Cyber Insurance is among my InsurTech trends predictions for 2018. The attention Cyber insurance receives has increased in the past year in the wake of media coverage of cyber attacks and Trump administration.

To better understand the opportunity in the Cyber insurance products I would like to share with you an interview with Nir Perry, the CEO and founder of CyberWrite, a company dedicated for the development of cyber insurance technologies.

The future of the agency - LA InsurTech Talk

The agents and the brokers are a cornerstone of the insurance industry. They are true entrepreneurs that, in most cases, start a business, hire people and serve their customers. With the rise of the InsurTech wave and the entrance of tech entrepreneurs to the insurance industry the agents, and mainly the brokers, are perceived as a middleman, as a cost that digital products can, and should replace in the name of cost reduction and efficiency. These claims, are partially false, or plainly disconnected from the insurance industry.

Fire side chat with Jeremy Hallett

I invited Jeremy Hallet, CEO of Hallett Financial and founder of Quotacy, to a fireside chat to answer the question how technology changed the agent's business throughout the years. From the introduction of the fax machine, the pager, the mobile printer to the mobile phone and the iPhone. I wanted Jeremy to share with the audience his twenty years of experience in the insurance industry and the motivation to launch Quotacy.

When one invites a knowledgeable speaker, one needs to invite a knowledgeable interviewer.

Jason Cass joined InsurTechLA as an interviewer to ask all the hard, and soft, questions and to keep a fast pace and a high energy discussion.

Broadcasting the event live

I recommend to watch the event as it was vivid and overflowing with information. Here are several snippets (with edits) from the discussion.

[Q] JC: in the past several years, billions of dollars were invested into the new insurTech companies and none of them is making a profit. Does it make sense?

[A] JH: I didn't read all the balance sheets of all the companies that are out there, but it takes two to four years to grow a business. I invest my revenue back in the business so I can bring it to the next level.

[Q] JC: Let's talk about IoT.

[A] JH: Hippo, an MGA that positioned in the market as premium service, provides Roost, a leak detector, to its customers. By been pro-active the carriers can provide IoT devices and reduce unnecessary claims.

"A smoke detector is built to beep at 3 in the morning, that's how the chemistry in the 9v battery works. A 9v battery with Wifi can tell you, your phone, that it is beeping".

The insurance companies see the changes and want to adopt it. The InsurTech companies push the carriers better than the agents towards that change.

JH: a Wells Fargo executive told me "I have millions of customers; I cannot make a mistake. But a new FinTech startup can go and make mistakes. They can go and make version 1 and then version 2 and 3. Only then, Wells Fargo will step in and buy the tech, the supporting technology and what else is going on".

The change

[Q] GS: how the technologies (Iot, CRM, new quoting systems etc) help the agents?

[A] JH: I would say - push the carriers to adopt the technology, the services and reduce the rates and improve the service.

There are agents who want to change and adapt new tools and new ways. They need the carriers help.

JH: how can I help the agent that works for me, or uses Quotacy, to provide service to a 45 years old couple who wants to protect their family.

JH: underwriting manuals are 2,000 pages long. I work with twenty carries. It is hard to compare the best price and coverage in 40,000 pages.

JC: I get it, it is all about making the money. There are four pieces: Price, Cost, Coverage and Service + Relationship. The carriers control everything but the relationship. It is hard to place a price tag on customer relationship.

The mix of the agent and the tech will be a winner.

JC: Jeremy, tell us about Quotacy.

JH: Quotacy is the best place to buy life insurance. My other goal is to get 1,000,000 families under the umbrella.

Customer engagement

Do you pick up the phone from an unfamiliar number?! No. If you are expecting an email I'll send you an email.

Fast claim process leads to a happy customer and a better brand.

The agency

Technology and AI don't come to take our employees (the agency) jobs. New tech enables us to give our employees meaningful work.

JC: the industry is lacking young people. The agency owner can be the cause and solution to the problem that prevents the advancement of his own business. If you give a young man a phone book and tell him to start dialing, first, I don't think he ever saw a phone book, second, he will not do it because there are better ways to work.

The agency owner should find a way out of the "pale, stale, male" problem.

JC: I write commercial insurance. The carrier expect a renewal on November 1st. I need to meet the business owner in September because the carrier tells me it will take 60-90 days to underwrite it.

We should have weekly policies. The reason that we have a yearly policy is the time that it takes to write the policy. Take a look at Trov and Slice.

Meaningful work, meaningful life.

@LAinsurTech with Jason Cass

Setting up the place. Once again, my thanks to Carbon Five that made their Santa Monica office available to the LA InsurTech community.

Master of the chairs - Joe Scheffler

Frictionless Customer Experience

Frictionless customer experience is the future of insurance customer engagement. Today, the interaction with insurance comes at the cost of mental effort, and sometimes pain. Insurance companies that manage to smooth the customer's interaction gain a new 'value proposition' that they can offer to the customers. The customer journey doesn't start from the "search for insurance policy", it starts from understanding the risk and reason for purchasing an insurance policy. One journy ends after a customer purchases a policy, another journey ends after the customer recovers her loss.

This technology is not going to replace the human insurance agent. In the next couple of decades the number of the insurance agents will decrease as the Millennials matures, Gen-X retires, demand changes and the technology evolves. However, today's artificial intelligence (AI) can not, yet, provide a warm shoulder, a hug and an empathy.

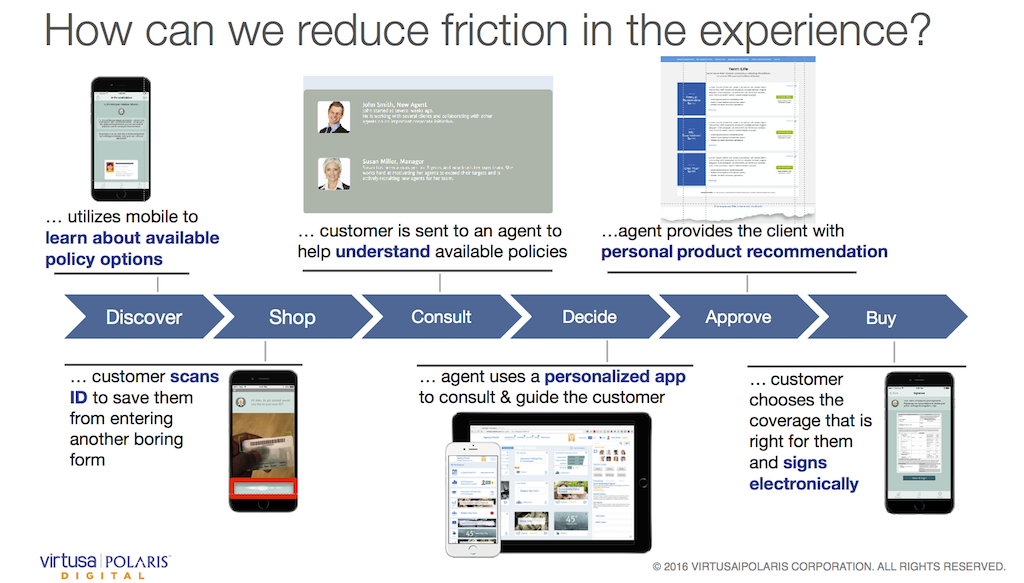

Adam Gabrault, VP at VirtusaPolairs, talked with the InsurTech Los Angeles meetup about the technology that powers the frictionless user experience and mapped the journey that a customer takes to purchase an insurance policy.

Everything is going mobile

The frictionless customer experience is crafting the digital paradigm. E-Commerce, social networks and media had cracked the code - one tap to buy, one swipe for love and recommended content is a scroll-down away from you. Although it has been 10 years since the mobile revolution, the financial institutions and insurance companies have a mobile presence because "everyone else has an app". Luckily there are FinTech and InsurTech that act as path finders and introduce a mobile first with less friction service as Mint, Lemonade, Acorns and Trov.

What the insurance companies need to do to be mobile?

I will start with the disruptive concept that demands restructuring of insurance carrier product lines and IT infrastructure and that is - shift from policy-centric to customer-centric approach. Instead of selling the insurance product that you have, sell what the customer wants and needs.

During his talk at the InsurTech Los Angeles meetup Adam pointed seven additional actions:

- Reduce time to quote & cover improves conversion rates

- Digital natives demand a frictionless experience

- Expanded DIY servicing options enhances customer retention

- Digital engagement is replacing & augmenting physical channels

- AI & IoT open new markets including driverless cars, usage based policies etc

- Collaboration between carriers & InsurTech will accelerate innovation

- Agent experience must be enhanced to maintain relevancy

It starts by creating personas and addressing their needs. Let's take John as an example:

Let's reimagine the buying experience

Discover

Migrate the discovery from searching the web to an optimized mobile experience. There are opportunities here for InsurTech startups to develop services that can recommend customized coverage for the user.

Shop

Instead of filling a form and waiting for a sales representative to call you back and then repeat the form's questions, integrate identification systems and allow the customer to scan her/his ID card.

Consult

An agent will consult the customer on the best policy for him. Does the agent need to be a human or can it be an AI? For companies that positioned themselves as a premium service and use agents as the main distribution channel it will be a human that utilizes AI apps for efficiency.

Decide

Instead of the website, or the agent, try to up-sell and cross-sell other products to the user, a personalized app or agent will guide the customer.

Approve and buy

Move from endless paper forms to readable language (less legal) and e-signature.

Let's make insurance frictionless

We can make it by reducing the friction in various points of engagement. It is not important to address the side of the insurer as well and provide customer service and the insurance agents effective tools to make their work productive and helpful.