Frictionless customer experience is the future of insurance customer engagement. Today, the interaction with insurance comes at the cost of mental effort, and sometimes pain. Insurance companies that manage to smooth the customer's interaction gain a new 'value proposition' that they can offer to the customers. The customer journey doesn't start from the "search for insurance policy", it starts from understanding the risk and reason for purchasing an insurance policy. One journy ends after a customer purchases a policy, another journey ends after the customer recovers her loss.

This technology is not going to replace the human insurance agent. In the next couple of decades the number of the insurance agents will decrease as the Millennials matures, Gen-X retires, demand changes and the technology evolves. However, today's artificial intelligence (AI) can not, yet, provide a warm shoulder, a hug and an empathy.

Adam Gabrault, VP at VirtusaPolairs, talked with the InsurTech Los Angeles meetup about the technology that powers the frictionless user experience and mapped the journey that a customer takes to purchase an insurance policy.

Everything is going mobile

The frictionless customer experience is crafting the digital paradigm. E-Commerce, social networks and media had cracked the code - one tap to buy, one swipe for love and recommended content is a scroll-down away from you. Although it has been 10 years since the mobile revolution, the financial institutions and insurance companies have a mobile presence because "everyone else has an app". Luckily there are FinTech and InsurTech that act as path finders and introduce a mobile first with less friction service as Mint, Lemonade, Acorns and Trov.

What the insurance companies need to do to be mobile?

I will start with the disruptive concept that demands restructuring of insurance carrier product lines and IT infrastructure and that is - shift from policy-centric to customer-centric approach. Instead of selling the insurance product that you have, sell what the customer wants and needs.

During his talk at the InsurTech Los Angeles meetup Adam pointed seven additional actions:

- Reduce time to quote & cover improves conversion rates

- Digital natives demand a frictionless experience

- Expanded DIY servicing options enhances customer retention

- Digital engagement is replacing & augmenting physical channels

- AI & IoT open new markets including driverless cars, usage based policies etc

- Collaboration between carriers & InsurTech will accelerate innovation

- Agent experience must be enhanced to maintain relevancy

It starts by creating personas and addressing their needs. Let's take John as an example:

Let's reimagine the buying experience

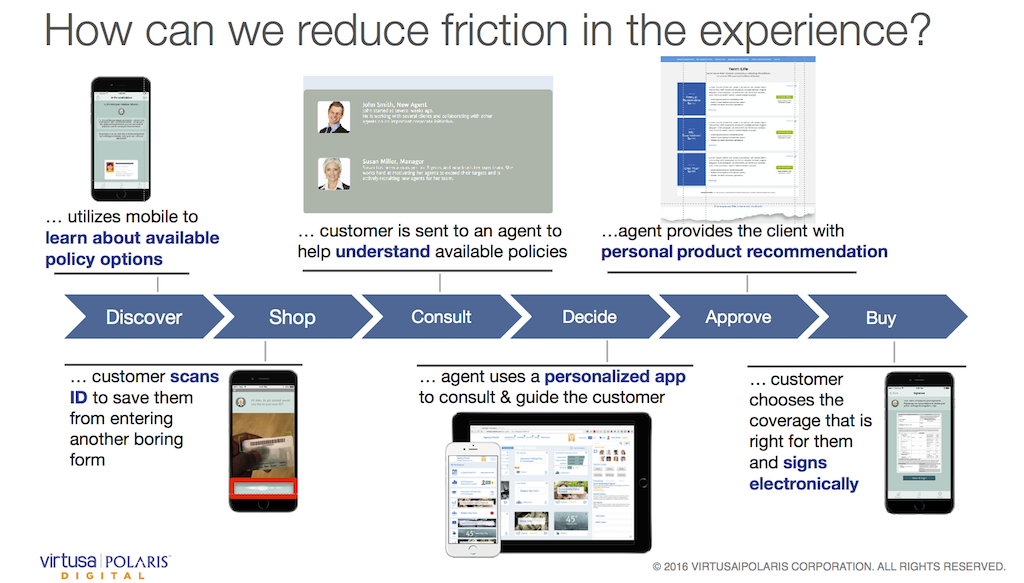

Discover

Migrate the discovery from searching the web to an optimized mobile experience. There are opportunities here for InsurTech startups to develop services that can recommend customized coverage for the user.

Shop

Instead of filling a form and waiting for a sales representative to call you back and then repeat the form's questions, integrate identification systems and allow the customer to scan her/his ID card.

Consult

An agent will consult the customer on the best policy for him. Does the agent need to be a human or can it be an AI? For companies that positioned themselves as a premium service and use agents as the main distribution channel it will be a human that utilizes AI apps for efficiency.

Decide

Instead of the website, or the agent, try to up-sell and cross-sell other products to the user, a personalized app or agent will guide the customer.

Approve and buy

Move from endless paper forms to readable language (less legal) and e-signature.

Let's make insurance frictionless

We can make it by reducing the friction in various points of engagement. It is not important to address the side of the insurer as well and provide customer service and the insurance agents effective tools to make their work productive and helpful.