from payments or core systems into embedded distribution

Impact on Competition

- Kayna's explicit UK/US expansion plan intensifies competition in those markets, where embedded insurance adoption in vertical SaaS is accelerating

- Forces both insurers and vertical software providers to take insurance monetization more seriously—software companies that delay embedding insurance risk losing ancillary revenue to competitors who integrate with platforms like Kayna

- Carriers without strong API-first distribution capabilities may find themselves relegated to capacity providers behind embedded platforms, losing direct customer relationships

5. Unreasonable Labs – $13.5m with MS&AD Ventures Participation

Date

- Announcement: March 11, 2026

- Execution: Round likely closed in early 2026

Investors and Target

- Target: Unreasonable Labs, an insurtech/innovation-focused startup (name suggests experimentation platforms, AI tooling, or new distribution models for insurers)

- Investors: Venture syndicate including MS&AD Ventures, the VC arm of MS&AD Insurance Group (Japan-based global insurer)

Amount of Funds

- Total raise: $13.5 million

Use of Funds

- Scale experimentation and productization of insurance-related technology (e.g., AI proof-of-concept tools, new digital distribution channels, or innovation platforms for carriers)

- Deepen ties with strategic carrier partners like MS&AD, potentially co-creating products for Asian and global markets

- Hire engineering, product, and go-to-market teams to move from R&D to commercial deployment

Competition

- Other innovation-focused insurtechs offering experimentation platforms, AI tooling, or rapid prototyping for carriers

- Incumbent insurers' internal innovation labs and incubators

- Larger insurtech vendors expanding into adjacent innovation/analytics services

Impact on Competition

- Strategic backing from MS&AD Ventures signals that carriers are increasingly externalizing R&D and innovation into venture-backed entities that can move faster than in-house labs

- Competitors without similar strategic capital may struggle to keep pace in experimentation velocity, particularly in regulated and analytics-heavy domains like underwriting and claims

- Unreasonable Labs' funding validates the "innovation-as-a-service" model for insurers, potentially accelerating similar carrier-VC partnerships globally

6. Chowbus – $81m Growth Round for Restaurant Tech with Insurance Adjacency

Date

- Announcement: March 11, 2026

- Execution: Growth round likely closed in Q1 2026

Investors and Target

- Target: Chowbus, a platform providing POS systems, integrated marketing solutions, and AI-driven tools to restaurants

- While not a pure insurtech, Chowbus's deep integration into restaurant operations creates strong adjacency for embedded insurance products (e.g., business owner's policies, workers' compensation, cyber insurance)

- Investors: Growth investors (specific names not disclosed in available sources)

Amount of Funds

- Total raise: $81 million

Use of Funds

- Expand restaurant-tech footprint across markets and merchant base

- Enhance AI tools for menu optimization, marketing automation, and operational efficiency

- Creates option value to embed financial services and insurance offerings directly into restaurant workflows over time

Competition

- POS and restaurant-platform providers: Toast, Square, Clover, and others that have already begun embedding financial products and could also embed insurance

- Insurers and MGAs that sell restaurant insurance directly or via brokers—risk disintermediation if Chowbus partners with carriers to embed coverage at point-of-sale

- Other vertical SaaS platforms in hospitality/foodservice exploring embedded insurance

Impact on Competition

- If Chowbus partners with insurers to embed coverage (BOP, workers' comp, cyber), it could become a powerful distribution channel, capturing data and customer relationships ahead of traditional agents and brokers

- Competitors in restaurant tech (Toast, Square) may accelerate their own insurance partnerships, creating a race to own the "operating system" for restaurant risk and finance

- Traditional restaurant insurance brokers face potential disintermediation—merchants who buy insurance through their POS platform may bypass standalone brokers entirely

7. Alan – €100m Growth Round at €5bn Valuation

Date

- Announcement: March 10–11, 2026

- Execution: Growth round completed shortly before announcement

Investors and Target

- Target: Alan, a French digital health insurance and wellness insurtech serving individuals and enterprises across Europe

- Investors: €100m round led by existing investor Index Ventures, joined by Greenoaks, Kaaf, SH, plus angels including Tobi Lütke (Shopify founder) and Antoine Griezmann (footballer); Belgian bank-insurer Belfius also participated

Amount of Funds

- New capital: €100 million (~$116 million)

- Valuation: €5 billion post-money, up from €4.5 billion in 2024

Use of Funds

- Heavy investment in technology and AI, prioritized over near-term profitability push

- International expansion across Europe and product improvements, including scaling major contracts (e.g., health coverage for up to 135,000 French civil servants and families)

- Strengthen platform capabilities in telehealth, mental health, and integrated wellness services

Competition

- Traditional health insurers in France, Germany, Belgium, and other European markets

- Digital health and employee-benefits platforms offering overlapping services (e.g., Ottonova in Germany, other B2B2C health platforms)

- Large European insurers building their own digital health propositions to compete with pure-play insurtechs

Impact on Competition

- Alan's €5bn valuation and €785m ARR (+53% YoY) in 2025 demonstrate that top-tier investors still back scaled, near-break-even health insurtechs with proven unit economics and growth

- Raises competitive bar for smaller health-focused insurtechs and incumbents: peers must match Alan's speed of product iteration, AI adoption, and customer experience—or cede high-value employer and individual segments

- Traditional carriers face "build vs. partner" decision: invest billions to replicate Alan's digital platform, or partner/acquire to gain access to younger, tech-savvy customer base

8. Ualá – $195m Round Led by Allianz X for LatAm Financial Ecosystem

Date

- Announcement: March 4–6, 2026

- Execution: Equity round completed shortly before announcement

Investors and Target

- Target: Ualá, a Latin American fintech/neobank platform with embedded insurance offerings, scaling a comprehensive financial ecosystem across payments, banking, and insurance

- Investors: Round led by Allianz X (strategic investment arm of Allianz Group), with participation from Stone Ridge Holdings Group, Tencent, TABLE Holdings, Soros Fund Management, D1 Capital Partners, and other new and existing investors

Amount of Funds

- New capital: USD $195 million

- Valuation: Approximately $3.2 billion post-money

Use of Funds

- Scale Ualá's financial ecosystem across Latin America, including payments, digital banking services, and embedded insurance solutions

- Deepen and expand the Allianz–Ualá partnership, which previously supported Ualá's Series E totaling $366 million in 2024

- Expand into new LatAm markets and enhance product suite, combining Ualá's regional customer base with Allianz's global expertise in insurance and investment products

Competition

- Regional neobanks and super-apps: Nubank (Brazil), Mercado Libre's financial arm (Mercado Pago), and other LatAm fintechs partnering with insurers for embedded offerings

- Traditional banks and insurers attempting to build digital/embedded propositions without equivalent app engagement or customer data

- Other embedded insurance platforms targeting LatAm distribution (e.g., Gangkhar, regional MGAs)

Impact on Competition

- Strengthens Allianz's position in embedded insurance and digital distribution across LatAm by tying into a high-growth fintech with millions of engaged users, rather than relying solely on traditional agency or bancassurance channels

- Raises bar for other global insurers seeking LatAm distribution: partnering with large fintech platforms (or acquiring them) becomes more strategically urgent

- Traditional banks and carriers without strong digital ecosystems risk losing younger, mobile-first customers to super-apps that bundle banking, payments, and insurance in seamless UX

9. Lumen II Fund – Dedicated VC Vehicle for Italian Insurtech/Fintech

Date

- Announcement: Early March 2026

- Launch: Fund formation and first close in early 2026

Fund Structure and Investors

- Fund Managers: Ulixes Sgr and Lumen Ventures jointly launching "Lumen II" as a dedicated venture fund for insurtech, fintech, and digital health

- Limited Partners: Institutional LPs and private investors; specific LP names and total committed capital not fully disclosed in public coverage

Amount of Funds

- Fund size: Not clearly stated in available brief; described as a specialized fund with lead-investor strategy in Italy

Investment Focus

- Invest primarily in Italian insurtech, fintech, and digital health startups

- Emphasis on second-time founders and strong focus on gender balance in portfolio companies

- Position Lumen II as a lead investor to shape early-stage rounds and governance

Competition

- Other European insurtech-focused VC funds (e.g., CommerzVentures, Anthemis, Fin Capital) that also target Italian and Southern European dealflow

- Generalist Italian VC funds that invest across sectors but lack deep insurtech domain expertise

- Corporate venture arms of Italian and European insurers seeking direct startup investments

Impact on Competition

- Adds a new specialized capital source in Europe for early-stage insurtech, potentially improving funding access for Italian and regional startups versus relying solely on pan-EU or UK-based funds

- Other European insurtech VCs may face more localized competition for deal flow in Italy, especially around repeat founders with proven track records

- Italian insurtech startups now have credible local lead investor option, reducing need to relocate or pitch exclusively to non-Italian funds

10. Allied Trust – Sabine Re Ltd. Series 2026-1 Cat Bond ($100m Target)

Date

- Announcement: March 9–10, 2026

- Issue Date: March 2026, with maturity April 1, 2030

- Settlement: Expected in late March/early April 2026

Transaction Structure and Parties

- Sponsor/Cedent: Allied Trust Insurance Company, a Texas-domiciled P&C insurer writing property and homeowners insurance in Texas, Louisiana, North Carolina, and South Carolina

- Issuer: Sabine Re Ltd., a Bermuda-domiciled special purpose insurer (SPI)

- Investors: Catastrophe bond and ILS investors purchasing Series 2026-1 Class A principal-at-risk notes

Amount of Funds

- Target issuance: $100 million of Class A cat bond notes

- Actual pricing: Final size and spread to be confirmed at settlement; marketing indicated $100m target

Use of Funds

- Proceeds collateralize a multi-year named-storm reinsurance agreement for Allied Trust, providing three-year indemnity, per-occurrence protection against named storms in Texas, North Carolina, South Carolina, and Louisiana

- Supports staggered maturities in Allied Trust's reinsurance tower, diversifying capital sources and reducing reliance on traditional reinsurance

- This is Allied Trust's second Sabine Re cat bond issuance (first was Series 2024-1 for $100m), demonstrating repeat access to ILS markets

Competition

- Traditional reinsurance capacity from global and regional reinsurers

- Other ILS solutions: sidecars, collateralized reinsurance, quota-share funds

- Competing US regional carriers tapping cat bond market for property-catastrophe capacity (e.g., Heritage's Citrus Re series, other Florida and coastal carriers)

Impact on Competition

- Reinforces cat bonds as a core, repeatable component of regional carriers' reinsurance programs, not a one-off capital-markets experiment

- Encourages peers (other regional P&C carriers in cat-exposed states) to consider capital-markets risk transfer to complement or partially replace traditional reinsurance, especially as spreads and expected losses evolve

- Traditional reinsurers face ongoing competition from ILS for property-cat capacity; those without ILS fund-management capabilities may lose market share to hybrid reinsurers and ILS managers

11. Nascent Re – First Listed ILS Preferred Shares (€10m OFS Re)

Date

- Announcement: Early March 2026

- Listing: March 2026 (exact listing date not specified in brief)

Transaction Structure and Parties

- Issuer: Nascent Re, a reinsurance and retrocession facilitator active in matching reinsurance/retro risk and capital for investors and ILS fund managers

- Instrument: €10 million OFS Re preferred shares, listed as insurance-linked securities

- Investors: Institutional and qualified investors purchasing listed ILS preferred shares

Amount of Funds

- Issue size: €10 million (~$11 million)

Use of Funds

- Provide capital to support Nascent Re's reinsurance and retrocession risk-transfer activities

- Broaden investor base that can access ILS exposure via listed securities, as opposed to private funds or unlisted structures

- Demonstrate new wrapper/structure for ILS capital, potentially attracting investors who prefer listed, liquid securities over private placements

Competition

- Other ILS structures: cat bonds, collateralized reinsurance, sidecar funds, and private ILS funds

- Traditional reinsurance and retrocession capacity from global reinsurers

- Listed reinsurance equities and hybrid capital instruments issued by reinsurers

Impact on Competition

- Nascent Re's listed ILS preferred shares add a new structural option for ILS investors, potentially appealing to those seeking liquidity, transparency, or regulatory capital treatment that differs from unlisted funds

- Competes with other ILS managers and reinsurers for investor capital; success of listed format could encourage broader adoption and innovation in ILS capital structures

- Supports broader trend of capital-markets investors directly backing insurance risk through diverse structured products, reducing exclusive reliance on traditional reinsurance equity or debt

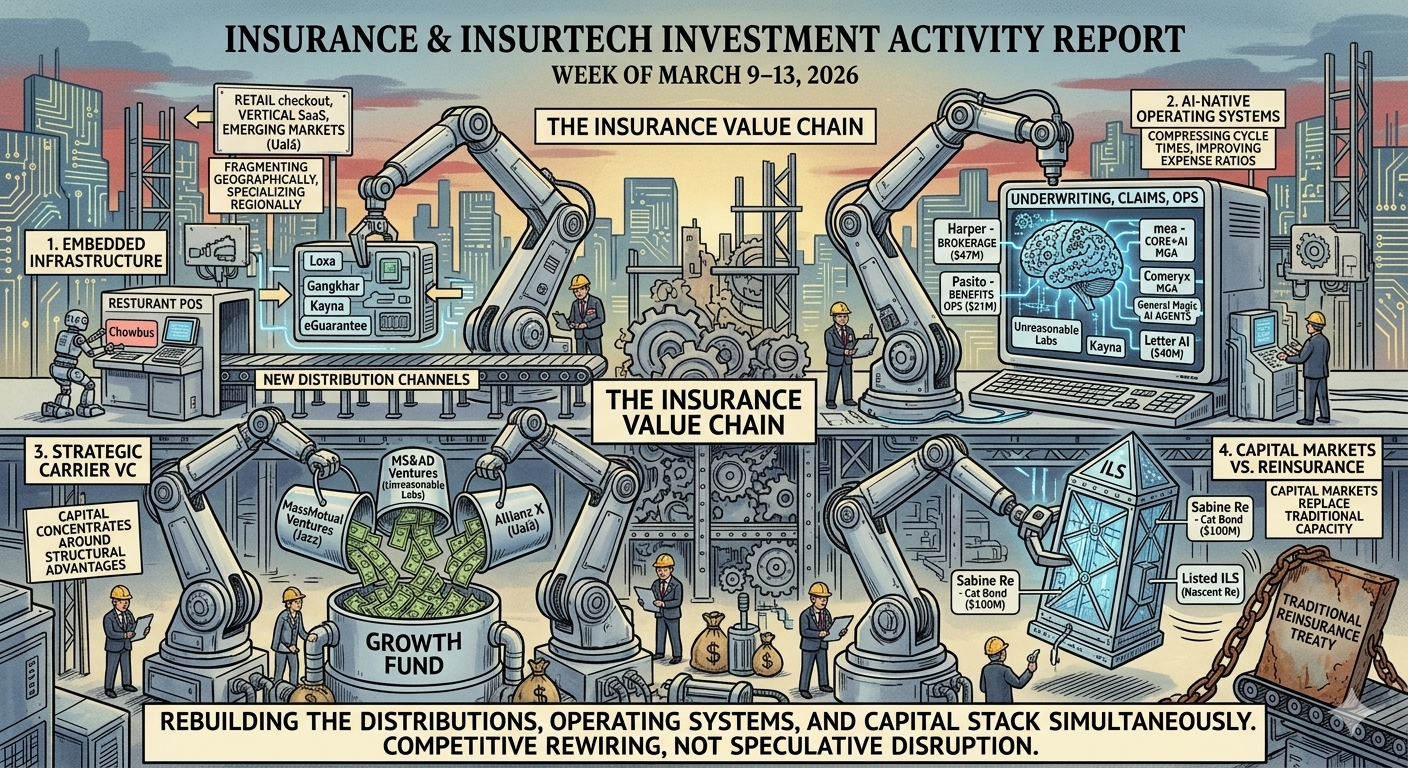

COMPETITION ANALYSIS: WHO WINS, WHO LOSES?

Embedded Insurance Infrastructure – Winners

Platforms: Gangkhar ($4.25m), Kayna (€1.5m), Loxa (£2.7m), and Ualá's embedded insurance features (backed by $195m Allianz X round) collectively represent over $210 million in capital flowing into embedded distribution.

Why they win:

- Control customer touchpoints at moment of purchase (retail checkout, vertical SaaS workflow, fintech app)

- Capture rich behavioral and transactional data that incumbents lack

- Offer frictionless UX that traditional agency/broker channels cannot match

- Backed by strategic investors (Allianz X, Anthemis, Delta Partners) who provide distribution partnerships, not just capital

Losers:

- Traditional agents and brokers in commodity lines (auto, SME commercial, embedded affinity) face disintermediation

- Incumbent carriers without strong API-first distribution risk becoming "dumb capacity providers" behind embedded platforms, losing direct customer relationships and pricing power

- Smaller embedded platforms without funding struggle to compete on multi-market regulatory compliance, carrier integrations, and go-to-market velocity

Health Insurtech at Scale – Alan's Market Signal

Platform: Alan (€100m at €5bn valuation, €785m ARR +53% YoY)

Why it matters:

- Demonstrates that investors still back scaled, near-profitable health insurtechs with proven unit economics—not just early-stage experiments

- Alan's choice to prioritize AI investment over near-term profitability signals confidence in long-term competitive moat via technology, not just customer acquisition

- Strategic participation from Belfius (bank-insurer) and Tobi Lütke (Shopify) suggests ecosystem partnerships (embedded health via e-commerce, bank distribution) are becoming critical

Competitive implications:

- Traditional European health insurers must decide: invest billions to replicate Alan's digital platform and AI capabilities, or partner/acquire to access younger, tech-savvy customer base

- Smaller health insurtechs without path to €500m+ ARR face existential pressure—consolidation or exit likely for subscale players

- Employers increasingly expect integrated wellness, telehealth, and mental health in health insurance offerings; carriers without these features lose enterprise deals to platforms like Alan

Capital Markets & ILS – Diversification Accelerates

Transactions: Allied Trust's $100m Sabine Re cat bond, Nascent Re's €10m listed ILS preferred shares, and Ualá's $195m Allianz X round all signal capital-markets innovation.

Why capital markets win:

- Regional carriers (Allied Trust) can access repeatable, multi-year cat capacity outside traditional reinsurance, reducing treaty negotiation friction and pricing volatility

- Listed ILS structures (Nascent Re) broaden investor base beyond private ILS funds, potentially improving liquidity and transparency

- Strategic insurer investments in fintechs (Allianz X → Ualá) create hybrid distribution models that combine carrier expertise with fintech scale

Losers:

- Traditional reinsurers without ILS fund-management capabilities lose property-cat market share to cat bonds and collateralized structures

- Insurers relying solely on traditional reinsurance face higher cost of capital and less flexible terms compared to peers diversifying into ILS and alternative capital

- Brokers and intermediaries in pure-placement roles (no data, no analytics, no capital) risk disintermediation as carriers access capital markets directly or via specialized ILS managers

MACRO CONTEXT: WHAT THE WEEK'S DEALFLOW REVEALS

1. THE "EMBEDDED OR IRRELEVANT" INFLECTION POINT HAS ARRIVED

The concentration of capital into embedded distribution this week — Gangkhar, Kayna, Loxa, and the Ualá-Allianz X partnership — is not a coincidence. It reflects a structural shift that has been building for several years and is now hitting an inflection point driven by three converging forces:

Vertical SaaS maturity: Platforms like Kayna's target partners (field services, professional services, construction tech) and Chowbus have reached sufficient scale and data depth that embedding insurance is no longer technically complex — it is a product decision. The infrastructure exists; the question is who builds the insurance layer on top of it.

Carrier API readiness: A critical mass of carriers and MGAs now have API-enabled quoting and binding capability, meaning embedded platforms can offer real-time insurance purchasing rather than directing customers to a separate flow. Without this, embedded insurance is just a referral program. With it, it is true distribution.

Consumer and SME behavior shift: Post-pandemic merchant and consumer behavior has permanently shifted toward managing business services — including insurance — within the software tools they use daily. Merchants who manage their business through Chowbus, their accounting through QuickBooks, or their operations through a field services SaaS increasingly expect insurance to be available there too — not as a separate relationship.

The competitive implication: Carriers and MGAs that have not yet defined their embedded distribution strategy — including which platforms to partner with, what API capabilities to build, and how to price for embedded channels — are falling behind a wave that cannot be stopped. The question is no longer whether embedded insurance will be a primary distribution channel; it is which carriers will own the best partnerships.

2. STRATEGIC CARRIER CAPITAL IS RESHAPING THE STARTUP COMPETITIVE LANDSCAPE

This week's rounds involving MassMutual Ventures (Jazz), MS&AD Ventures (Unreasonable Labs), and Allianz X (Ualá) are part of a broader pattern: carriers are using their venture arms not just to generate financial returns, but to shape which startups become infrastructure.

The competitive implication of this pattern is underappreciated. When a carrier-backed VC participates in a startup's round, it typically comes with:

Data-sharing agreements that improve the startup's model quality

Distribution partnerships that accelerate the startup's revenue growth

Regulatory navigation support in the carrier's home markets

An implicit signal to other carriers that this platform is worth partnering with

This means carrier-backed rounds compound: the first carrier to invest unlocks advantages that attract the next carrier partnership, which attracts the next. The startups that accumulate these relationships early — Jazz, Unreasonable Labs, and to a larger extent Ualá — build moats that are not purely technological. They are relational and data-driven, and extremely difficult for a later-entering competitor to replicate.

The carriers most at risk from this dynamic are those without dedicated, active venture arms who are watching competitors invest in and shape the next generation of insurance infrastructure. Every quarter they delay, the startups most worth partnering with become more expensive to acquire and less willing to offer preferential terms.

3. FROM "AI IN INSURANCE" TO "AI AS THE OPERATING SYSTEM OF INSURANCE"

The Crowdfund Insider analysis circulating this week — carriers demanding ROI proof from AI vendors — is directionally correct but misses the deeper structural shift visible in this week's deals.

The pressure on AI vendors to show tangible outcomes is real and healthy. But the more significant dynamic is that AI is no longer a feature being added to insurance platforms — it is becoming the foundation on which new insurance platforms are built.

Alan is not an insurer that added AI; it is a company that built an insurer on AI from day one and is now investing more heavily in AI as it scales. Gangkhar is not building an embedded insurance platform and layering AI on top; its AI capabilities are what enable it to serve emerging markets where traditional underwriting data is sparse. Unreasonable Labs is not retrofitting a legacy system with AI; it is building experimentation infrastructure for carriers that want to deploy AI without the organizational friction of doing it in-house.

The competitive implication of this shift:

For incumbents, the risk is not that AI vendors will replace them — it is that the carriers and intermediaries that partner with the right AI-native platforms will build structural cost and speed advantages that compound over time. A carrier whose underwriting, pricing, and customer-service workflows run on AI-native infrastructure will have expense ratios and cycle times that legacy competitors cannot match within their current technology architecture.

For insurtechs, the risk is the one the Crowdfund Insider piece correctly identifies: carriers have limited patience for AI pilot programs that do not translate to operational metrics. The insurtechs that survive and scale will be those that can point to specific loss-ratio improvement, submission-processing speed, or customer-retention metrics — not just proof-of-concept deployments.

4. CAPITAL MARKETS ARE BECOMING A CORE REINSURANCE STRATEGY, NOT AN ALTERNATIVE

Allied Trust's repeat cat bond issuance and Nascent Re's listed ILS preferred shares, taken together, reflect a maturing relationship between insurance risk and capital markets that is fundamentally changing the competitive dynamics of reinsurance.

The traditional reinsurance relationship was bilateral: carrier negotiates annually with a set of reinsurers, pricing determined by loss experience, capacity availability, and relationship quality. The carrier had limited alternatives and limited transparency into how reinsurers priced their risk aggregations.

The emerging model is multi-channel: carrier uses cat bonds for named-storm or specific-peril layers where ILS pricing is competitive, uses collateralized reinsurance for mid-layer risks, uses traditional treaty for relationship-based capacity, and retains more risk on layers where modeled expected loss is well understood. This portfolio approach gives carriers pricing leverage, structural flexibility, and reduced dependency on any single reinsurer relationship.

The broader competitive implication for the reinsurance industry: Traditional reinsurers who do not operate ILS fund management arms — or who lack the data and technology to offer carriers real-time portfolio analytics alongside capacity — will increasingly compete on price alone for commodity cat layers, while losing the strategic partnership role to reinsurers that offer a full capital-markets toolkit. The structural pressure on reinsurance pricing that ILS has exerted for