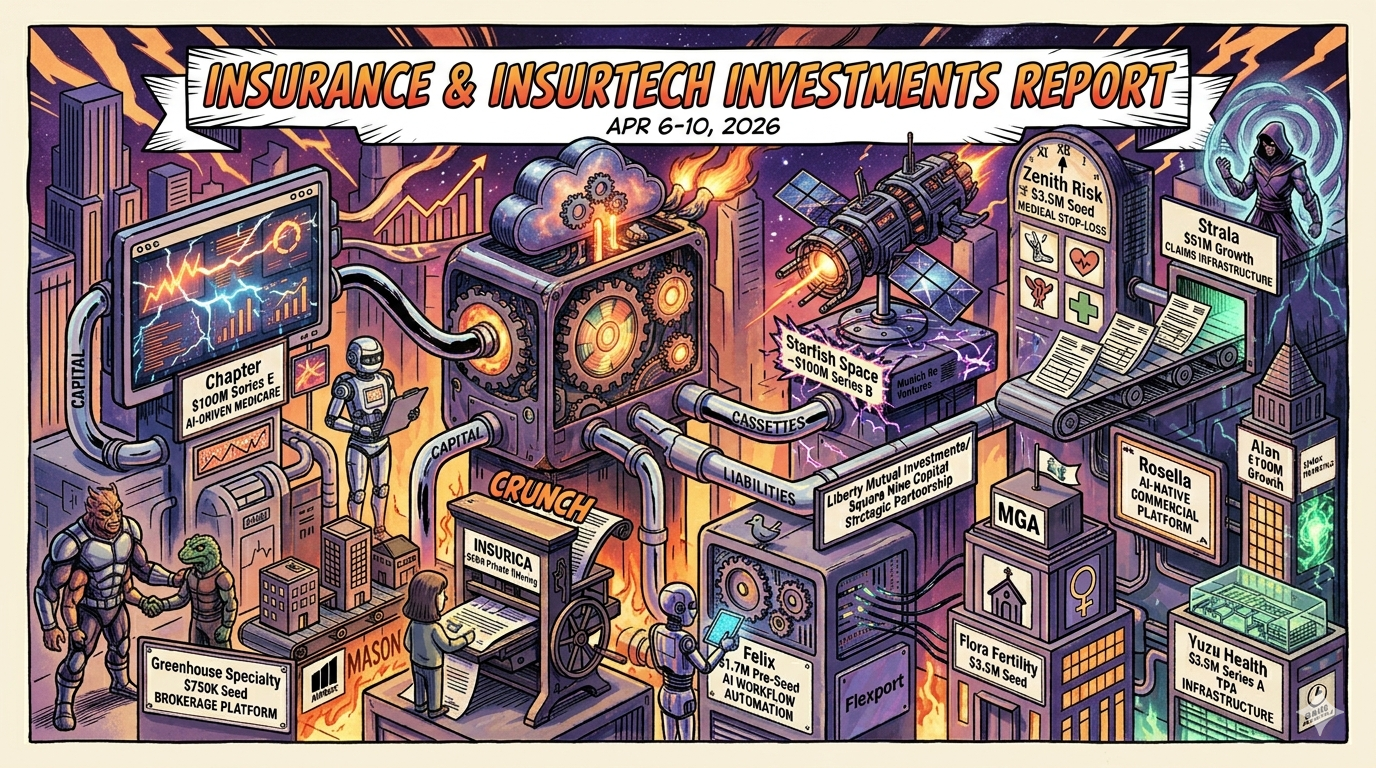

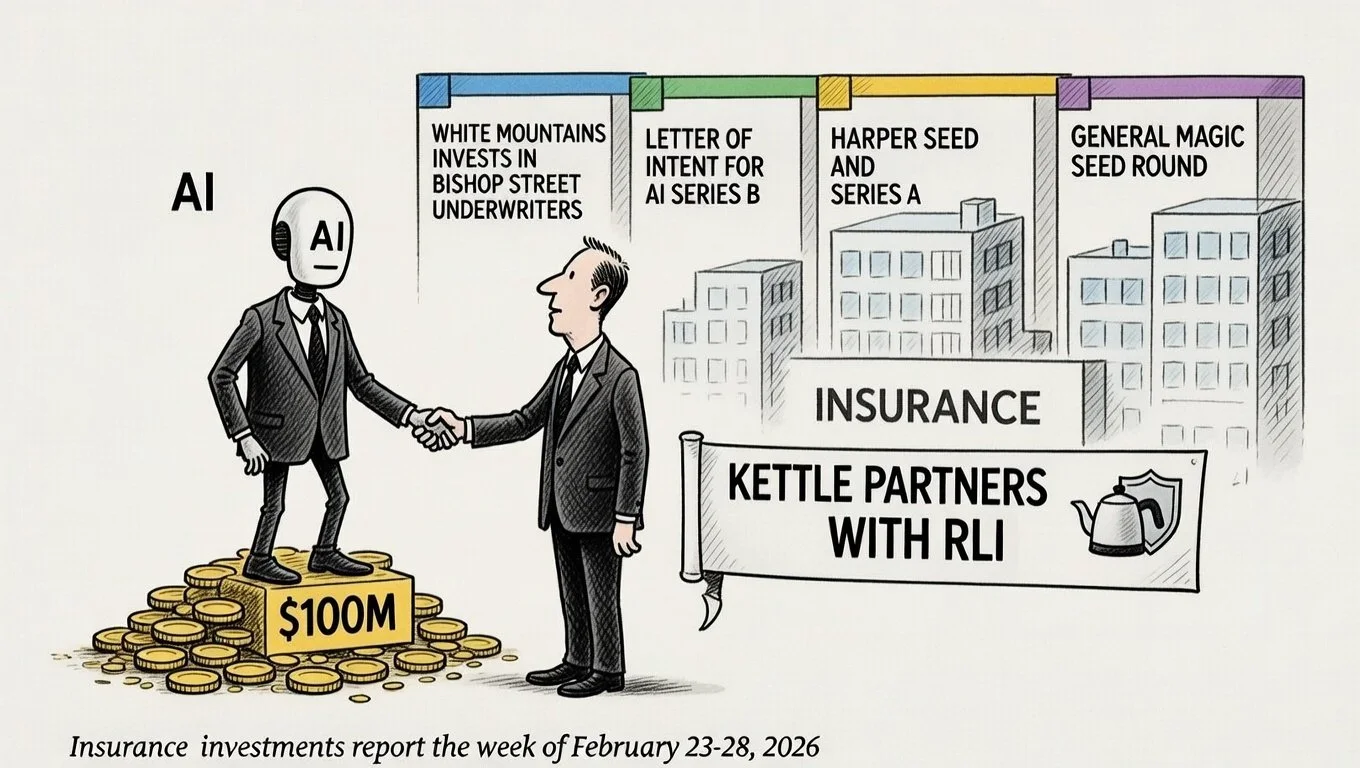

In the week of February 23–28, 2026, the insurtech sector resembled a gold rush where artificial intelligence was the only metal worth mining. White Mountains poured $125 million of structured capital into Bishop Street Underwriters, turning an MGA platform into something resembling a private-equity heavyweight. Meanwhile, carriers edged closer to the action: RLI took a strategic equity stake in Kettle, the AI-savvy MGA specialising in wildfire-exposed commercial property, securing both capacity and a front-row seat to better catastrophe models.