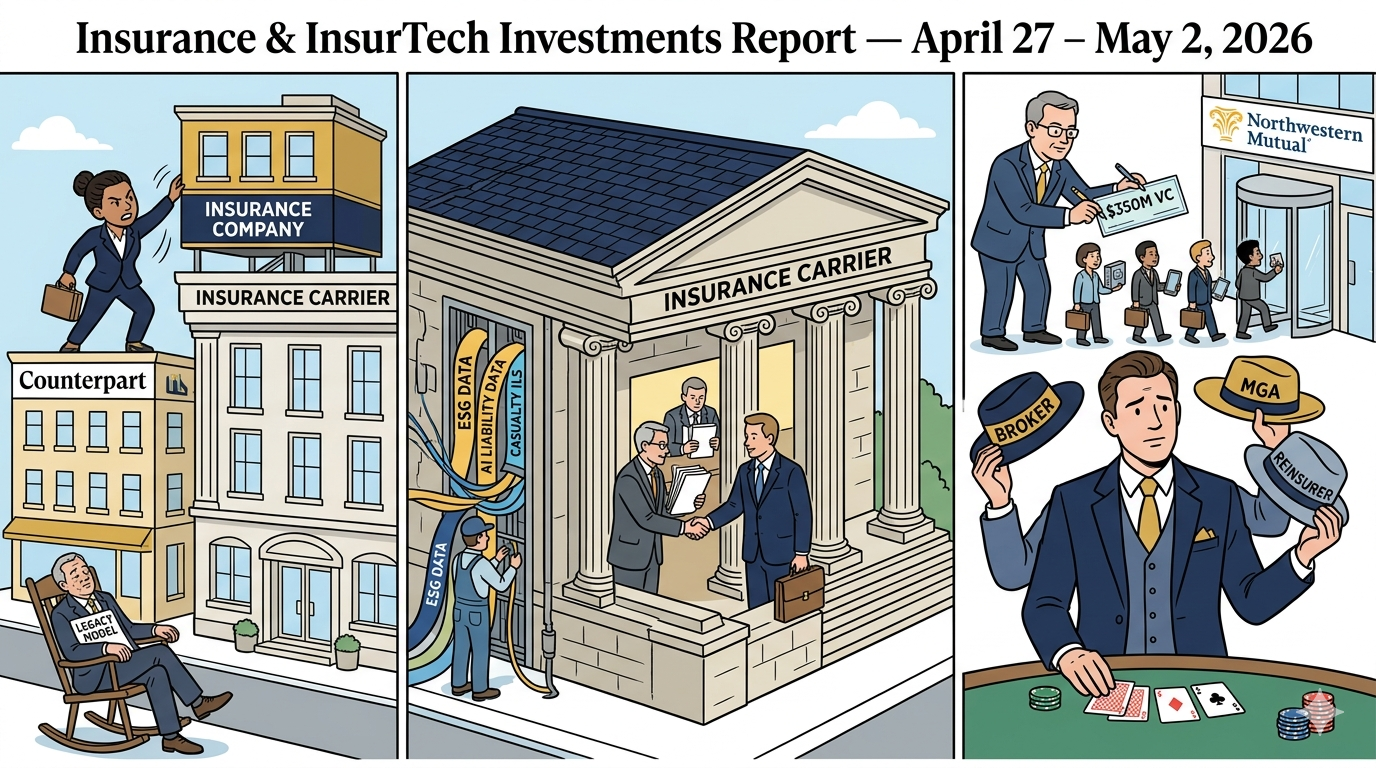

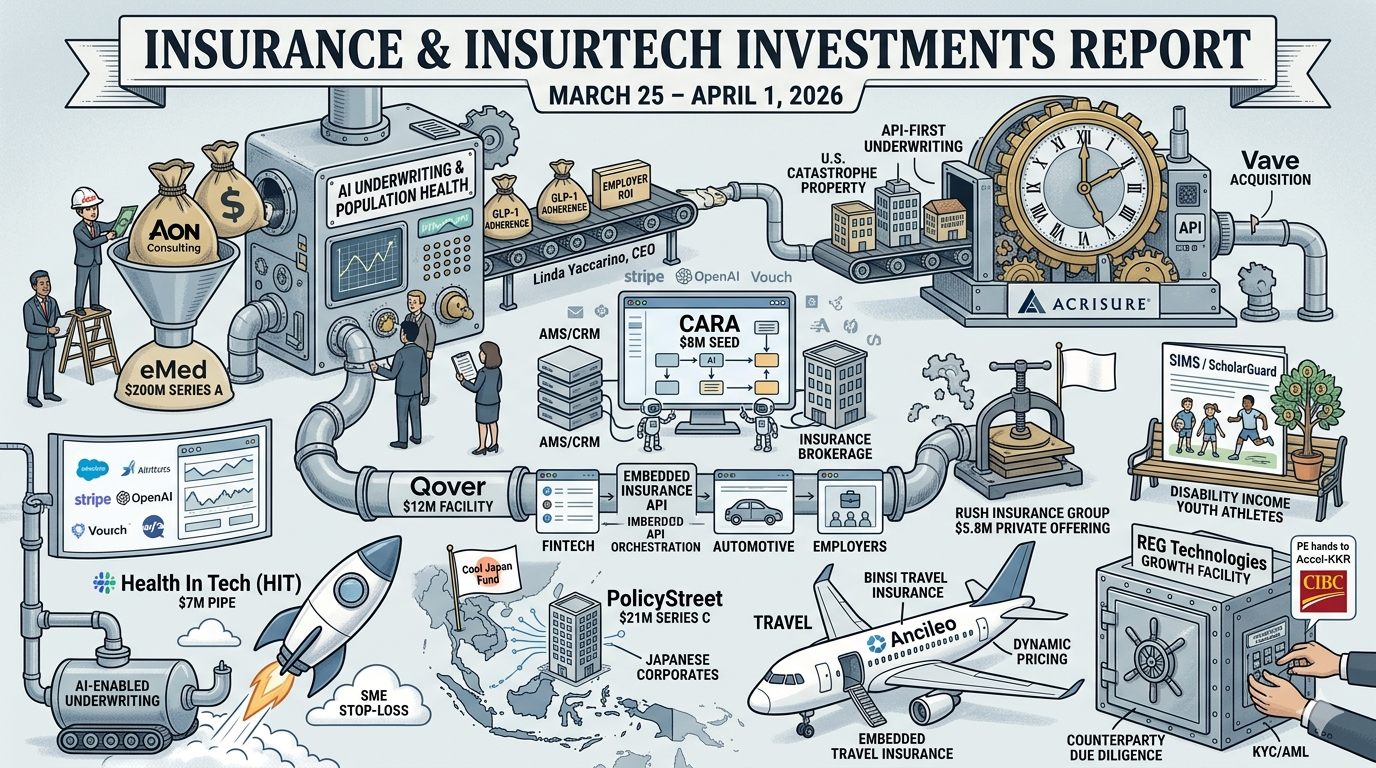

This week’s deal flow (March 29 – April 4) underscores a structural shift in insurance: distribution is consolidating around platforms, while AI and embedded infrastructure are redefining how products are built, sold, and serviced. From eMed’s $200M raise turning Aon into a direct distribution engine for GLP-1 population health, to Acrisure doubling down on API-first underwriting via Vave, the signal is clear—control is moving away from balance sheet providers and toward those who own access, workflows, and data. Across health, property, brokerage operations, and embedded insurance, capital is flowing to players that compress friction, integrate deeply, and scale distribution natively rather than incrementally.