$1.05B+ in disclosed investment activity | 2 transactions | A quiet week by count, a generational one by signal

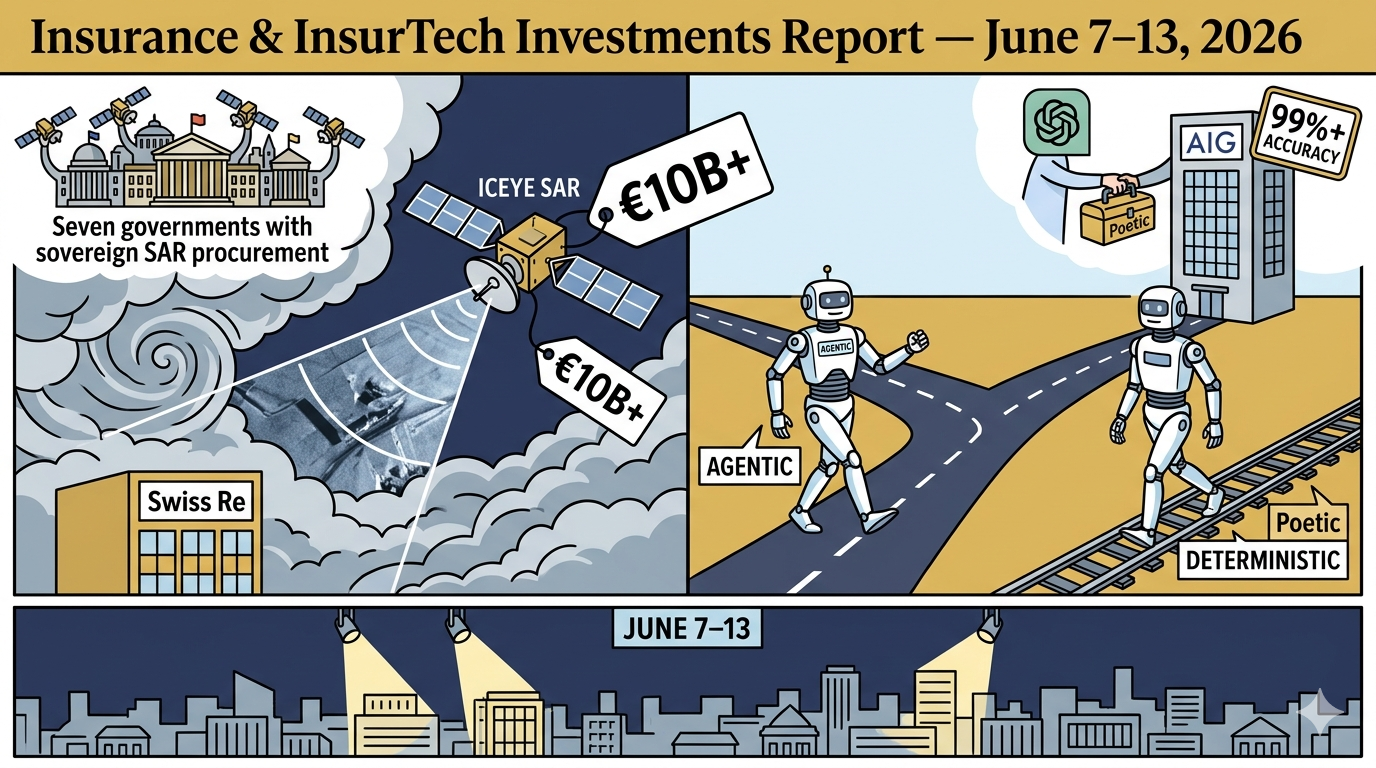

Two deals. One pushed a Finnish satellite company past a €10 billion valuation on the strength of demand from sovereign governments and the insurance carriers — Swiss Re, Juniper Re, AXA — that already depend on its imagery. The other put OpenAI's own capital behind an AI system that AIG is running in production today, at 99%+ accuracy, on a process that used to take humans hours. Neither deal is "an insurance round" in the traditional sense. Both are insurance infrastructure rounds — capital flowing into the tools that will determine which carriers see risk clearly and operate efficiently, and which don't. After three consecutive weeks of multi-billion-dollar carrier transactions (HHH/Vantage, PayPay/T&D, Nationwide/MassMutual, DB Insurance/Fortegra), this week's quiet exterior conceals two of the most consequential infrastructure bets of the year.

1. ICEYE (Finland)

€1B+ (~$1.16B) at €10B+ Valuation | Series F — Sovereign Intelligence and Insurance Catastrophe Infrastructure Date: June 9, 2026

What Happened

Founded in 2015 by Rafal Modrzewski (CEO), Helsinki-based ICEYE operates the world's largest constellation of synthetic aperture radar (SAR) microsatellites — currently 70 satellites in orbit, providing all-weather, day-and-night Earth observation imagery regardless of cloud cover. The company closed a €450 million ($520M) primary Series F round led by General Atlantic, at a valuation exceeding €10 billion ($11.5–12B) — roughly quadrupling its €2.4 billion valuation from a €200M round closed just six months earlier (December 2025). Including a secondary share placement for existing shareholders, the total transaction exceeded €1 billion. ICEYE now ranks among Europe's largest privately held technology companies — a "decacorn" alongside Finnish peers Oura and Supercell. The company serves Swiss Re, Juniper Re, and Insurity as named clients in the insurance vertical, alongside seven European governments that have procured sovereign satellite systems. New primary capital will fund expansion of manufacturing capacity, targeting production of 100 satellites per year by 2028, up from the current rate of 50.

- Lead: General Atlantic (Sascha Günther, Managing Director, led the investment)

- New investors: Qatar Investment Authority (QIA), Nokia, TCV (watchlist hit — TCV is one of the 35 tracked funds)

- Existing investors participating: Solidium, Tesi, Varma, Ilmarinen, Lifeline Ventures

Use of Funds

- Scale satellite manufacturing from 50 to 100 units per year by 2028

- Expand global footprint and intelligence capabilities for sovereign and commercial clients

- Continue vertical integration of the SAR satellite production platform

Strategic Thesis

Six months ago, ICEYE was worth €2.4 billion. Today it is worth more than €10 billion. That is not market sentiment — it is demand outpacing supply at a rate that forces a structural re-rating. ICEYE's SAR constellation solves a problem that optical satellites cannot: imaging through cloud cover, at night, during the exact conditions when catastrophes — hurricanes, floods, wildfires — are most active and most in need of monitoring. For insurance, this is not a nice-to-have. Swiss Re, Juniper Re, and Insurity use ICEYE's imagery to assess portfolio exposure during live events and accelerate claims triage with observed data rather than modeled estimates. For governments, SAR constellations are now understood as essential national security infrastructure — seven European governments have already procured sovereign systems, a trend accelerated by the post-2022 security environment. General Atlantic's Sascha Günther's framing — "the world's largest and most advanced SAR constellation on a vertically integrated platform" — is the investment thesis in one sentence: ICEYE doesn't just operate satellites, it manufactures them, controlling its own supply chain at a moment when demand for sovereign space-based intelligence has no real ceiling.

Why It Matters

- TCV's participation — the same growth equity firm that led Corgi's back-to-back raises three weeks ago — signals that TCV is building a thesis around AI-and-data infrastructure companies serving insurance and financial services from multiple angles simultaneously

- The valuation quadrupling in six months reflects a genuine supply constraint, not hype — ICEYE is doubling its manufacturing capacity because demand from governments and insurers already exceeds what 50 satellites/year can serve

- Swiss Re, Juniper Re, and Insurity's continued reliance on ICEYE as named clients means the insurance industry's access to real-time, all-weather catastrophe imagery is now tied to a company valued at €10B+ — the strategic importance of the relationship has been re-rated alongside the company

Competition

- Direct competitors (SAR satellite constellations): Capella Space, Umbra, Synspective (Japan)

- Category competitors: Optical Earth observation providers (Planet Labs, Maxar) — limited by weather and daylight constraints that ICEYE's SAR technology does not share

- Emerging dynamic: As ICEYE's production scales toward 100 satellites/year, the resolution, revisit-rate, and coverage advantages over optical-only competitors compound — insurers without SAR-based catastrophe monitoring access increasingly compete with an information disadvantage during live events

Market Consequences

For the insurance industry, ICEYE's re-rating is a forcing function. Carriers and reinsurers that built catastrophe response workflows around ICEYE's imagery — Swiss Re, Juniper Re, Insurity — now have access to a company with the capital and manufacturing scale to double its constellation by 2028, widening the resolution and coverage gap versus competitors relying on traditional optical imagery or licensed catastrophe models alone. Carriers without an equivalent SAR data relationship face a widening information gap during live catastrophe events — the exact moment when claims triage speed and exposure assessment accuracy matter most. The broader signal for insurance-adjacent infrastructure investors: companies that solve hard physical-world data problems at sovereign scale are being valued as strategic national infrastructure, not as venture bets — and the insurance relationships embedded in those companies appreciate in strategic value alongside them.

Bottom line: ICEYE quadrupled in value in six months because the world — governments and insurers alike — needs to see through clouds faster than the company can currently build satellites. Swiss Re, Juniper Re, and Insurity are already inside that relationship.

2. Poetic (USA)

$50M Series A at $500M Valuation | AI Process Automation — AIG, SoFi, Chime as Production Clients Date: June 10, 2026

What Happened

Founded by Markie Wagner (CEO) — a Thiel Fellow and former machine learning engineer at Google and Waymo, previously running an AI consultancy called Delphi Labs — San Francisco-based Poetic (formerly operating under the name "Forge") emerged from stealth with a $50 million Series A at a $500 million valuation. Poetic has built a new category of automation software: rather than deploying autonomous AI agents, it uses a purpose-built programming language that lets operators define complex, high-stakes business workflows in natural language while delivering deterministic execution — described by the company as software that "learns like AI but runs like code." AIG is named as a production customer, with Poetic reporting 99%+ accuracy on a complex, multi-hour insurance process that previously required significant manual effort. At SoFi, Poetic achieved 99%+ quality executing fraud investigations end-to-end within five weeks, with CEO Anthony Noto confirming "100% process adherence, even in our most complex compliance investigations." Chime is also named as a customer. The company reports an eight-figure run rate achieved with just four employees in 2025, and a 100% pilot-to-production conversion rate across every client engagement to date.

- Lead: Kleiner Perkins (Leigh Marie Braswell, Partner, led the investment)

- Participating investors: OpenAI, Founders Fund (Peter Thiel), First Harmonic

Use of Funds

- Expand forward-deployed implementation teams

- Accelerate growth into additional industries beyond financial services

- Bring the platform to more of the world's largest enterprises

Strategic Thesis

Poetic's investor list is the thesis. OpenAI investing directly in an application-layer company is rare — it signals that OpenAI views Poetic's deterministic-execution architecture as solving a problem that general-purpose AI agents have not solved: reliability at the accuracy threshold insurance and financial services actually require. Markie Wagner's framing — "in AI, there's too much attention on quick demos and shiny objects, and not enough on outcomes" — is a direct critique of the autonomous-agent approach that dominates current AI product positioning, including approaches taken by companies like Pace (which raised $46M three weeks ago on an agentic AI thesis). Poetic's bet is that insurance underwriting, fraud investigation, and compliance — processes where being wrong 5% of the time is genuinely unacceptable — require a fundamentally different architecture: a programming language for AI-directed workflows that produces the same correct output every time, rather than an agent that reasons its way to an answer with some probability of error. The 100% pilot-to-production conversion rate, if it holds as the company scales beyond four employees, is the single most important data point in the announcement — it suggests Poetic has solved the production-reliability problem that has stalled the majority of enterprise AI deployments industry-wide.

Why It Matters

- AIG running Poetic in production at 99%+ accuracy on a complex, multi-hour insurance process — with the company's own framing emphasizing deterministic execution over autonomous agents — represents a direct architectural alternative to the agentic AI approach that Pace, Blitzy, and most AI-insurance startups have taken

- OpenAI's direct investment in an application-layer company serving insurance and financial services is a signal about where OpenAI sees durable value accruing in the AI stack — not just at the model layer, but at companies that solve enterprise reliability problems on top of models

- The eight-figure run rate achieved with four employees, prior to this raise, demonstrates the capital efficiency that the "software that learns like AI but runs like code" architecture enables — a structurally different cost base than agent-based competitors requiring larger engineering teams to manage non-determinism

Competition

- Direct competitors (insurance process automation): Pace (agentic AI operations, $46M Series B three weeks ago), Sapiens' Insurance Agentification (Agentic Claims, Agentic Underwriting), Gradient AI, Ushur

- Category competitors: Traditional RPA vendors (UiPath, Automation Anywhere) serving the same back-office automation use cases with non-AI approaches

- Emerging dynamic: The architectural divide between "agentic AI" (Pace, Sapiens' Agentification programme) and "deterministic AI-directed execution" (Poetic) represents two competing bets on how enterprise AI reliability gets solved — both are now well-capitalized and will compete for the same carrier automation budgets

Market Consequences

For carriers evaluating AI automation vendors, Poetic's emergence creates a genuine architectural choice that didn't exist as clearly three weeks ago: agentic platforms that reason through workflows with some probability of error per step, versus deterministic platforms that execute a defined process the same way every time. AIG's production deployment at 99%+ accuracy gives carriers a reference point for the deterministic approach at the exact moment Pace is establishing reference points for the agentic approach at Prudential and WTW. Competing automation vendors — Gradient AI, Ushur, and traditional RPA providers — now face well-capitalized competitors on both architectural fronts simultaneously. For insurance back-office and compliance functions specifically, the bar for "production-ready AI automation" has been set by two different companies in the same month, at two different insurers (AIG for Poetic, Prudential/WTW for Pace) — carriers without an active evaluation in either category are now visibly behind two direct industry peers.

Bottom line: OpenAI just backed a company that bets enterprise AI's reliability problem is solved by writing deterministic code that AI directs — not by trusting an agent to reason its way there. AIG is already running it in production at 99%+ accuracy. That is a direct challenge to every agentic AI platform currently selling into insurance.