Insurance & InsurTech Investment Intelligence Report

Week of June 21–27, 2026

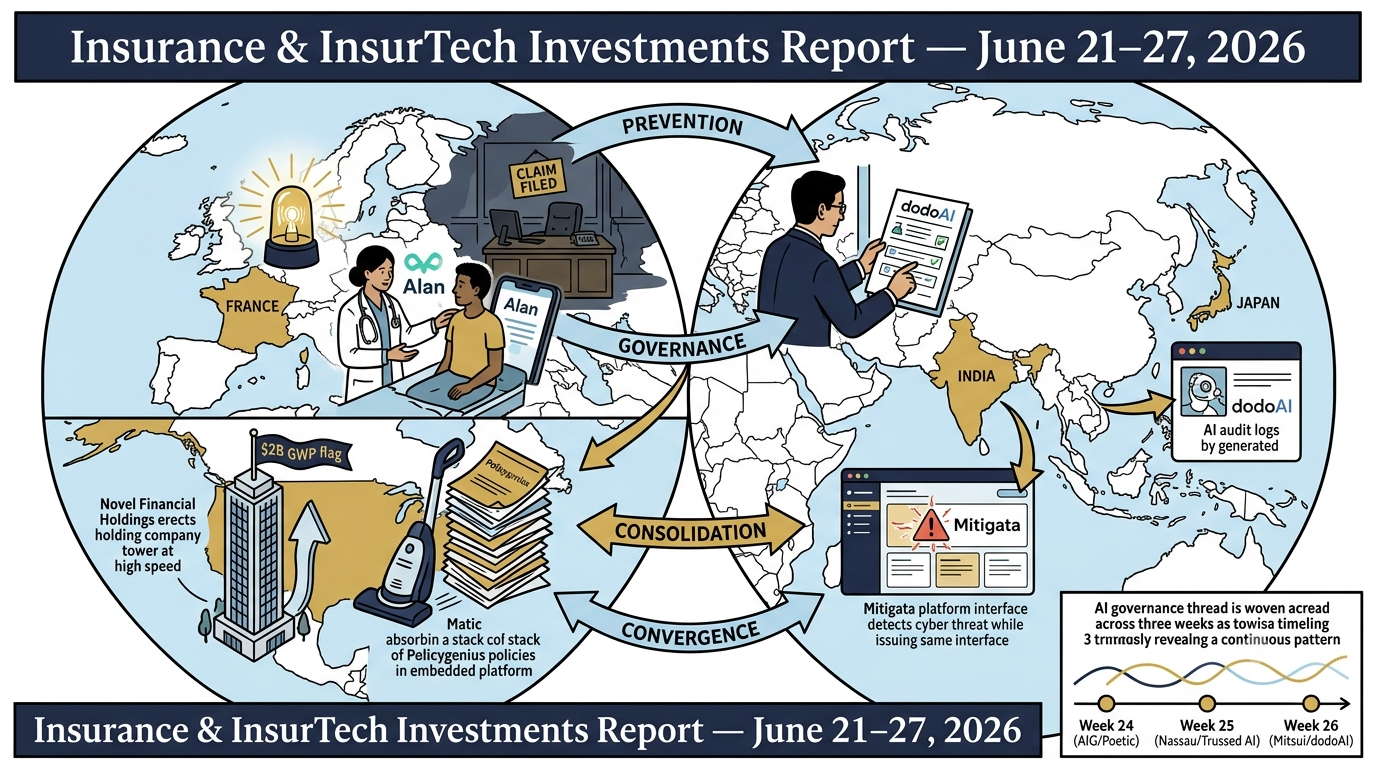

$608M+ in disclosed capital | 4 primary transactions + 4 special situations | Prevention insurance, agentic decisioning, and a carrier-built disaster stack

Alan's €480M Series G is the week's headline — Europe's largest non-AI raise of 2026, led by Prosus at a €5.5 billion valuation. The pattern around Alan: embedded insurance (Matic acquiring Policygenius's P&C book with PE backing), specialty holding company formation (Novel Financial Holdings / Flexpoint Ford), cyber insurance as integrated resilience platform (Mitigata in India). Four special situations add further dimension: IAG Firemark Ventures / Spacecube ($3M, June 26) closes the loop on Firemark's deliberately constructed four-layer disaster resilience portfolio — prediction, detection, psychological support, physical recovery — revealing the most complete carrier-owned disaster response stack assembled by any insurer globally; Taktile's $110M Goldman Sachs-led raise surfaces the most concrete AI claims automation benchmark of 2026 ($90M+ projected savings at a named global insurer); The Doctors Company closes its $12B MPL merger with ProAssurance; and dodoAI extends the AI governance thread to its third consecutive week and second continent. Together they describe an industry simultaneously expanding what insurance does — from reactive protection to proactive prevention — and tightening the infrastructure required to do it at scale.

1. Alan (France)

€480M ($550M) Series G at €5.5B ($6.3B) Valuation | Prevention Insurance — Europe's Largest Non-AI Raise of 2026

Date: June 25, 2026

What Happened

(Prior coverage note: Alan's Series G first tranche — €100M led by Index Ventures at a €5.0B valuation — was covered in the InsurTech.ME reports for the weeks of March 9–13 and March 16–20, 2026. This is a new, substantially larger second tranche with a new lead investor at a higher valuation, constituting a distinct capital event.)

Founded in 2016 by Jean-Charles Samuelian-Werve (CEO) and Charles Gorintin (CTO), Paris-based Alan is Europe's leading health insurtech and the architect of what it calls "prevention insurance" — a model that combines health coverage, care navigation, wellbeing services, and AI-powered health assistance in a single platform designed to keep members healthy rather than only compensating them when they become ill. Alan announced a Series G financing round of €480 million ($550M) led by Prosus — the Amsterdam-listed technology investor and operator whose portfolio spans food delivery (iFood, Just Eat Takeaway), fintech (PayU), and classifieds (OLX) across Europe, India, and Latin America. The round values Alan at €5.5 billion ($6.3B), an increase of at least €500 million from Alan's March 2026 Series G first tranche ($116M at €5.0B). Total funding across nine rounds now exceeds $1.3 billion. In Q1 2026, Alan surpassed €800M in annual recurring revenue, grew 53% year-over-year, serves more than 1.1 million members across 37,000+ businesses, self-employed professionals, and retirees in France, Spain, Belgium, and Canada — and is profitable in France. More than 850 employees. Closing subject to French regulatory approval (ACPR). The investment structure includes both primary equity and secondary share acquisition, providing select early stakeholders partial liquidity.

- Lead investor: Prosus (Fahd Beg, Head of Investments — €400M primary commitment)

- Existing investors: Teachers' Venture Growth (TVG), Index Ventures (both participating)

- New investor: Dara Holdings

Use of Funds

- International expansion into new countries beyond current four-market footprint

- Acquisitions to accelerate market entry and service breadth

- Continued investment in AI, healthcare services, and product development

- Alan Campus launch (January 2027) — digital health insurance for students aged 18–28

Strategic Thesis

Prosus is one of the world's largest consumer technology operators — not a healthcare investor. Its bet on Alan is explicitly a consumer platform bet, not a health bet. Fahd Beg's framing — "an integrated platform where insurance, prevention and care delivery reinforce each other, creating an exceptional healthcare experience" — describes the logic: Alan's platform generates daily engagement that food delivery and fintech platforms generate in adjacent verticals. Prosus's Large Commerce Model AI and its global network of consumer platforms (iFood, Swiggy, OLX) create distribution infrastructure that Alan can leverage for international expansion into markets where it lacks brand recognition or regulatory relationships. The exchange is bilateral: Alan gets a consumer distribution partner with global reach; Prosus adds a regulated health insurance platform to its lifestyle ecosystem, enabling cross-product health and wellness integration across its two billion customer base. Jean-Charles Samuelian-Werve's articulation of the category is precise and consequential: "Prevention should be too." If that category thesis proves correct — that consumers will pay a consistent premium for health insurance that keeps them well rather than only paying when they're sick — the TAM is not the European health insurance market. It is the global healthcare economy.

Why It Matters

- €800M ARR, 53% YoY growth, profitable in France: Alan enters this round from an operating position that most health insurtechs never reach — profitable in the core market while still growing at venture rates, providing Prosus with a fundamentally different risk profile than a pre-revenue bet

- Prosus's involvement transforms Alan's international expansion from a capital-constrained organic effort into a distribution partnership backed by one of the world's most experienced consumer platform operators — the question is no longer whether Alan can afford to expand but whether Prosus's consumer platform network accelerates regulatory and brand entry in new markets

- The €500M valuation step-up in under 90 days (March to June Series G) reflects institutional conviction re-pricing, not hype — Teachers' Venture Growth and Index Ventures both re-upped, providing continuity of informed investor conviction across the step-up

Competition

- Direct competitors (European health insurtech): Wefox (broker-led, Austria/Switzerland/Netherlands), Doctolib (appointment booking, France/Germany — adjacent but not insurance), Bupa (traditional private health, UK/Europe)

- Category competitors: National health systems (NHS, French Assurance Maladie, Belgian INAMI) which Alan supplements rather than replaces; traditional complementary health insurers (Axa Santé, Harmonie Mutuelle in France)

- Emerging dynamic: The "prevention insurance" category Alan is defining has no direct equivalent at scale — the competitive threat is not from incumbents replicating the model but from the model failing to translate across regulatory and cultural contexts as Alan expands internationally

Market Consequences

European health insurtechs without Alan's operating metrics — profitable core market, demonstrated retention, AI-native member experience, 1.1M+ member base generating longitudinal health data — face a competitive credibility gap that compounds as Alan's international expansion demonstrates the model's portability. Traditional French and European complementary health insurers (mutuelles, complémentaires santé) face a long-term structural challenge: Alan's AI-native care navigation generates daily member touchpoints that traditional insurers, interacting with members only at enrollment and at claim, cannot replicate. The longitudinal health data advantage this generates compounds — the more Alan knows about its members' health patterns, the more precisely it can intervene preventively, the better its loss ratios become, and the more it can reduce premiums for members who engage. For Prosus, the Alan investment represents the first major foray into regulated health insurance from a consumer technology conglomerate — if it works, expect Amazon, Apple Health, and Google Health to be asked whether they are next.

Bottom line: Prosus just paid €480M to bet that health insurance becomes a daily-engagement consumer platform rather than an annual enrollment product. Alan's €800M ARR and French profitability suggest the bet is not theoretical. The question is whether prevention insurance travels across borders the way food delivery did.

2. Novel Financial Holdings / Flexpoint Ford (USA)

Undisclosed | PE Investment in Diversified Insurance Holding Company — $2B GWP Platform Date: June 22, 2026

What Happened

Novel Financial Holdings, Inc. — a Jersey City, New Jersey-based diversified underwriting and insurance services holding company launched in May 2025 — announced a strategic investment from Flexpoint Ford, a specialist private equity firm focused exclusively on financial services and adjacent verticals. The investment is made from Flexpoint's Asset Opportunity Fund III and Insurance Opportunity Fund I — two dedicated vehicles, the latter explicitly insurance-focused. Novel was founded and is led by a team of insurance industry veterans: Chairman Jacques Bonneau (former CEO of PartnerRe) and CEO Rob Bredahl (former CEO of Howden Re). Novel manages both policyholder-owned reciprocal exchanges (through ownership of attorney-in-fact entities) and traditional stock insurance companies through direct ownership and service contracts. Across its platform, Novel-managed carriers write approximately $2 billion in annual gross written premium across multiple lines of business. A significant milestone: effective April 1, 2026, GeoVera Nova (specialty residential property insurer, catastrophe-exposed markets, AM Best rated A/Excellent) became a wholly owned Novel subsidiary, integrated with SageSure for underwriting, claims, and distribution. Terms undisclosed.

- Investor: Flexpoint Ford (Asset Opportunity Fund III + Insurance Opportunity Fund I)

- Novel leadership: Jacques Bonneau (Chairman, former PartnerRe CEO), Rob Bredahl (CEO, former Howden Re CEO)

- Flexpoint Ford context: 20+ year track record in financial services PE; prior insurance investments include Enstar (run-off), GeoVera, and other carrier/MGA platforms

Use of Funds

- Support continued build-out of Novel's diversified insurance platform

- Fund further acquisitions across underwriting and insurance services

- Expand balance sheet deployment across multiple lines and underwriting cycles

Strategic Thesis

Novel is building the modern equivalent of a diversified insurance holding company — combining fee income from attorney-in-fact management of reciprocal exchanges with operating results from owned insurance carriers. The model is structurally elegant: AIF management fees provide a stable, capital-light revenue stream that funds platform overhead; owned carrier operations provide the underwriting income and float that compound with scale. Rob Bredahl's architecture — one year in, $2B in GWP, AM Best A-rated catastrophe carrier absorbed — is exactly what Flexpoint's Insurance Opportunity Fund I was formed to back: a proven management team with institutional insurance credibility building a differentiated holding company structure. The Bonneau/Bredahl combination is perhaps the most credentialed founding team in recent insurance holding company formation — PartnerRe and Howden Re represent two of the most respected platforms in global specialty reinsurance and broking. The Flexpoint investment validates both the management quality and the structural model at a moment when insurance holding company formation is attracting increasing PE interest as the underwriting cycle creates favorable conditions for well-capitalized new entrants.

Why It Matters

- $2B in gross written premium across Novel-managed carriers at 13 months post-launch is an extraordinary commercial traction figure for a startup holding company — this is not a concept being capitalized, it is an operating platform at meaningful scale

- Flexpoint's Insurance Opportunity Fund I is a dedicated vehicle for exactly this type of investment — not a generalist PE fund making an opportunistic bet, but a specialist with 20+ years of insurance PE track record confirming the structural validity of Novel's model

- The GeoVera Nova integration (AM Best A/Excellent, SageSure distribution partnership) provides Novel with a high-quality catastrophe-exposed residential platform at a moment when cat-exposed capacity commands premium pricing — the timing is structurally advantageous

Competition

- Direct competitors (insurance holding company build-outs): Transverse (specialty insurance holding, Blackrock-backed), Obsidian Insurance Holdings (PE-backed diversified carrier), Accelerate Insurance Holdings — a new cohort of PE-backed holding companies forming simultaneously

- Category competitors: Established insurance holding companies (Markel, Fairfax, RLI, Kingsway) — the structural models Novel is studying and attempting to replicate at speed

- Emerging dynamic: PE capital is flowing into insurance holding company formation at an accelerating rate as the hard market creates favorable conditions for new carriers — Novel's management team quality is its primary differentiation in a field with increasingly sophisticated competitors

Market Consequences

The insurance holding company formation wave — Novel, Transverse, Obsidian, and others launched in 2023–2025 — is entering its capitalization phase simultaneously. PE firms with dedicated insurance vehicles (Flexpoint Insurance Opportunity Fund, Stone Point's Insurance Solutions Fund) are the primary capital sources, creating a competitive dynamic where management team quality and structural differentiation matter more than capital access. Novel's Bonneau/Bredahl founding team is the clearest differentiation signal in the current cohort. The SageSure distribution partnership embedded in the GeoVera Nova relationship provides immediate commercial traction for the catastrophe-exposed property segment — one of the most constrained capacity categories in the current market. For specialty property owners, real estate investors, and HOA managers in catastrophe-exposed markets, Novel/GeoVera Nova represents additional capacity from an A-rated platform at a moment when available capacity is scarce.

Bottom line: A former PartnerRe CEO and former Howden Re CEO launched an insurance holding company thirteen months ago. It already manages $2 billion in GWP, owns an AM Best A-rated cat carrier, and just attracted Flexpoint Ford's dedicated insurance fund. That is the pace of a team that knows exactly what it's building.

3. Matic (USA)

Undisclosed Minority Investment + Policygenius P&C Book Acquisition | Embedded Insurance — PE-Backed Consolidation Date: June 24, 2026

What Happened

Columbus, Ohio-based Matic — an embedded insurance platform integrating homeowners and auto insurance into the mortgage origination, servicing, banking, and real estate ownership journey — announced two simultaneous transactions: a minority strategic growth investment from Primus Capital, and the acquisition of Policygenius's property and casualty insurance portfolio (approximately 30,000 policies across home, auto, and other personal lines). Matic was founded in 2014 by Ben Madick (CEO) and Dmitry Melnichenko (CTO). The company's digital marketplace includes 70+ insurance carriers and 100+ distribution partners spanning mortgage origination/servicing, banking, real estate, and personal finance. Policygenius's P&C policies fall outside Policygenius's core life insurance focus — the acquisition is a natural fit and transfers customers to Matic's carrier marketplace with no coverage disruption. Primus Capital is a growth-oriented PE firm focused on healthcare, software, and technology-enabled services; Matic is its first insurance technology investment. Terms of both the investment and the acquisition are undisclosed.

- Investor: Primus Capital (minority, growth equity)

- Acquisition target: Policygenius P&C portfolio (~30,000 policies, home/auto/other personal lines)

- Prior institutional investors: Homie, SWK Holdings, Nationwide Insurance (strategic)

Use of Funds

- Continue development of Matic's proprietary insurance platform

- Expand embedded partnership network (currently 100+ partners)

- Pursue further inorganic growth — book acquisitions and strategic partnerships

- Integrate Policygenius's P&C policyholders into Matic's carrier marketplace

Strategic Thesis

Matic is executing a two-track growth strategy simultaneously: organic (embedded partnership expansion with banks, mortgage servicers, and real estate platforms) and inorganic (acquiring books of business from platforms exiting P&C). The Policygenius acquisition is the second track in action — Policygenius's life insurance focus creates a natural divestiture candidate for its P&C book, and Matic's embedded platform is the most natural buyer: it already has carrier marketplace access across 70+ insurers, it serves the homeownership journey, and it has the customer service infrastructure to absorb 30,000 policies without operational disruption. Ben Madick's framing — "build Matic to be the leading home-led agency" — is the strategic intent precisely stated. Primus Capital's backing gives Matic the capital and operational partnership to execute further acquisitions systematically, not opportunistically. The pattern is becoming clear: embedded insurance platforms with strong distribution partnerships and carrier marketplace depth are becoming natural consolidators of P&C books from platforms whose primary business is not P&C insurance.

Why It Matters

- 30,000 Policygenius P&C policies transferred through Matic's embedded platform demonstrates that AI-native embedded platforms can absorb book acquisitions without proportional operational cost increases — the same pattern as Connie Health in Medicare navigation

- Primus Capital's investment is its first insurance technology bet, signaling that growth equity firms without prior insurance specialization are now viewing embedded insurtech platforms as investable growth equity opportunities — expanding the capital base available to the category

- The 100+ distribution partner network spanning mortgage, banking, and real estate creates a compounding distribution advantage: each new embedded integration generates customer touchpoints at a natural insurance need moment (home purchase, mortgage refinancing, new construction) that organic customer acquisition cannot replicate at equivalent cost

Competition

- Direct competitors (embedded home/auto insurance): Kin (Florida-focused, direct), Openly (homeowners MGA, Allianz X-backed), Branch Insurance (bundled home/auto), Hippo (homeowners)

- Category competitors: Traditional captive agency models (State Farm, Allstate), independent agent networks, digital insurance aggregators (The Zebra, Insurify)

- Emerging dynamic: As mortgage servicers and banks seek to embed insurance more deeply into homeownership journeys, embedded platform depth (carrier options, partner integrations, customer service quality) becomes the primary competitive moat — Matic's 70+ carrier marketplace and 100+ partner network is the largest in the category

Market Consequences

Policygenius's decision to divest its P&C portfolio while retaining its life insurance core is a strategic signal about where digital marketplace aggregators see their long-term competitive advantage — life insurance, with its higher commissions and advisory complexity, versus P&C, where commoditization and price competition reduce platform margin. Matic's willingness to absorb P&C books creates a structural dynamic: digital platforms with P&C books but life-primary strategies have a natural counterpart in Matic. Additional P&C book acquisitions are likely. For traditional personal lines carriers competing for homeowner insurance customers, Matic's 100+ embedded distribution partnerships represent an alternative channel that is growing — policies written through embedded platforms in a mortgage origination flow have higher retention because the relationship is embedded in the homeownership journey itself, not dependent on renewal marketing.

Bottom line: Matic just bought 30,000 Policygenius P&C policies and attracted its first PE backer simultaneously. The embedded insurance roll-up thesis — acquire books from platforms exiting P&C, serve them through your carrier marketplace, integrate them into your embedded distribution network — is now in active execution.

4. Mitigata (India)

$15M Series B | India's First IRDAI-Regulated Cyber Insurance Broker — AI-Native Resilience Platform Date: June 23, 2026

What Happened

Founded in 2023 by Mohit Anand (CEO), Sarthak Dubey (COO), Mayank Morya, and Akshit Kaushik, Bangalore-based Mitigata is India's first IRDAI-regulated insurance broker focused exclusively on cyber insurance, operating as an AI-native full-stack cyber resilience platform. The company closed a $15 million Series B led by Bessemer Venture Partners (Pankaj Mitra, Partner), with existing investors Nexus Venture Partners (Anand Datta, Partner), Titan Capital, and WEH Ventures participating. Mitigata's platform integrates security operations, cyber risk intelligence, compliance automation, digital forensics, incident response, and cyber insurance into a single operating framework built on the principle: Insure. Detect. Defend. Recover. The company has grown 12–15x over the past year, now serves 800+ organizations across financial services, healthcare, manufacturing, retail, and technology, and has processed more than one million security incidents through its AI-native security operations centre. Prior raise: $5.9M Series A (Nexus-led, August 2025). Total raised: ~$21M.

- Lead investor: Bessemer Venture Partners (Pankaj Mitra, Partner)

- Participating investors: Nexus Venture Partners, Titan Capital, WEH Ventures (all existing)

Use of Funds

- Expand Security Operations Centre into India's largest sovereign AI security infrastructure

- Double headcount across AI research, product, engineering, and customer success

- Accelerate international expansion beyond India

- Deepen homegrown AI security infrastructure investment

Strategic Thesis

Mitigata's architecture is the most sophisticated articulation of the cyber insurance convergence thesis: the company that underwrites the cyber risk is the same company that monitors, detects, and responds to the threats that generate that risk. Traditional cyber insurance is a financial instrument — it pays after a breach. Mitigata's platform is an operational instrument — it reduces the probability and severity of a breach before it happens, and coordinates incident response when it does. The convergence creates a structural advantage that standalone insurers and standalone security vendors cannot replicate independently: Mitigata's security operations data directly informs its underwriting model, creating a feedback loop that improves risk selection and pricing as the platform grows. Bessemer's Pankaj Mitra named the competitive dynamic precisely: "The accelerating number of AI-driven malicious attacks, combined with a severe shortage of cybersecurity talent, has resulted in a perfect storm for Indian enterprises." India's combination of high digital adoption, sophisticated threat landscape (state-grade AI-driven attacks), and critical cybersecurity talent shortage creates ideal conditions for a platform that delivers security outcomes as a service alongside the insurance that covers residual risk. IRDAI regulation as India's first dedicated cyber insurance broker is a structural moat — regulatory approval takes years, and Mitigata already has it.

Why It Matters

- India's first IRDAI-regulated cyber insurance broker is not a coincidence — it is a structural moat that took years to build and cannot be replicated quickly by competitors entering after Mitigata has established market position

- 12–15x growth in twelve months at 800+ enterprise clients demonstrates product-market fit in a segment (Indian enterprise cyber) that has historically been severely underinsured relative to actual risk exposure

- The Bessemer investment signals global growth equity confidence in the Indian cyber insurance/resilience category at a moment when AI-driven threats are making cybersecurity a board-level priority in markets where it was previously an IT operational concern

Competition

- Direct competitors (India cyber insurance): Tata AIG Cyber Insurance, HDFC ERGO Cyber Secure, New India Assurance Cyber policies — all traditional carrier products without integrated security operations

- Category competitors: Global managed security service providers (MSSPs) without insurance integration, pure-play cyber insurance carriers (Coalition, At-Bay, Cowbell — U.S.-focused)

- Emerging dynamic: The convergence of cyber insurance and managed security services is a global trend — Coalition's security scanning, At-Bay's risk monitoring, Cowbell's continuous underwriting signals — Mitigata is executing the convergence thesis for India with regulatory approval that global platforms lack

Market Consequences

India's enterprise cyber insurance market is structurally underinsured: high digital adoption, sophisticated threat landscape, and a regulatory environment that is rapidly requiring cyber risk disclosure create demand that traditional carriers offering standalone policies cannot serve adequately. Mitigata's integrated platform — insure, detect, defend, recover — addresses the full risk lifecycle rather than only the financial consequence. For traditional Indian carriers (Tata AIG, HDFC ERGO, New India) offering cyber policies as standalone products, Mitigata represents a category competitor that bundles the insurance with the service that makes the insurance unnecessary in ideal scenarios. The international expansion signal is significant: Mitigata's architecture is replicable in Southeast Asian markets (Singapore, Indonesia, Malaysia) with comparable digital adoption profiles, talent shortages, and threat landscapes — markets where IRDAI regulation doesn't apply but the operational model translates directly.

Bottom line: India's first regulated cyber insurance broker just raised a Bessemer-led Series B. It grew 12–15x in twelve months. The platform doesn't just pay after a breach — it monitors, detects, and responds before one happens. That is not a better cyber insurance product. That is a different category.

Special Situation: dodoAI (Japan)

¥280M (~$1.8M) Seed | Enterprise AI Governance — Mitsui Sumitomo Insurance Venture Capital as Investor, P&C Insurer as Pilot Client Date: June 21, 2026

What Happened

Tokyo-based dodoAI Inc. (formerly 58 Inc., rebranded June 1, 2026) closed a ¥280 million (~$1.8M) seed round led by Genesia Ventures, with participation from Quantum Leap Ventures, Mitsubishi UFJ Capital, Mitsui Sumitomo Insurance Venture Capital, and angel investor Hideki Otsuka (CEO, Speee). dodoAI provides a "Sovereign Agentic OS" — an enterprise-grade AI governance platform that monitors, verifies, and audits AI-generated outputs while requiring human approval before final execution. The platform is model-agnostic (supports OpenAI, Anthropic Claude, Google Gemini) and deployment-agnostic (public cloud, on-premises, air-gapped). An active P&C insurer pilot disclosed: a large Japanese non-life insurance company deployed dodoAI to AI-driven development across a subsystem of a core platform — reducing labor requirements by 35–98% in targeted areas while maintaining quality standards. The company operates 34 employees across Tokyo, Ho Chi Minh City, and Hanoi.

Why It Matters for Insurance

Two insurance-linked investors in a ¥280M seed deal — Mitsui Sumitomo Insurance Venture Capital and Mitsubishi UFJ Capital (the banking arm that insures through Tokio Marine, its MUFG affiliate) — is not a coincidence. It reflects the same recognition that drove Nassau Financial to invest in Trussed AI last week: insurance carriers are deploying AI at scale in operations, underwriting, and claims — and they need the audit and governance infrastructure before regulators require it. Japan's FSA (Financial Services Agency) has been among the most active global regulators in AI governance frameworks for financial institutions. Mitsui Sumitomo Insurance Venture Capital investing in dodoAI is a carrier-level signal that the Japanese insurance industry is preparing for AI governance requirements rather than reacting to them. The P&C insurer pilot result — 35–98% labor reduction in targeted subsystems — establishes that the product works in live insurance environments, not just in controlled tests.

The AI Governance Thread — Now Confirmed Cross-Continental

Three weeks: three AI governance investments with direct insurance connections.

- Week 24 (June 7–13): Poetic $50M — OpenAI-backed deterministic AI execution architecture deployed at AIG at 99%+ accuracy. Governance-through-architecture.

- Week 25 (June 14–20): Nassau Financial → Trussed AI — insurance carrier investing in AI governance and audit infrastructure for regulated enterprise AI. Governance-as-compliance.

- Week 26 (June 21–27): Mitsui Sumitomo Insurance Venture Capital → dodoAI — Japanese insurance CVC investing in sovereign agentic OS with human-in-the-loop review. Governance-as-operations.

Three different governance approaches. Three different geographies (USA, USA, Japan). Three consecutive weeks. This is not a coincidence. It is a sector recognizing simultaneously, across jurisdictions, that AI deployment without governance infrastructure creates regulatory and operational exposure that is arriving faster than most compliance calendars assume.

Bottom line: Mitsui Sumitomo Insurance Venture Capital just backed AI governance infrastructure in Japan. Last week Nassau Financial did the same in the US. The carriers building AI governance capability now are running three weeks ahead of the carriers still deciding whether they need it.

Special Situation: IAG Firemark Ventures / Spacecube (Australia)

$3M Strategic Investment | Modular Disaster Recovery Infrastructure — Completing the Firemark Resilience Portfolio Date: June 26, 2026

What Happened

IAG Firemark Ventures — the corporate venture arm of Insurance Australia Group (ASX: IAG), led by General Partner Scott Gunther — made a $3 million strategic investment in Spacecube, a Melbourne-based modular building company founded by Mark Davies (CEO). Spacecube manufactures flat-packable, transport-ready modular accommodation and community infrastructure units that can be delivered and assembled within hours in challenging terrain, including off-grid environments without utility connections. Units are self-sufficient: integrated solar, battery storage, and rainwater/septic compatibility. The investment follows a successful pilot deployment after the January 2026 Victorian bushfires, where Spacecube units enabled multiple displaced families to remain on their properties while permanent homes were rebuilt — rather than relocating to temporary accommodation centers far from their land, communities, and livelihoods. Under the new partnership, Spacecube becomes part of IAG's disaster response capability across rural and regional Australia under the NRMA Insurance, CGU, WFI, and RACV brands. Geographic expansion to New Zealand and potential urban/commercial applications are under consideration.

- Investor: IAG Firemark Ventures ($3M strategic)

- Target: Spacecube — modular rapid-deployment accommodation and community infrastructure

- Prior Spacecube investors: Taronga Group, AfterWork Ventures

- IAG brands deploying: NRMA Insurance, CGU, WFI Insurance, RACV

The Firemark Portfolio Architecture — Revealed

Scott Gunther's statement this week is the most strategically significant thing IAG has said in any of its four consecutive Firemark investment announcements: "This latest investment by Firemark Ventures expands our deliberately constructed disaster-resilience portfolio that spans prediction, detection, assessment and now rapid on-property recovery."

That sentence maps the full Firemark stack for the first time:

- Prediction: 7Analytics — geoscience-driven flood and landslide prediction models at asset level

- Detection: Near Space Labs — high-frequency aerial imagery for real-time event monitoring

- Assessment: Sonder (Week 25) — immediate mental health and safety triage at the moment of crisis

- Recovery: Spacecube (Week 26) — rapid physical shelter deployment within hours of displacement

This is not a CVC portfolio assembled deal by deal. It is a purpose-built insurance value chain — from predicting which assets are at risk, to detecting when an event occurs, to supporting the policyholder psychologically in the immediate aftermath, to providing physical shelter while permanent repairs proceed. Each investment addresses a different failure mode in the traditional insurer's disaster response capability. Together they describe a carrier that intends to be present at every stage of a disaster lifecycle, not only at the claims lodgment and settlement stages.

Why It Matters

The Spacecube investment closes the loop on what IAG has been building through Firemark for the past two consecutive weeks in a way that no individual investment announcement made clear on its own. The strategic intent — disclosed explicitly for the first time in the Spacecube announcement — reframes the Sonder investment retroactively: IAG was not making a one-off mental health bet. It was laying one layer of a four-layer disaster resilience infrastructure.

For insurance industry observers, the significance is architectural: IAG has quietly assembled what may be the most complete disaster response capability owned by any insurer globally, spanning geoscience prediction, aerial imagery, psychological first response, and physical shelter — all through minority CVC investments in specialist companies, not internal builds. The capital deployed is small relative to IAG's balance sheet. The strategic differentiation is large relative to any competitor who responds to disasters only after claims are lodged.

Competition and Market Consequences

Suncorp, Allianz Australia, and QBE Australia — IAG's primary Australian general insurance competitors — respond to disasters primarily through claims assessment and settlement processes. None has a comparable vertically integrated disaster-response investment portfolio. The policyholder experience differentiator that IAG is building is not a product feature that can be replicated through a marketing campaign — it requires four separate technology relationships, a pilot deployment track record, and a deliberate portfolio construction thesis. That is 18–24 months of execution minimum for a competitor starting from scratch today.

The Spacecube model also has direct financial logic beyond policyholder welfare: a displaced homeowner who remains on their property in a Spacecube unit maintains daily visibility over the rebuild, reduces the risk of contractor disputes and delays, and has lower secondary loss costs (alternative accommodation, storage, community displacement effects) than one relocated to temporary housing far from the site. If IAG can demonstrate actuarially that Spacecube deployments reduce total claims cost per event, the $3M investment is not a CSR expense — it is a claims management tool.

Bottom line: IAG just disclosed that it has been deliberately building a four-layer disaster resilience portfolio — prediction, detection, psychological support, physical recovery — through Firemark Ventures. The Spacecube investment is the final layer. No other insurer has assembled this stack. The competitive advantage is not any single investment. It is the architecture.

Special Situation: Taktile (USA / Germany)

$110M Series C | Goldman Sachs-Led Agentic AI Decision Platform — One of the World's Largest Insurers Projecting $90M+ in Claims Savings Date: June 24, 2026

What Happened

Founded in 2020 by Maik Taro Wehmeyer (CEO) and Maximilian Eber (CTO), New York- and Berlin-based Taktile closed a $110 million Series C led by Growth Equity at Goldman Sachs Alternatives (Christian Resch, Partner; Jade Mandel, Managing Director), with participation from Balderton Capital, Index Ventures, Tiger Global, Y Combinator, and Dig Ventures. Total funding: $184M. Taktile provides an Agentic Decision Platform that allows banks and insurers to deploy AI agents for high-stakes, high-volume decisions — underwriting, claims processing, fraud detection, compliance — through a modular architecture that integrates with existing core systems. The platform's December 2025 milestone: Taktile Labs confirmed frontier AI models had crossed the threshold required for reliable high-stakes financial decision automation. Named production outcomes: 95% automation in B2B underwriting; 75% reduction in AML false positives; one of the world's largest insurers running multiple claims use cases projecting $90M+ in cost efficiencies. Named customers (non-insurance): Mercury, Monzo, Faire, Pleo. The insurer customer is unnamed. The Fortune exclusive describes a tornado claims workflow: document reading agent → coverage interpretation agent → payout decision agent — three sequential AI agents completing a process that previously took human examiners weeks.

- Lead: Growth Equity at Goldman Sachs Alternatives

- Investors: Balderton Capital, Index Ventures, Tiger Global, Y Combinator, Dig Ventures

Why the $90M Insurer Claim Matters

The $90M projected savings figure is company-reported and insurer-unnamed — standard practice for enterprise AI vendors protecting client confidentiality. But it is consistent across the primary press release (BusinessWire), the Fortune exclusive, and eight additional sources — and Goldman Sachs Growth Equity, which led the round with full access to customer data under NDA, validated it with their investment. The figure is therefore treated as credible and notable, with the appropriate caveat that it is projected savings from a single large insurer, not realized across all customers.

The Fortune tornado claims workflow description is the most concrete public articulation of how multi-agent insurance claims automation actually works in production: not a single AI model answering a question, but a sequential chain of specialized agents — each handling one defined task (reading, interpreting, deciding) — with human oversight available at each handoff. This is the architectural detail that most AI claims automation vendors describe in abstract terms. Taktile's CEO described it in a specific, verifiable workflow for a specific peril (tornado) in a specific state (Minnesota). That level of specificity is either a production deployment being described accurately, or a sales claim exposed to immediate customer verification. Goldman Sachs Growth Equity does not lead $110M rounds on unverified sales claims.

Why It Belongs Alongside Pace, Poetic, and Sapiens

Taktile joins Pace ($46M, Thrive/Sequoia, Prudential/WTW in production), Poetic ($50M, OpenAI/KP, AIG in production at 99%+ accuracy), and Sapiens' Agentification programme (ADIA-backed) as the now four best-capitalized AI automation platforms with documented insurance production deployments disclosed in June 2026 alone. The category is no longer emerging. Four simultaneously well-capitalized, Goldman- and OpenAI-backed platforms are all competing for the same carrier automation budgets, with real production references at named insurers, in the same 30-day window.

Bottom line: Goldman Sachs just led a $110M round into an AI platform where one of the world's largest insurers is projecting $90M+ in claims savings. The tornado claims workflow — three sequential AI agents, document to decision — is the clearest public description of production AI claims automation published this year. The benchmark is now set.

Special Situation: The Doctors Company / ProAssurance (USA)

$12B Combined Asset Base | Medical Professional Liability Merger — Close Date: June 26, 2026

What Happened

The Doctors Company (TDC) — the nation's largest physician-owned medical malpractice insurer — completed its acquisition of ProAssurance Corporation (NASDAQ: PRA), a Birmingham, Alabama-based specialty insurance holding company focused on medical professional liability and workers' compensation. The merger closed June 26, 2026, following regulatory approvals in Alabama and multiple other states, plus FTC HSR antitrust clearance (granted July 2, 2025). ProAssurance shareholders received $24.50 per share in cash. The combined entity's total asset base is approximately $12 billion, creating the dominant U.S. medical professional liability insurer by scale. ProAssurance brings its NORCAL Mutual (acquired 2021) and Medmarc (specialty products liability) operations into the combined platform. TDC continues under its existing physician-governed structure.

Why It Matters

The MPL market has been consolidating for years — NORCAL absorbed into ProAssurance, ProAssurance now absorbed into TDC — and the combined $12B entity is a qualitatively different competitor than either legacy platform. Scale in MPL matters because loss development tails are long (a claim filed today may not resolve for 5–10 years), reserving accuracy requires deep historical data, and reinsurance pricing is significantly better at $12B than at $5B. For physicians, hospitals, and healthcare systems shopping MPL coverage, the combined TDC/ProAssurance now has the balance sheet, the actuarial depth, and the claims management infrastructure to compete for any account nationally.

Bottom line: The dominant U.S. physician-owned MPL insurer just absorbed its largest competitor. The combined $12B platform is a new competitive reality in medical malpractice — and a template for the next wave of specialty lines consolidation.